I never copy. Everything I type comes out of my mind, which, in a world where I mostly see repetition, it’s something I’m proud about. Nevertheless, I cannot help but remark that this article is highly in line with Geoff’s “Things That Don’t Change”. Give his Substack a read, it’s unique content from the wisest professional I’ve met.

The really stuck with me and, when I went over one of Christensen’s findings, resemblance was notorious. I’m currently reading The Innovator’s Dilemma. It’s been a slow read given it’s not my morning book and that it’s, even though academic, spectacular. These are the types of books I think are most important to properly digest and internalize.

Sustaining technologies

We’ve covered thoroughly what Clayton understands by disruptive innovation and why can it make large firms collapse. On this occasion, it is in the second type of technology where I want to put the focus on.

Sustaining technologies are small improvements to previously created products. They, by definition, are innovations upon disruptive innovation. The zero to one move creates the market, displaces old technology and sustaining technologies are meant to maximize the efficiency at which this new product operates. Generally, we tend to see sustaining technologies translated into annual rates of productivity improvement.

A good example I can think of is the iPhone. Steve Jobs was in charge of disrupting the smartphone market. But, after the invention, where did we go? iPhone model 15 or something like that is about to hit the market. Each subsequent model of the iPhone had more throughput, more computing power, improved UI, UX and many more marginal upgrades.

The common pattern

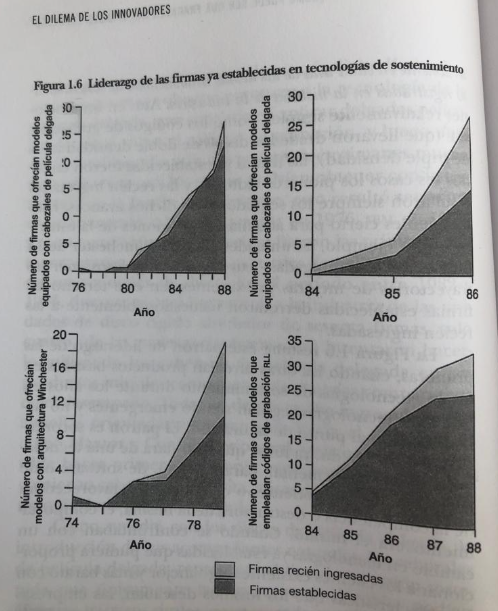

During the read, there was something that strongly hit me. Christensen utilizes the disk drive market to expand on the idea. Clayton found that, in cases of sustaining technology development upon already established products (disk drives), the companies that generally led the charge were the already established ones. And he goes even further (I’m translating):

“Established firms were not only leaders in innovation with regards to the development of risky technologies, but literally every single subsequent sustaining innovation that was registered in the history of the industry”.

Even more interestingly, almost all new companies that tried to enter the market at a point at which a sustaining technology was being introduced, went bankrupt. The following image (apologies for being in Spanish) shows the number of firms, the shadow being established ones, that were participating in markets of sustaining innovation.

They dominated all along. New players cannot compete in products that are being improved upon. Startups cannot displace giants in their field, maybe due to accumulated know-how, distribution channel, but not the point of this article. Ironically, new firms are the ones that dominate in products that imply disruptive innovation, which end up displacing established leaders.

In 1978-80, new companies developed 8-inches disk drives, much smaller than the 14 inches, currently offered by leaders. As time went by, the number of 14-inches disk drives producers tended to decline. Two thirds of them never introduced the 8-inch technology. The remaining third did so, but two years after the invention. Finally, all 14-inches producers ended up being expelled from the market. The following images illustrates the same thing as the previous one, but with disruptive technologies.

The holy grail?

The so famously called ‘MOATs’ do not protect companies from disruptive innovation, as far as I’m concerned. It’s what allows businesses to continue investing in sustaining technologies without newcomers eating their profits, perhaps justifiable with Christensen’s work. I wonder, then… a MOAT is not enough to compound capital for really long periods of time.

The crucial image published here is the first one, which shows the tendency of established companies to lead the way in product improvements. That might partially help us answer what are the characteristics of a company destined to compound capital forever, if possible. The key: things that don’t change.

If established companies are most likely destined to lead the way in these sustaining technologies, but with the possibility of being displaced by disruptive innovation, then we have to take the latter element out of the equation. Imagine a company that belongs to an industry with no room for disruptive innovation but that, at the same time, has good margins and returns on capital. That might be a decent definition of an ideal business, a true compounder.

Personal commentary

I’m immersing myself in dark waters. The amount of concentration and information needed to try take these things further is getting increasingly difficult. I will be covering a lot of Clayton’s ideology as he appears to be a brilliant thinker. Hope you enjoyed the article and that it triggers some interesting thoughts!

In case you missed the earnings reviews I posted, here they are:

Thank you for the shout out, Giuliano!

A company with a true moat should be earning a higher return on capital thanks to that moat... and therefore it will always be under attack by competitors. That's why I find it so important to understand potentially disruptive technologies, even if they're not necessarily in my portfolio.