Overall financial analysis

ASML reported results yesterday before the market opened. The company generated over 6.9bn in revenue, growing at 27%. Growth deceleration seems worrying but shouldn’t be. Last quarter’s growth was an outlier due to the extremely weak Q1 ASML had in 2022 when compared to this year’s Q1.

(Keep in mind all numbers are in Euros.)

ASML’s financials are quite volatile on a quarterly basis, or at least have been in the past years. However, this is the fifth quarter in a row in which the company shows consistent sequential growth. Given the nature of its business, occasional drops like we’ve seen in Q1 of 2022 are expected. Nonetheless, good signs of continued normalization. One last thing I’d like to highlight is the extremely rapid growth ASML is experiencing despite the context it’s in. Not only are these quarters being compared to very tough comps, but the semiconductor industry has been in a down cycle for some time now. This does get to show how mission critical are the company’s systems for the industry and the high demand they have.

There is though some component of revenue that correspond to 2022 but was delayed to this year:

“The value of fast shipments in 2022 leading to delayed revenue recognition into 2023 is around €3.1 billion” Q4 2022 press release

“As you know, we fast ship DUV immersion and EUV. But on DUV immersion we came to an agreement with customers, where we basically have a reduced test protocol. Which they now accept as good enough to basically recognize revenue when we ship the machine out of our factory in the Netherlands. Instead of taking revenue when we do the installation at the customer site.” Q2 2023

Moving down the income statement, ASML did 3.54bn in gross profit, up from 2.66bn in the comparable quarter. This translates into a 210bps margin expansion, with GPM being at 51.3%. Operating income came in at 2.26bn, implying a margin of 32.8%, which increased by 240bps. Finally, net income for the quarter was 1.94bn, flat sequentially, but up from 1.4bn last year. ASML operated at a 28.1% net profit margin.

At an operating level, ASML brought in 385M in cash from operations and had 544M in purchases of property, plant, equipment and intangible assets. Consequently, free cash flow was at -161M for the quarter. This is nothing more than seasonality and operating volatility, which is, observed under yearly timeframes, normalized. ASML tends have one strong quarter of free cash flow per year, two at best, generally being the fourth one. Demand explosion since 2020 probably made the business experience unusual income from operations in the rest of quarters as well. However, that has not been the case for the past decade.

Revenue breakdown

ASML derives revenue from two major sources. The first and main one consist in the selling of photolithography machines while the second one in support, upgrading and selling enhancements to further improve performance of old systems sold.

In the last reported quarter, 81% of the company’s revenue came from selling lithography machines. As everything financial-related to ASML, share of revenue is somewhat volatile. Even though system sales appear to have been taking share of total revenue, at least since early 2019, their share of total revenue seems to oscillate between 65-80%.

Additionally, system sales revenue is also split into two main products, deep ultraviolet (DUV) and extreme ultraviolet machines (EUV).

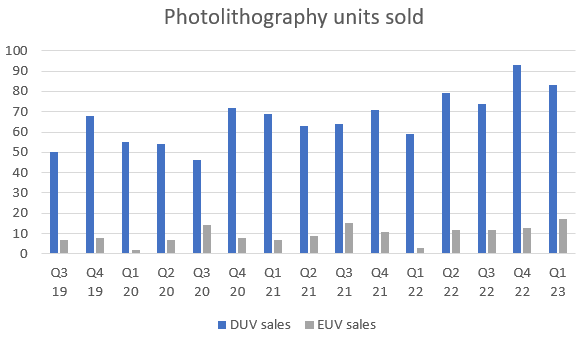

In this last quarter, ASML sold a total of 113 photolithography systems. Out of the total, 12 of them were their most advanced machines, EUV, and the remaining were DUV systems sold.

Moving forward, the company always discloses the regions to which they ship their systems. This is a somewhat useful indicator to see the company’s geographical exposure. Out of the total, 34% of the machines were shipped to Taiwan, 27% to South Korea and 24% to China. Destination also varies quite drastically quarter to quarter. Taiwan represented 49% of the shipments last quarter and, in Q1 of 2022, only 22%. Quarterly isolated numbers tell very little information.

Furthermore, ASML’s sales can also be categorized by the nature of the product’s demand. Logic chips are in charge of processing information while memory chips of storing data. In the last quarter, machines intended to produce logic chips made up for 84% of the total units sold.

Bookings

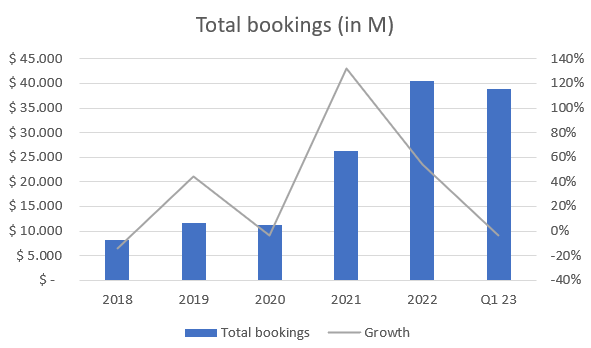

Bookings is a very insightful variable since it allows us to infer what are companies foreseeing and, from ASML’s perspective, it offers a window into its future topline. Moreover, it sort of shows how resilient could the subsequent quarters be for the company, which, in a downturn cycle for the semi industry, can prove useful.

Quarterly net bookings were 4.5bn, up sequentially from 3.75bn, reaccelerating. What is noticeable here is the superb rise in demand for ASML systems, with a backlog of orders raising from 10bn in 2020 to 40bn in 2022. The curious thing is that there is little to no correction or digestion now, like we’ve seen in other sectors. This ultimately reiterates how crucial ASML’s equipment is.

The company ended fiscal year 2022 with 40.4bn in backlog revenue, number which fell sequentially to 38.9bn and now to 38bn. The semiconductor industry has been immersed in a down cycle for some time now, which provides further perspective on how ASML’s bookings act as a form of cushion.

Lastly, 69% of the systems booked are destined towards logic-chip manufacturing. The remaining 31% are machines booked for memory-chip manufacturing.

Out of the 4.5bn of net bookings, 1.6bn correspond to EUV systems. I’ll further discuss bookings in the final section.

Capital return to shareholders

During the second quarter of 2023, ASML repurchased over 500 million dollars in shares, which amounts for 0.25% of the company’s market cap. In parallel, ASML paid 1.2bn in dividends over the first semester of the year.

Outlook and management commentary

Management began by offering context into how the semiconductor space is bearing. Uncertainty remains at very high levels due to the geopolitical environment, inflation and export controls. Additionally, even though there seems to be some end-markets bottoming out of the cycle, demand remains relatively low due to generally high inventories across the board. Customers are looking to moderate wafer output as they work to reduce and rebalance their inventories. Consequently, they lower the use of their lithography tools.

Demand for systems was an interesting point of the conference call. Absolute and long-term demand is high, as always, though immediate demand has somewhat changed and is machine-type-specific. Management mentions EUV has seen some demand shifting forward, a delay. The reason for this is the fabs they are meant for,which are extremely complex. Special and highly skilled people are required to build them and it seems as if there’s not enough supply at the moment, so advanced fabs readiness was pushed.

On the other hand, DUV systems demand is still extremely high, still exceeding supply. Even though there have been some delays from customers due to the aforementioned reasons, this machines have been quickly picked up by Chinese customers particularly. Strong demand for tools at mature and mid-critical nodes compensated delays.

“ our Public Chinese customers say: We are happy to take the machines that others don’t want”

Turning into guidance, ASML plans to ship over 375 DUV systems, with a mix of 25% immersion, some of them using the fast shipment process. Management has come to an agreement that allows revenue recognition on shipment and, as a result, now expect an additional 700M euros in sales (such recognition was expected to be capitalized in 2024, now delayed revenue recognition stands at 2.3bn). This means DUV guidance was raised from a 30% growth to 50% for 2023.

In EUV, due to the adjustments in demand timing related to delays in fab readiness, supply chain and geopolitical uncertainties, management now expects to ship 52 systems this year. This translates into an expected growth rate of 25% for the EUV business unit, compared to the previously expected 40%. Ultimately, both things indicate ASML raised its overall guidance from 25% growth to 30%.

Final remark on the semiconductor landscape and outlook for 2024:

“customers were expecting a recovery in the second half of this year, but it now seems this is moving more towards 2024. Also, the shape and slope of the recovery remains unclear. However, based on a combination of the current firm demand and a strong backlog of around 38 billion euros, there are clearly still opportunities for growth in 2024”

My take

ASML reported a spectacular quarter, very much in line with what it’s used to. The lack of ’digestion’ in bookings is truly notorious and something I’d like to put special emphasis on. It is always talked about how mission-critical the company’s equipment is for foundries. However, the fact that bookings quadrupled in two years with no signs of correction clearly reveals this aspect of lithography machines. Moreover, management always mentions how strong demand is. Customers practically fight over their systems, there’s always a company waiting for another to delay its shipment so that they can take it instead. All of this translates into the rapid growth ASML is experiencing and that it’s coming above management’s own expectations

From a financial standpoint, the company still operates at best-in-class margins and it presents signs of some sort of stability. When enough years have gone by, there is always a point at which margins and returns on capital tend towards. Such point could be seen as the company’s natural profitability. In ASML’s case, both things are very high. Additionally, bookings provide this window into the company’s future as to what to expect and act as a form of cushion that, as seen in the recent downturn, is a great asset.

Personal commentary

I still owe myself a proper research article of ASML, which should allow me to have more insightful observations. I hope you enjoyed the review, next one coming is Tesla’s.

Disclosure: This is NOT financial advice.

Excellent work Giuliano. This article is more than enough to excite someone about ASML!

Gracias por compartir tu trabajo Giuliano, genial como siempre!!