Before going into the article, in the following weeks I’ll also be covering Visa, Google, Microsoft, Texas Instruments, Mercado Libre and Zoetis. If you’d like to receive the earnings reviews at your email, you can subscribe below.

Overall financial analysis

Tesla reported results on Wednesday after the market closed. The company generated over 24.9bn in revenue, growing at 47% on a yearly basis, reaccelerating from the 24% growth rate it saw last quarter. This is outstanding. It seems somewhat surreal that Tesla can keep such high growth rates at this scale.

For some perspective, a comparable player in terms of size who is also growing very fast, AWS, decelerated to a 15% growth rate. Same with Microsoft’s intelligent cloud business unit, being at an 80bn+ run rate, but growing at 16% YoY.

Moving down the income statement, Tesla generated 4.5bn in gross profit, implying a margin of 18.2%, which was down 680bps YoY and 110bps sequentially. The company’s operating margin stood at 9.6%, declining 490bps yearly and 180bps QoQ, meaning Tesla had 2.4bn in operating income. Lastly, net income was 2.7bn for the quarter, the only ‘bottomer-line’ that went up sequentially and yearly. Net profit margin was 10.8%, declining 250bps yearly, but staying flat on a quarterly basis.

Tesla brought in 3.06bn in cash from operations while it had 2.06bn in capital expenditures. Both variables leave free cash flow at 1bn for the quarter. Tesla is a capital intensive company, from all perspectives. It employs a lot of cash to build new gigafactories, improve old ones, improve products (which they actually do) and develop new technologies. Most CapEx is destined though towards capacity expansion, both in terms of EVs and Tesla’s supercharging network. The company’s free cash flow margin has been very volatile over the past couple of quarters, it really depends on the CapEx Tesla incurs in. The business generates vast amounts of cash from operating activities, but reinvests most of it.

Breakdown by segment

Automotive

In the second quarter of 2023, Tesla produced a total of 479,700 vehicles, implying an increase of 86% over the comparable quarter. In the same line, it delivered 466,140 EVs, 83% more than they did last year. Both deliveries and production set a new record for the company and had a decent leap up sequentially.

Relative demand for Teslas has been quite uncertain for some quarters given the mismatch that had been having place between production and deliveries. Management called for a persistence of this mismatch this quarter and the previous one, though the gap narrowed a bit, with deliveries outgrowing production on a quarterly basis. In absolute terms, the story clearly tells demand exceeds supply. If not, deliveries and orders wouldn’t be growing at these orders of magnitude. Finally, global vehicle inventory (days of supply) has continuously grown due to this mismatch as well, now being at 16 days, up from 15 last quarter. However, For next Q:

“We expect that Q3 production will be a little down because we’ve got some shutdowns”

All of this translated into 21.2bn in revenue for the automotive segment. This implied an yearly increase of 45% and 6% sequentially. Moreover, it generated 4.08bn in gross profit, which was flat year on year and down from the past quarter. The margin at which this business unit operates has suffered greatly in 2023, mainly due to the price cuts. This quarter, GPM stood at 19.2%, down 870bps YoY and 190bps QoQ.

As negative as price cuts had been qualified by investors, it allowed Tesla to continue growing at the fast pace it has always done and, consequently, grabbing market share. Tesla market share at the three main regions it operates has ticked up once again and in a pronounced way in EU.

Having more Teslas being driven around is not only beneficial from a financial standpoint, but it also helps to continue feeding Tesla FSD software. The pronounced increase in vehicle deliveries immediately translated to the accumulated miles driven with FSD’s Beta. It has now surpassed the 300M mark and exponential growth should continue since delivered Teslas are still out there, but more will be joining.

“There's just no substitute for massive amount of data. And obviously, Tesla has more vehicles on the road. Then, collecting this data, then all of the companies combined. And really, just don't know how anyone could do what we're doing.”

A key component of Tesla’s automotive segment from a technological and competitive standpoint is their network of supercharger stations and connectors. Both continue growing at 30%+ rates and have now more than quadrupled over the past 4 years. The company is putting real emphasis on this infrastructure.

This allows us to deviate and cover Tesla’s services & other segment, which includes non-warranty after-sales vehicle services and parts, sales of used vehicles, retail merchandise, paid supercharging and vehicle insurance revenue.

“The 2nd quarter of 2023 has been the quarter of Supercharging. A significant number of companies, including Ford, GM, Mercedes, Nissan, Polestar, Rivian, Volvo and Electrify America, have announced adoption of NACS”

Services & other generated a record 2.15bn in revenue, growing at 46% YoY and 17% QoQ. Moreover, its gross profit was 166M for the quarter, which has been quickly ramping up for the past years, meaning the business unit operated at a 7.7% gross margin, an expansion of 390bps yearly and 400bps sequentially. It is remarkable that services & other’s revenue has quadrupled over the past 4 years while the GPM went from -40% to 8%.

Energy segment

Tesla’s energy generation and storage segment had tended nowhere for a couple of years and it started to quickly gain territory after 2020. Since Q1 2020, revenue multiplied by a factor of 5. Moreover, as most of Tesla’s business units, it has been showing strong signs of operating leverage. This past quarter, it did 278M in gross profit, at a margin of 18.4%. The latter experienced an expansion of 720bps on a yearly basis and 740 QoQ.

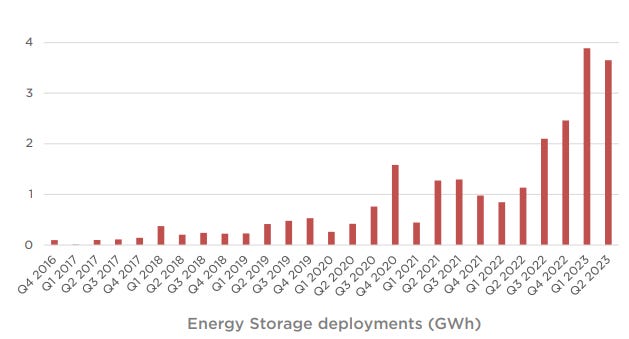

Last quarter saw an abrupt growth in energy storage deployments, measured in gigawatts per hour. Second quarter of 2023 showed a small sequential decline, but it’s still impressively above previous levels. Deployment grew 222% YoY to 3.73.7 GWh. All of this is mainly due to the ongoing ramp of Tesla’s first dedicated Megapack factory in California.

Outlook and management commentary

Some specific guidance before the details:

50% production CAGR is maintained

There is ample liquidity to fund product roadmap and capacity expansion plans

Focus is on reducing costs for improving per unit profit, but management believes innovation in software, AI and fleet-based earnings will increase overall profits

Cybertruck is on track to be delivered this year

During the conference call, one of the main points of discussion was demand and pricing, which affects margins. However, emphasis on demand was quite low with respect to previous quarters, perhaps as a consequence of the superb growth in deliveries. Moreover, Model Y became the best-selling vehicle of any kind globally in Q1, helping deal with demand concerns.

With regards to price cuts, Tesla’s team mentioned their unique advantage of having real-time supply and demand data. Both allow them to price accordingly. Furthermore, management recognizes customers’ costs depend on macroeconomics as well, mainly interest rates, which increase interest payments, leading to an increase in the car’s cost from the customers perspective. Moving forward:

“If macro conditions are stable, I think prices will be stable. And if they are not stable, we would have to lower prices.”

The reason why management has been sacrificing margins goes around the main thesis they have around their EV fleet, the FSD software. It appears that the company wants to have as many cars in the road as possible for two reasons:

More cars mean more data fed into the algorithm, which will ultimately determine Tesla’s value and the capabilities they’ll have. It’s what will separate Teslas from normal cars and Tesla from other companies

Once it’s rolled out, Tesla drivers will be able of either paying a monthly subscription or a full license for 15,000 dollars. The first option should allow Tesla to start earning high margin recurring revenue, making the company much superior at a fundamental level. The second one would imply a massive inflow of high margin revenue, helpful for funding the roadmap and staying ahead of competition.

But, reaching full autonomy is crucial for Tesla to win the race. And to do so, my conjecture is that they need as many cars in the road as possible. Additionally, it will be data and how well-trained FSD is what will dictate how much will Tesla’s lead last in the AI wave and how apart from others:

“It’s well over $1 billion in Dojo. we’ve got a truly staggering amount of video data to do training on. And this is another thing, in order to copy us, you also need to spend billions of dollars on training compute”

Another thing that was mentioned a few times was the Cybertruck. Management reiterated that they expect cybertrucks to started being deliver by the end of this year and for high volume production to start next year. Additionally, they mentioned demand is extremely high and that the product itself will be something truly novel. Lots of new technology.

I believe the following extract contains the perfect explanation of what Tesla’s team plan is:

“the single most important priority is to ensure we are continuing to invest heavily in the core technologies that will drive the long-term value of the business. This include increasing spending on AI-related technologies such as full self-driving Optimus and Dojo, as well as new products such as Cybertruck, our next-generation platform in the semi, as evidenced by the continued growth in our R&D spend. This also includes continuing our investments in capacity expansion, not only in our vehicle factories but also our supercharging network service, internal applications, and battery processes as we continue with meaningful capital expenditures to lay this foundation for the future. Second, we continue to work toward our goals of maximizing volumes on both our vehicle and energy business, but most importantly, doing so in a way that generates the capital to continue our pace of R&D and capital investments.”

My take

The quarter was phenomenal, as usual. I don’t see gross margins as a true concern moving forward. Given Tesla appears to be not only aiming to the automotive market, but to the self-driving one, I think their approach to flooding the streets with Teslas is what will allow them to stay ahead of competition for decades. Furthermore, FSD is only one of the likely many software offerings Tesla will have. Tesla is less and less a car company. They are not the objective of the game, they are the door to Tesla’s ecosystem, to their set of services like superchargers and software-like offerings.

Besides, price cuts should not be something that surprise us, Elon has been calling for this move for over 15 years now. The following statement is from Elon Musk in 2006:

“The strategy of Tesla is to enter at the high end of the market, where customers are prepared to pay a premium, and then drive down market as fast as possible to higher unit volume and lower prices with each successive model”

Tesla’s financials would be a concern if they returned to 2015 or so levels. However, for the past years, operating margins and returns on capital have been quite high. And, interestingly, Tesla has somewhat shown what the true nature of its business is. Every time investments lag on no matter which business unit, margins rapidly climb.

The company has got to a position where it properly funds its own projects and roadmap, which, considering how capital intensive Tesla is becoming, it is a merit by management. Dollars invested today is what will make Tesla remain leading in all fronts. Finally, the company has a stacked and growing cash pile, now at 23bn, offering the needed flexibility if something goes south.

Personal commentary

I really enjoy covering this company. Other upcoming earnings reviews will be on Microsoft, Google, Visa, Zoetis, Texas Instruments and Mercado Libre. Feel free to subscribe below to receive them!

Disclosure: This is not financial advice.

I agree. Underrated quarter. Obviously there are weak points but considering the context, this is excellent execution.