Google reported earnings last Tuesday. As with all earnings reviews, we will first go over the overall business from a financial standpoint, to then dive into each segment. I will also be covering Visa, Texas Instruments, Zoetis and Mercado Libre. Make sure to be subscribed if you want to receive the reviews.

Overall financial analysis

Alphabet generated 74.6bn in revenue, a record only after two strong fourth quarters (the company has some seasonality). Topline grew 7% on a yearly basis and at the same rate sequentially. This puts the company’s 4yr CAGR at 17.6%.

Last year, Google was mostly just digesting the excessive growth it experienced during and after the pandemic. Revenue growth decelerated up to a 1% growth in Q4 of 2022 and then reaccelerated to 3% last Q and 7% on this one. Seems getting back to trending in the right direction. Digestion was something needed and it would be normal to get some more of that moving forward given the pandemic leaped Google’s revenue 2 or 3 years forward.

Alphabet had a record 42.6bn in gross profit, implying a margin of 57%, which was flat YoY and slightly up sequentially, very in line with past years’ average. At the operating level, the company did 21.83bn with the OPM standing at 29.3%, up 140bps YoY and 400bps QoQ. Lastly, earnings for the quarter were 18.36bn, meaning Alphabet had a 24.6% net profit margin, up yearly and sequentially, though still well below the peak in 2021, where investments lagged income.

At the end of last year and also the beginning of this one, management had called for cost-discipline measures. They mentioned and emphasized their intention of returning Google to its previous levels of profitability by a complete re-engineering of their cost structure. One of the big decisions the company made was to not only stop hiring, but doing layoffs. At an average salary of 250k (arbitrary number), every 10k employees that are laid off, the company gets to save 2.5bn in opex.

Google brought in a record 28.6bn in cash from operations, increasing 47% YoY and 21% sequentially. It is worth noticing though that there was an 8bn dollar ‘boost/swing’ in income taxes, which dramatically helped. Cashflow from operations would have been at 20bn otherwise. Capital expenditures saw a step up from last Q, as guided by management, and were 6.8bn. This leaves free cash flow at 21.8bn or a 29% margin.

Before going into each business unit, a brief overview. As a whole, Alphabet generated 74.6bn dollars in revenue. Advertisement revenue was 58.1bn, up 3.2% YoY and representing 78% of total sales. The following chart illustrates how much revenue did businesses contribute as a % of the total.

Break down by segment

In case you are not really sure about what businesses are include in each segment, this image might be useful.

Google Services

Google services is the most relevant contributor to Alphabet’s topline, accounting for 66.28bn dollars. The segment grew 5.4% YoY and represented 89% of total sales, the latter being slightly down yearly and up sequentially. Moreover, it is composed of a wide array of products and services, which are grouped under two large labels, Google advertising, and Google other.

Google Advertising consists of GSearch & Other, YouTube and Google Network. Starting with Google Search & Other, this generated 42.6bn in revenue, up 4.7% on a yearly basis and 5% QoQ.

During 2020/21, GSearch & Other’s size basically doubled, with growth rate reaching 50%+ numbers at 100bn+ run rate, surreal. Companies that experience this kind of unusually excessive demand generally tend to contract in the following years, as it is like the business has got a few years ahead of itself. Nonetheless, even though revenue growth decelerated, it kept growing in all quarters with the exception of Q4 of 2022, when it declined 1%. After that period, revenue accelerated to 1.8% in Q1 and 4.8% in this one. All of this should help illustrate this business’ resilience. Lastly, TTM revenue stands at 165bn, high levels of growth are of course not expected moving forward.

Google Network is composed of Google AdMob, AdSense and Ad Manager. GNetwork’s revenue declined 5% YoY to 7.85bn, but it grew 4.8% sequentially. Alike GSearch and almost all ad-companies, this business unit saw abnormal growth during 2020-22 for which digestion is expected and natural. Alike Search, it seems as if GNetwork bottomed in terms of growth rates in Q4 of 2022, now showing less declines on a yearly basis for the second quarter in a row.

It is unknown to me why has GNetwork struggled and is struggling this much. Could be a product of how competitive the ad landscape has become with Apple, Microsoft and Amazon flooding the space. Nonetheless, comparisons with Search are kind of off. GSearch is one of the best products/businesses that have ever existed.

YouTube, moving forward, generated 7.66bn from advertising, growing 4.3% YoY and 14% sequentially. I feel the need to re-post what I wrote last quarter, as something very similar has occurred:

“The platform has been a very controversial topic due to its ‘weakness’. In this regard, there are several points I’d like to go over that could offer more context on the reasons behind it:

1. YouTube Shorts was released globally in July 2021. Management has been heavily focused on its growth and are just now turning their attention to monetization. This creates a headwind in viewership for YouTube long-form videos and, therefore, to their monetization as well.

2. YouTube began their subscription offerings in 2014, but it is just now taking off. As of the last data I recall, it had over 80M premium subs and over 5M TV subs. This revenue is not included in YouTube ads and, of course, it creates another headwind. YT subscriptions literally eliminate ads from your videos.

3. The platform also saw abnormally high growth during the pandemic and has been trying to digest this growth thereafter.”

The pronounced sequential growth and continuance of the rebound could make one think YouTube ads’ “struggle” has ended or is near the end. YouTube is one of the strongest businesses out there, its MOAT seems impenetrable and seeing it translate rapidly back into topline is positive.

Management commentary on YouTube (ex subscriptions):

YouTube Shorts are now watched by over 2 billion logged-in users every month, up from 1.5 billion just one year ago.

YouTube is growing audiences and driving increased engagement.

Those are the three components of Google advertising services. Altogether, they generated 58.1bn in revenue for the quarter, up 3% YoY.

There was further stabilization in advertiser spend.

Shorts. Momentum remains strong. Watchtime and monetization are moving in the right direction.

Google Other is the final component of Google Services. It is composed of, mainly, Google Play Store, YouTube subscription offerings and hardware sales. Google Other brought in 8.1bn revenue during the quarter, up 24% YoY and almost 10% sequentially, ‘led by strong growth in subscriptions’. Even though the name of this segment makes one think it is trivial, YT subscriptions and Play Store are expected to continue driving high growth moving forward. Pixel could also turn interesting after Google adds Generative AI capabilities to it (via Android).

Management commentary on Google Other:

The Living Room remained the fastest growing screen in terms of watch time. 150M people are reached on Connected TV screens in the US.

Substantial engagement by viewers and ROI for advertisers is driving monetization of the Living Room.

Subscriptions are growing well. Last number was 80M subs in November last year.

Pixel continues to have strong sales momentum.

Play Store returned to positive growth in the second quarter, driven primarily by a solid increase in the number of buyers.

All of the aforementioned businesses make up for Google Services. Total revenue was 66.28bn, up 5.5% year over year. Moreover, it generated 23.45bn in operating income, implying a margin of 35%. The latter expanded 100bps YoY and slightly QoQ.

Google Cloud

In here, we have two products: Google Cloud Platform and Google Workspace. Google Cloud has grown at an extremely fast pace for the past decade, but the problem was the business unit lost more money as quarters went by.

In Q1 of this year, the segment turned operatively profitable for the first time, and the trend continued in this one. Google Cloud generated 8.03bn in revenue during the quarter, growing 28% yearly and 7.7% sequentially, while it had a 4.9% operating margin, having done 395M in operating income. The operating margin expanded 1860bps YoY and 230bps QoQ.

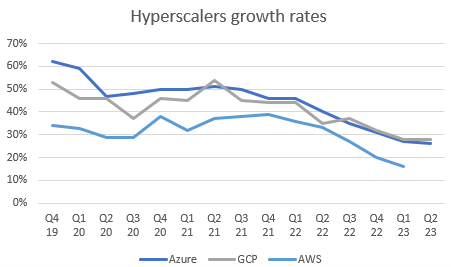

There has been extremely tough competition in the cloud computing space. GCP has been rapidly but barely outgrowing Azure for the past quarters. Google Cloud Platform has been retaining its market share and Azure continuously gaining more. Amazon has not reported results yet.

Management commentary on Google Cloud:

Duet AI was introduced. It helps people collaborate with AI to code, write, etc. Over 750k Workspace users have access to it.

“Our generative AI capabilities also give us an opportunity to win new customers and upsell into our installed base of 9 million paying Google Workspace customers”.

GCP was overall strong. However, there was a continued moderation in the rate of consumption growth as consumers optimized their spend.

Google Workspace strong revenue growth was driven by increases in both seats and average revenue per seat. (I think this is the 8th quarter in a row they say this)

GCP growth was above the growth rate for Cloud overall.

Management commentary and outlook

A large part of management’s speech was around efficiency. They are working on their cost buckets, trying to reduce them as much as possible. To this end, progress was made with regards to the efficiency at which data centers operate. Expense growth will continue to slow down and so should the pace of hiring, as we saw in the pertinent chart. Furthermore, management is optimizing their real estate footprint, reassessing the need or not of having particular offices.

The second worth mentioning bracket was, of course, AI. “Google is on its 7th year of being an AI-first company”. This quote is meant to remember investors that AI has been around for quite a while and Google, even if it hasn’t been doing as much advertising on its capabilities as other businesses, has been playing a leading role in the space. Management mentions that, in fact, nearly 80% of advertisers already use at least one AI-powered Search Ads product.

Alphabet’s intention is very much like Microsoft’s. The company already posses products with immense user bases, some of them almost reaching a physical peak. That’s why, near the limit, Google will now focus and has been focusing on integrating AI across their ecosystem, being able to provide more value to customers. An example is, for instance, Duet AI, which is an AI assistant for writing, coding and extracting insights from data. Moreover, they realize the Search landscape seems somewhat threatened to change and, to protect their monopoly, management has released Bard and seriously improved it since launch. If you want some detail:

“We also added Google Lens capabilities, so you can take an image and ask all kinds of questions, turn it into code, and more. This new feature has been really popular, and it’s been great to see people sharing their experiences. Bard can now read its responses aloud, and you can adjust them for tone and style. We continue to see great interest in using Bard for coding tasks.”

The final thing, though a step below the others in perceived relevance, was YouTube. The company sees YouTube as a true source of future growth and they remind investors of it every conference call. They mentioned how strong momentum has been and, even if it ‘struggled’ with ads, the business itself is doing phenomenal due to subscriptions. Their current focus is on Shorts, Connected TV and subscription offerings, all of which, management mentioned, grew nicely.

My take

Google’s past couple of quarters were decent considering the context it was in. A tough macro environment with a very weak advertising market, plus extremely tough comps in 2020/21 made the company decelerate growth to almost 0%. Perhaps that’s what could make someone think the company wasn’t doing alright, which was not my opinion. I think, considering everything, that Google has done well all along, though with no wonderful quarters. Nevertheless, this quarter was, finally, much better than the previous ones.

Almost all business units returned to decent clips of growth, with all of them continuing to accelerate. Google Cloud Platform is growing at a faster pace than the 28% shown, we don’t know how fast, so it might be even taking share from the giants. YouTube has probably surpassed the 40bn annual run rate with revenue coming from ads and subscriptions. The business unit’s MOAT and optionality are huge, it’s an authentic monopoly over the audiovisual marketplace. Moreover, GSearch, thought as dead and disrupted, returned to decent growth, which is always good to see, and more so given its size. All margins returned to trending upwards and operating leverage continues to rapidly kick in GCP.

As a final remark, Google is not only Search. It has abundant sources of potential growth and all of them are doing well. Additionally, even if it were only about Search, it has been my view since the research was done, that displacing it will be far from easy. Not only it is an internalized-as-it-gets habit, but it is a product reinforced by many other billion-user products. Gmail, GChrome, Android are all wheels that spin around Search, but that make Search spin as well.

Personal commentary

Lots to say with respect to Google. I hope you enjoyed the article and got all the relevant information there is about the quarter. Next in line are Texas Instruments, Visa, Zoetis and Mercado Libre. Make sure to be subscribed below in order to receive them.

Disclosure: This is not financial advice.

Impeccable, as always.