I will be covering Google, Visa, Texas Instruments, Zoetis and Mercado Libre. If you’d like to receive them, make sure to be subscribed below.

Microsoft reported their 4th quarter earnings results last week. Keep in mind it follows a different fiscal year, being two quarters in advance of the calendar. Nonetheless, I’ll utilize calendar quarters for there to not be any confusion. As usual, we will first analyze the overall business to then dive into each segment.

Overall financial analysis

The company generated a record 56.1bn dollars in revenue, growing 8.3% YoY and 6.3% sequentially. However, Microsoft’s business model is composed of two types of offerings. The first of them is product, which includes generally hardware-like products that are typically charged as a one-time fee. Secondly, Microsoft offers services to clients, all sort of software-based offerings and, due to its recurrent-usage nature, the company charges monthly/yearly subscriptions for them.

Subscription-based offerings tend to be much more resilient, making up for a fundamentally stronger business. Since Satya Nadella became CEO, emphasis has been placed in turning Microsoft into a subscription-based business, or as close to that as possible. Consequently, recurring revenue as a percentage of total sales have been continuously trending upwards, now standing at 70%.

Moving down the income statement, Microsoft generated 39.3bn in gross profit, implying a gross profit margin of 70.1%, up 280bps YoY and 60bps QoQ. For the quarter, it had 24.25bn in operating income, operating at a 43.2% margin, which increased by 360bps YoY. Finally, the company made 20.08bn in net income, meaning the net profit margin stood at 35.7%, also up 350bps YoY. Note that there was a 500M boost from other income and 1bn in provision for taxes in comparison to last year’s Q helping the bottom line.

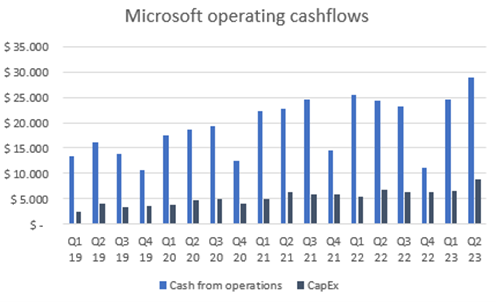

During this last quarter, Microsoft brought in 28.77bn in cash from operations, the highest amount ever, increasing 16% on a yearly basis. Similarly, it had the highest amount of capital expenditures, being 8.94bn. Both variables leave the free cash flow at 19.82bn for the quarter, which curiously was not a record as it fell below March 2022’s.

Before going into a detailed analysis on each segment’s performance, a general overview. During the quarter, the Productivity and Business Processes segment generated 18.29bn in revenue, growing 10% yearly. The Intelligent Cloud business unit did 23.99bn in revenue, up 15% YoY. Finally, More Personal Computing had a total revenue of 13.9bn, which fell 3.5% YoY.

More importantly, the margins at which segments are operating are vital to determine how much are they contributing to Microsoft’s bottom line. To this end, P&BC, IC and MPC made up for 37%, 43% and 20% respectively, of total operating income. I’d say it’s objectively good to see this is the case, same with revenue shares, because P&BC and IC have stronger inherent competitive advantages and fundamentally superior characteristics.

Breakdown by segment

If you are not sure what products compose each business unit, this image might be useful.

Productivity and Business Processes

Along with Intelligent Cloud, this is one of the two business units I believe matter the most for the company. In here, we have products that still have a long runways, can be sold at high margins, have a thesis on their own, are mostly subscription-based with strong lock-in effects, and are immersed in this hybrid industry of professionals and productivity with a leading position.

P&BP generated 18.29bn in revenue, growing at a 10% rate on a yearly basis and 4.4% sequentially. Moreover, it operated at a 49.5% margin, which was up over 500bps YoY and slightly QoQ. This means the business unit did 9.05bn in operating income. The abrupt margin expansion YoY is more due to a weak comparable quarter, which had much lower margins than the past 8Qs average.

In here, the main offerings I pay attention to are Dynamics (Dynamics 365 is key), Microsoft Office (Teams is key) and LinkedIn. All products have been growing at double digits for a long time and growth accelerated during 2020/21. LinkedIn even got to 40%+ growth rates.

This past quarter, Office 365 commercial seats grew 11% while Microsoft 365 consumer subscribers grew 12.2% to 67M. Remember commercial seats are for enterprises and consumer subscribers are professional individuals, mostly. Both businesses’ growth rates seem to be stabilizing at low double digits.

Dynamics grew 19% on a yearly basis and continued accelerating QoQ, having grown by 17% last quarter and 13% the previous one. Dynamics 365, a component of Dynamics, was a major contributor to this, growing at 26% YoY. This was the first fiscal year in which Dynamics revenue was reported and it’s at 5.4bn for the TTM.

Lastly, LinkedIn grew 5% on a yearly basis, and has generated 15.1bn in the last twelve months. Deceleration on LinkedIn has been notorious, but it seems to be more growth digestion than other thing. It grew at unusually high rates for over two years, deceleration is more than normal until this extra growth gets digested. Nevertheless, management guided for continued deceleration for the next quarter, which may start to indicate something’s going on. Even though FY23’s growth rate was healthy, at 8%, it’s important to keep an eye on this.

Management commentary:

“We are taking share in every category”

All-up, more than 63,000 organizations have used AI-powered capabilities in Power Platform, up 75% quarter-over-quarter.

Power Automate now has 10M MAUs, up 55% YoY

Dynamics surpassed 5bn in revenue this FY (it was launched in late 2016)

Feedback on Microsoft 365 Copilot is that it’s a game changer for employee productivity.

There are more than 1900 apps in Teams app store and cusomters have built over 145k custom lines of business apps

Teams Phone is the market leader in cloud calling, with more than 17 million PSTN users, up 45% year-over-year.

Microsoft Viva has 35M MAUs

LinkedIn has now more than 950M members. Talent Solutions surpassed 7bn in revenue in the TTM

Intelligent Cloud

The IC segment generated 23.99bn in revenue, showing high and persistent growth. On a yearly basis, IC grew 15.3% and, sequentially, 8.6%. Being at an almost 90bn run-rate, exhibited growth is nothing but impressive. Furthermore, this is accompanied by a continued show of operating leverage. Intelligent Cloud did 10.52bn in operating income, implying a 43.8% margin, which has been expanding for several years now, though it has been around these levels for the past two or so.

Intelligent Cloud also constitutes a very large part of Microsoft’s thesis because of the nature of this business, with fantastic fundamentals. But, as with the previous segment, there are many businesses embedded here, with most of them having shown very rapid growth, profitability at scale and still have long runways. Among some of the secular trends Microsoft has candidate leaders are cloud computing, cloud security and open-source development.

Azure, probably the most important component of Microsoft’s ecosystem, grew by 26%, showing a slight deceleration from the previous quarter’s 27%. Remember Microsoft does not disclose Azure particularly, it includes it with other cloud services. It is remarkable that, given Azure’s size, which might be at a 55-65bn run rate, it continues to grow at 26% on a yearly basis. Deceleration is expected as it gets larger, but Azure’s holding relatively well. AWS, as a comparison, guided for low-mid double digits growth for this quarter I believe.

Management commentary:

The Microsoft Cloud surpassed $110 billion in annual revenue, up 27% in constant currency, with Azure all-up accounting for more than 50% of the total for the first time

Azure Arc has 18k customers, up 150% YoY

Great momentum across Azure OpenAI Service, with more than 11k organizations, with 90% of them added this Q

Microsoft Fabric was introduced this Q and over 8k customers signed up for the trial. Over 50% are using 4+ workloads

27k organizations have chosen GitHub Copilot, up 2x QoQ

More than one million organizations now count on our comprehensive, AI-powered solutions to protect their digital estate across clouds and endpoint platforms, up 26% year-over-year. More than 60% use 4+ security products, up 33% YoY

Microsoft Entra ID has more than 610M MAUs

More Personal Computing

The last segment that Microsoft has is MPC, which has been posing trouble for the past couple of years. The pandemic got this business to grow extremely fast and its fundamentals are not completely meant for client retention nor does it have immense secular tailwinds backing its growth up. Partly due to these reasons, MPC has struggled with growth and its profitability.

More personal computing generated 13.9bn in revenue, declining 4% on a yearly basis, but growing 4.8% sequentially. This business unit’s revenue is generally all over the place so quarterly growth probably means nothing, or at least it ain’t determinant. Moreover, it operated at a 33% margin, getting back to 2019-2021 levels.

In this segment, not many singular products are of extreme appeal to keep a close eye on, at least from the perspective of what conforms Microsoft’s main thesis in my opinion. Nevertheless, it is in here where they have Bing’s revenue and their gaming segment. The first of them has suddenly materialized as a potential growth driver for the company after it announced the collaboration with Open AI and integrated their features into the search engine. Similarly, Microsoft is working on a chatbot that would work as an AI assistant for its products.

The gaming segment is a somewhat secondary element, but the company is working in making it a business with strong fundamentals. Satya intends for it to become a subscription-based offering via the game pass, which would act as a key to Microsoft’s realm of titles and cloud gaming platform.

Management commentary:

Devices thar run on Windows 11 has 2x YoY

Azure Virtual Desktop and Windows 365 surpassed 1bn in revenue for TTM

To date, Bing users have engaged in more than one billion chats and created more than 750 million images with Bing Image Creator.

Microsoft Edge took share for the ninth consecutive quarter.

Record engagement across Game Pass, with hours played up 22%

Management commentary and outlook

Management discussed the overall strength and momentum their business is having across the whole board. High and profitable growth is being achieved in almost all business units. What they particularly emphasized is how they are trying to integrate AI with all of their products, something they’ve been doing with things like GitHub Copilot, Bing’s Conversational AI capabilities and, more recently, Microsoft 365 Copilot. Management also mentioned integrations across power platform and how strongly positioned is Azure with respects to AI development and application. What the company believes all of this will translate to is rapid growth for customers, more value received from the cloud and improved efficiency, helping their bottom lines.

Bookings fell 2% YoY ‘as healthy renewal was more than offset by a prior year comparable that benefited from a material volume of large, multi-year commitments’. Commercial remaining performance obligations stood at 224bn at the end of the quarter, increasing 18% on a yearly basis. What was curious about this quarter is that there was a record number of 10M+ contracts for Azure and Microsoft 365, meaning Microsoft is locking in multiple very large organizations. Similarly, Azure contracts saw the highest average annualized value for long-term contracts, mainly driven by AI. This should, in some way, transmit customer’s excitement for future releases or simple infrastructure usage for development.

Guidance:

We expect capital expenditures to increase sequentially each quarter through the year as we scale to meet demand signals.

We are committed to driving operating leverage

Guidance first Q:

P&BP revenue of 18-18.3bn, growing 9-11%. Office 365 should drive Office commercial growth, with an expected 16% in cc. Linkedin revenue growth is expected in the low-mid single digits. Dynamics expected growth is of mid to high teens

IC revenue of 23.3-23.6bn, growing 15-16%. Revenue will continue to be driven by Azure, with an expected growth rate of 25-26%.

MPC revenue of 12.5-12.9bn, declining 6-3%. Windows OEM revenue is expected to decline low to mid-teens and devices mid-30s. Search and news ads is expected to grow mid to high single digits.

My take

I believe Microsoft’s quarter was spectacular, even slightly better than the past couple of quarters. Seeing P&BP and IC continue gaining share of the overall revenue and operating income is great. These two business units have much better fundamentals, including very high switching costs, a more predictable topline, the ability to easily cross-sell services, etc.

In parallel, big positive that Azure continue to grow its share out of Microsoft’s Cloud revenue, making it continuously grab market share from the cloud computing market. Additionally, signs of growth stabilization have been showing across the board, with some rebounds.

Moving forward, even though bookings decreased, commercial RPOs increased dramatically. Guidance for the next quarter implies an 8.3% yearly growth rate, sticking relatively close to their ambition. Moreover, customers are showing trust and excitement towards Microsoft’s and Azure’s future, with large and long-term contracts being at the highest level ever. Finally, for the full year, management committed to continue driving operating leverage by being cost disciplined. Margin expansion is also part of their ambition. Good to see them delivering on that.

The only point I’d say left me a bitter taste is LinkedIn’s growth rate, which does not seem to bottom. FY23’s growth rate was healthy at 8%, but I was not expecting for it to decelerate further moving past this quarter. I’ll be keeping a very close eye on this because LinkedIn’s is, in my opinion, a big pillar in Microsoft’s thesis.

Finally, and as a sidenote, Microsoft is working towards improving the fundamentals of the More Personal Computing business with things like the Game Pass, Chat integrations, Cloud Gaming, Azure Virtual Desktop and Windows 365. All of this should translate into a higher margin and higher predictability revenue source.

Personal commentary

Somewhat long earnings review, but Microsoft is immense and I always try to cover as much ground as possible, without falling into redundancy or triviality. Hope you enjoyed the article and make sure to be subscribed if you’d like to receive the next reviews, which will be on Google, Texas Instruments, Visa, Zoetis and Mercado Libre.

Nice write up on Softie.