This article corresponds to the third part of Zoetis research. If you haven’t gone through part 1 and part 2, I’d suggest you at least skim through them, as it should help you get the full grasp of this piece. Many specificities were addressed in those write-ups. Anyhow, hope you enjoy the article.

Thesis

Complexity can be either a curse or a blessing. Fortunately, Zoetis thesis is quite straightforward. The company discovers, develops, manufactures and commercializes animal medications. The latter consists of vaccines, medicines, biodevices, diagnostic products and services.

The ultimate goal of such products is to keep animals healthy, and the reason for doing so varies from specie to specie. Nonetheless, the objective is, almost always, to cure, prevent, slow down and/or diagnose diseases. Understanding this is crucial as it is directly linked with the company’s thesis. Zoetis differentiates among two different group of animals; companion and livestock.

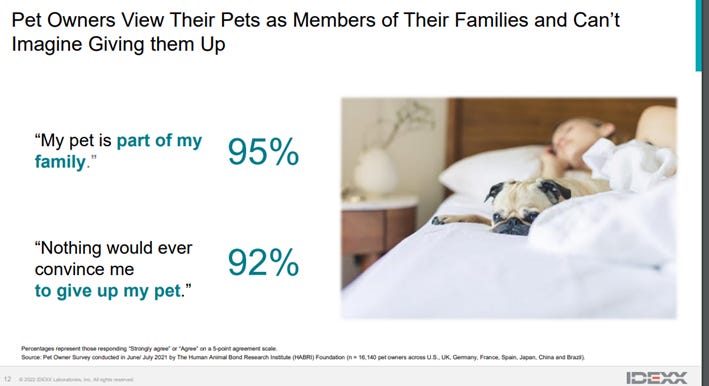

Companion animals are dogs, cats and horses. This segment is fueled by economic development, increases in disposable income, increases in pet ownership and spending on pet care. I’ll approach this from two perspectives, the economic and a more philosophical one. Interestingly, the percentage of US households with pets has dramatically increased over the past couple of decades, going from 56% in 1988 to 67% as of 2020, according to the following source.

It is my view that there is a fundamentally deep driver behind this trend. There’s a book (which I do not recommend) called Homo Deus and wrote by Yuval Noah Harari. Its thesis goes around analyzing humanity’s scientific progress. Ever since our race evolved to its current form, the vast majority of time alive has been destined towards solving global and complex issues, like sickness and poverty. However, these previously giant concerns have been somewhat ‘solved’, with extreme poverty going from 80-90% in the 1800s to less than 5% nowadays. A similar scenario has been playing out in the healthcare dimension. Consequently, humans’ minds are freer than before, allowing us to take a closer look at happiness and things alike.

At the same time, there’s a chapter from Zero to One dedicated to ‘secrets’. Thiel believes secrets are those ideas that are attainable only through very hard work. However, it would be logical to assume that secrets are, even though infinite, more difficult to uncover as more secrets are solved. The past five centuries conform a very successful story of secret-solving in all fields. Therefore, the remaining secrets are more difficult to solve than before, meaning less people will be able to do so.

Dedicating one’s life to something that’s outside the category of a secret could be considered meaningless. The other two set of ideas are conventions, easy to know, and mysteries, impossible to solve. Dedicating to both endeavors could be seen as meaningless due to, in the first case, its easiness and, in the second, its impossibility. Conclusively, there’s an ever-increasing psychological burden on humans.

There’s a book called ‘The Good Life’ which is based on the most longitudinal study of what makes up for a happy and fulfilling life. I have not read it, but heard about it several times. The discovery of the authors is that the best predictor for happiness over the long run is good relationships. The theory has been spreading all over the world now and I believe it not only applies to human relationships. Pets, or companion animals, can also be a fountain that fills people’s lives with meaning.

All of this translates into people’s willingness, with youngsters taking the lead, to spend as much as necessary to alleviate their pets’ pain. This made companies like Zoetis place more emphasis on pets, investing more money for addressing some of their untreated diseases. Consequently, overall pet’s health improved severely and, similarly to what happened with humans, pets life expectancy continues to trend upwards. This means that not only will (in my opinion) be more families adopting pets, but also increase the spend per dog, cat and horse, because of their extended life. A virtuous cycle emerges here. The more the pet lives, the deeper the human-animal bond created, and the more will owners be willing to spend.

According to World Animal Foundation, there are around 900M dogs worldwide and slightly over a half of them are kept as pets. Statista offers a more detailed view on the US, stating that there were 68M dogs as of the year 2000 and 90M in 2017. In the same line, pet dogs in Europe, according to Statista, increased from 73M in 2010 to 92M. The pattern repeats itself across regions.

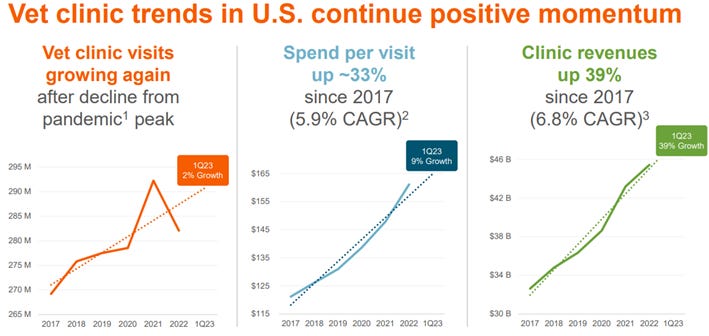

Dogs are just an example, but the same happens with cats. As a consequence of the continuous reproduction and adoption of pets, clinic visits naturally rise. Veterinarians act as a form of distributors of Zoetis’ products, for which keeping an eye on their business makes sense from an investor perspective. Moreover, it’s curious to see the spend per visit is rising as well, perhaps as a byproduct of the better solutions companies like Zoetis are developing, their greater awareness or even the human-animal bond, which might make owners consider more expensive or simply more medications for their pets.

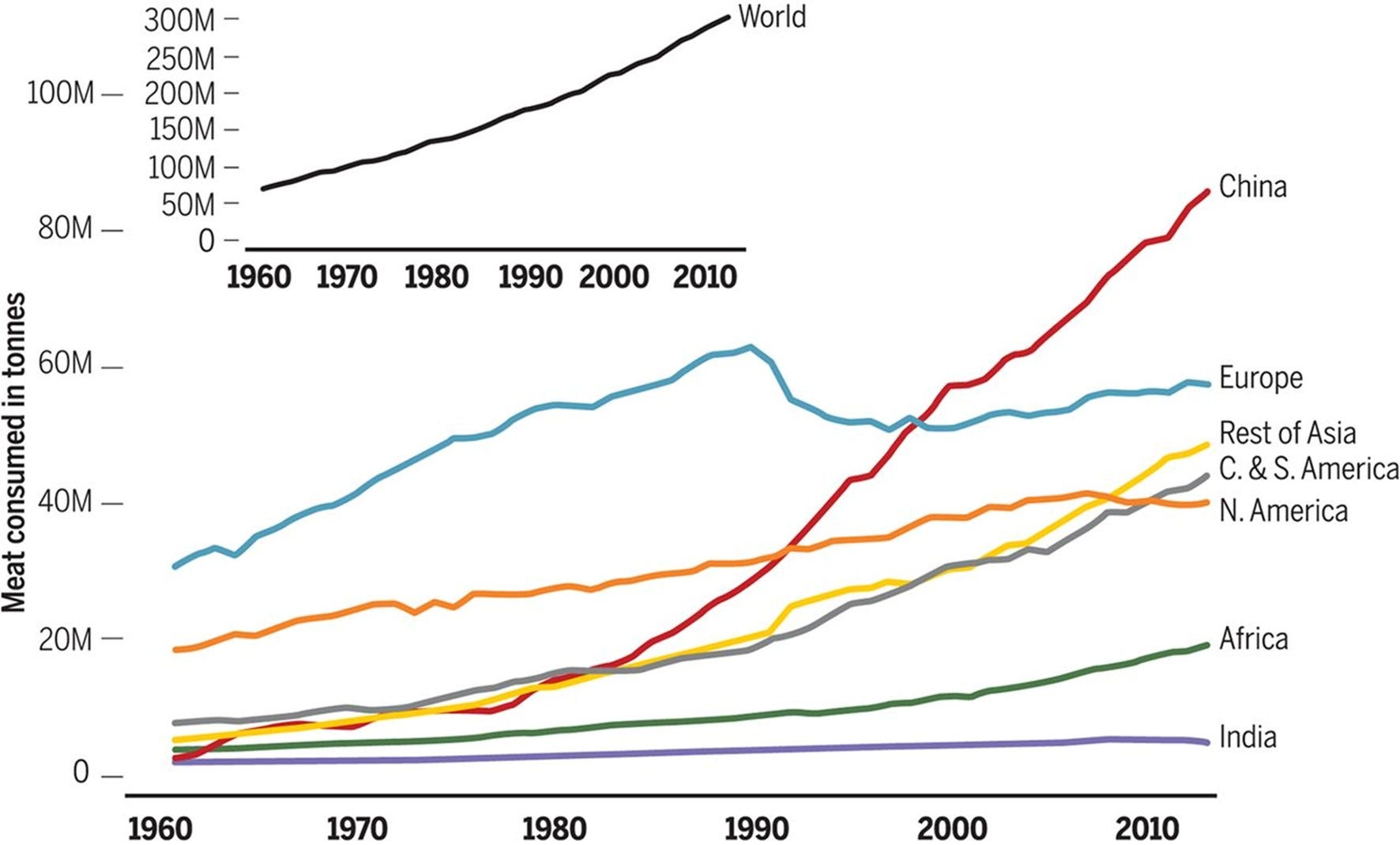

Moving past companion animals, Zoetis discovers, develops, manufactures and commercializes products for livestock as well. The company’s focus here is “on building and maintaining the health of animals that are in this space”. These help prevent and treat diseases, which enable cost-effective and sustainable production of high quality protein, for example. The demand for high quality protein goes hand in hand with the number of people alive. The more there are, the more mouths to feed.

As a reference, there were around 3bn people in 1960 approximately and 8bn as of 2023. Correlation does not imply causality, but because of the above-provided premise, it’s logical to assume at least some level of causality in this regard. Moving forward, if population continuous to grow, which seems like a valid base case for at least a couple of decades, so should meat and protein consumption.

“Livestock constitute 40% of agricultural output by price and meat production”

Moreover, GDP growth, which drives average household income up, is also a major indicator of what people consume. It has always been the case that lower income families had to eat what was at the lowest point of the food chain, in terms of price. Consequently, expensive things tended to be less consumed. With the high GDP growth the world experienced throughout the past two centuries, average household income went strongly upwards, allowing people to eat more meat, a product that has historically been somewhat scarce and expensive.

A public concern about this is that raising livestock is, according to innumerable studies, hurtful to the environment:

“Raising livestock for human consumption generates nearly 15% of total global greenhouse gas emissions, which is greater than all the transportation emissions combined. It also uses nearly 70% of agricultural land which leads to being the major contributor to deforestation, biodiversity loss and water pollution.” University of Colorado

Nonetheless, over the next couple of decades, in response to an increasing human population, overall food production must increase as well, and here’s an area for improvement. The Food and Agriculture Organization claims that over 20% of animal production losses are linked to animal diseases, which in turn affects the environment, as these are animals whom provided resources are not being utilized. Therefore, there’s this area in which Zoetis can make special emphasis on, innovation products that help increase productivity and improve livestock’s health.

“The FAO recognizes that animal health can also play a key role in both reducing greenhouse gas (GHG) emissions from livestock systems and improving food security. Healthier animals are more productive and generate lower emissions per unit of food produced.”

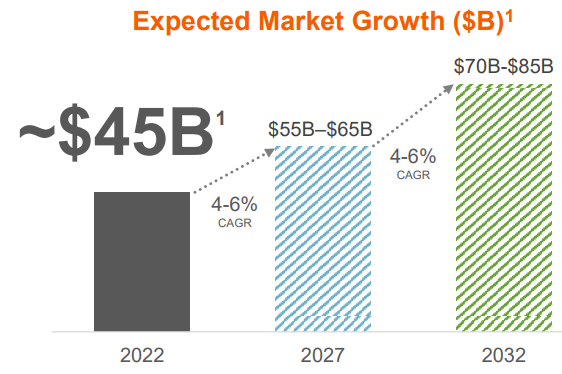

Conclusively, and to put a number to it, all of this translates into an animal health industry growing at a 4-6% CAGR for the next decade, according to Zoetis estimates. For their five years outlook, stated in the Investor Day of 2023, Zoetis ‘guided’ for mid to high single-digit growth with margin expansion.

Financial soundness

Once expressed the industry’s characteristics and Zoetis’ thesis, it’s easier to conceive why is the animal health industry resilient and non-cyclical. As shown in part 1, it got to even grow during 2008/09, the Global Financial Crisis. People’s willingness to continue paying for the well being of their pets and for food provides some sort of cushion to Zoetis income.

Moreover, many of the products manufactured and sold by Zoetis are of recurrent usage by nature. Cytopoint is a monthly injectable, Librela and Solensia are also for monthly alleviation, Simparica lasts for a month, etc, and they are bought on the basis at which they are utilized. As a result, Zoetis ends up with a large component of recurrent revenue, even if not in the strict sense.

Moving on, there has been this idea in my mind of ‘generational buyers’. In healthcare, once you find a solution that works for your pet, there is no reason why you wouldn’t simply buy such product every single month. This transforms pets into lifelong customers. Most of these diseases are always present, always a threat and almost never completely cured. Once they try Zoetis products, owners will buy from Zoetis until their pet dies.

One thing to keep in mind is the existence of generics in this market, similar to human healthcare, but of lighter presence. Once patents expire, like we’ve seen with Draxxin, competitors launch their generic medicines and can push down prices at the point of their convenience and steal customers away. These events, which whole impact is generally seen in the first 5 years, depresses the leading firm’s revenue and position. However, after and prior to this event occurring, acquired customers are most likely to become lifelong customers.

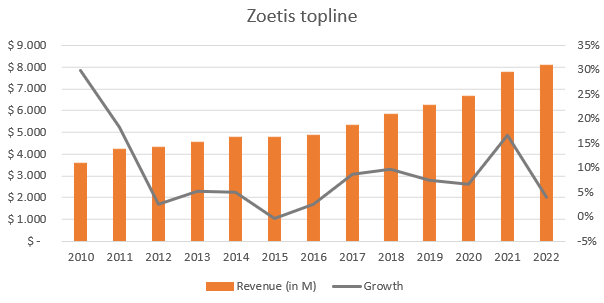

Anyhow, Zoetis revenue has grown at a 7.01% CAGR since 2010, being 8.08bn in FY 2022 and 8.2bn in the last twelve months (Q2 of 2023 results were a couple of weeks ago). The company’s historical growth goes in line with their outlook moving forward, having outgrown the industry and expecting the same thing to happen. In terms of revenue, Zoetis expects to exceed the industry’s 4-6% CAGR and grow at mid to high single digits.

Before moving down the income statement, I’ll try to distill revenue at the deepest level so that we know how it is generated. As a first parameter, revenue per geography. Zoetis directly markets its products in 45 countries and they are sold in over 100 countries. In 2013, a decade ago and first data available, Zoetis generated 61% of its total revenue from their international segment, which encompasses everything except for the US. However, last year, the company derived 3.68bn, or 46% of its revenue, from non-US countries.

This behavior is something that is further clarified when comparing the nature of Zoetis operations within and outside the United States, which we’ll address below. But some interesting dynamics I’ve observed when comparing 2013 to 2022’s revenue per country.

Australia’s revenue increased from 176M in 2013 to 289M in 2022

China’s revenue was 88M initially and 382M last year

Brazil did 313M in 2013 and 330M in 2022

US gross margin is at 80.8% while international margin is at 69.3%

Zoetis focus on selling companion animal products has been rapidly translating into their actual revenue. As of 2013, revenue generated from this animal group represented 38% of total sales, while last year, their share was of 65%, which increased 400bps on a yearly basis. In 2022, Zoetis companion animal business did 5.2bn in revenue. This puts the segment’s 12yr CAGR at 11.9%.

Geographical revenue shares, then, is not unintended. In 2013, 55% of US’ revenue came from livestock solutions, while the remaining from companion animals. Nonetheless, in 2022, 77% of US’ revenue was generated by companion animal products. On the other hand, international revenue generated something like 60-70% from livestock in 2013 and 49% in 2013. The larger input from livestock in international markets might be related to their agricultural production, caused by countries like Brazil and Australia.

Moving into revenue per category, there’s been an interesting change during the past decade. In its first annual report, Zoetis disclosed revenue generated by 6 product categories, whereas in its last one, and ever since 2017’s, disclosed 8. The two categories that the company started disclosing later were dermatology and diagnostics. Dermatology’s first disclosure was in 2017, which makes sense given the first product to hit the market was Apoquel in 2013, and diagnostics’ disclosure was in 2016, which did 38M dollars that year.

Here are the sources that generated the 7.74bn in revenue over the fiscal year 2022 (there’s a small percentage that Zoetis derives from other non-pharmaceutical products and contract human manufacturing):

Specifically:

Parasiticides did 1.86bn in revenue in 2022, growing 13.7% YoY and driven by the three strong brands with Simparica Trio being key. This puts the business unit’s 12yr CAGR at 9.9%, having done 602M in 2010.

Vaccines were responsible for generating 1.71bn in revenue, growing 2.6% YoY and exhibiting a 12yr CAGR of 4.5%.

The dermatology’s business unit ‘began’ in 2013 and started being disclosed in 2017, when it generated 428M in revenue. 5 years later, it did 1.32bn, growing 12.6% YoY and achieving a 5yr CAGR of 25%.

Anti-infectives generated 1.04bn in revenue during 2022, but have been fairly stagnant over the past decade. The business unit’s topline declined 11% YoY, affected by Draxxin’s loss of exclusivity, and has had a -0.3% 12yr CAGR.

Other pharmaceuticals, where Librela, Cerenia and Rimadyl are included, generated 1.04bn dollars in revenue last year, growing 8% on a yearly basis and mostly driven, I think, by Librela and Solensia’s launch and momentum. Measuring CAGR here makes no sense as there are continuous external shocks to the things included, like the removal of dermatology and diagnostics.

Diagnostics started being reported in 2016, when the business unit did 38M in revenue. Last year, Zoetis’ diagnostics business did 353M, down 5.6% YoY, but still exhibiting a 6yr CAGR of 45%.

Medicated feed additives generated 360M in revenue during 2022, down 14% on a yearly basis, yet still having a 12yr CAGR of 12.7%. Nonetheless, this has been a business that was at 347M in 2011, peaked at 505M in 2015 and then declined to today’s levels. Overall and removing 2010 from the equation, stagnant.

Below follows what could easily be the brightest spot of this article. In 2010 (still part of Pfizer but disclosed in their 2012 10-K), Zoetis had a gross profit margin of 63%, an operating margin of 11% and a net profit margin of 3%. In its last fiscal year, the company reported having a 70% gross profit margin, a 36% operating margin and a 26% net profit margin. That implies margins have expanded by 700bps, 2500bps and 2300bps, respectively.

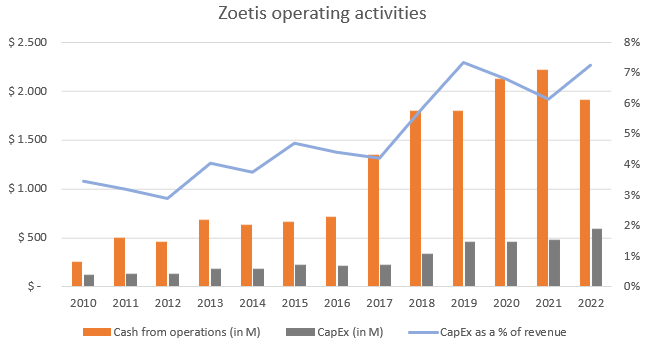

Alongside margin expansion, Zoetis has continuously increased the amount of cash it brings in from operating activities. In 2022, the company had 1.91bn cash generated by operating activities, down from 2021’s 2.2bn and from 2020’s 2.1bn. Last year’s cash from operations were down due to an increase of 120M in inventory expenditure, as the company ramps up their Librela’s storage for its launch in the US. At the same time, there was an extra 206M outflow due to deferred taxes. Contributing to this FCF’s downfall, capital expenditure was 586M, the highest ever, in line with the ‘guided’ manufacturing capacity expansion. Free cash flow was 1.32bn, down from 1.7bn in 2021.

Note: I expanded on the manufacturing capacity expansion in the previous part, you can go there for more details.

I’ll double click in the transition from 2016 to 2017, when Zoetis cash from operations grew 80%+ year on year. Since its IPO, the company had been incurring in multiple costs related to their operational efficiency initiative, ironically, and the supply network strategy. Furthermore, it was completing its separation from Pfizer which was also very costly.

“we're completing our standup from Pfizer, and that's been expensive and lengthy; we are completing – or generally completing the payments for implementing our efficiency initiative and we hope to put those behind us by the end of 2016.”

However, since 2013, management knew and had been claiming Zoetis was not operating at its natural profitability levels. On these types of claims, it is crucial to check management’s legitimacy when stating them. It helps foretell whether they are reliable or not when speaking. In any case, they called for it and it turned out to be true. Thereafter, Zoetis cash from operations never got below the new threshold.

“2016, we don't really demonstrate through our quarter results the real cash-generating properties of our business. 2017 will be the first opportunity for the market to see in our reported results the ability of this company to generate significant free cash flow.”

Going back to capital expenditures, Zoetis has been thoroughly focusing on companion animals both from a CapEx and R&D standpoint because of the segment’s expected outperformance. To this end, for instance, Zoetis developed and is now expanding its manufacturing capacity of Librela and Solensia. However, it’s not only growth what the company is after. Management recognized that products for companion animals can be sold at higher margins, which is the reason why they believe and are still guiding for margin expansion. Librela and Solensia are a perfect example of this, as well as the US business margins, compared to international.

Finally, Zoetis holds in its balance sheet 1.7bn in cash and equivalents, down from 3.5bn at the end of last year. The reason for this drop was “primarily attributable to the repayment of the $1.35 billion aggregate principal amount of our 2013 senior notes due 2023 in February 2023” and perhaps the increased inventory. Out of the 6.5bn long-term debt remaining, 1.35bn will be maturing in 2025, 750M in 2027 and 4.55bn thereafter.

“When you look at the current level of operating cash flow that we have and the strength of our balance sheet, we're able to fund almost the full consideration and still stay within our targeted gross debt to adjusted EBITDA range of 2.5 to 3. So that still leaves us the financial flexibility to fund future strategic investments and also return cash to shareholders through dividends and share repurchases” Q2 2018

A diversified business model

To wrap it all up, the following image aims to illustrate where does Zoetis derive revenue from. It breaks it down as we did above; per major product category, geography, and animal group.

Zoetis sells around 300 product lines that cover 5 major product categories and multiple more but with a smaller reach. It sells to more than 100 countries and 8 species. Moreover, Zoetis’ two largest customers are distributors, and accounted for 14% and 9% of the company’s revenue in 2022. It seems safe to conclude that, even if within the animal health industry, Zoetis has very diverse sources of income and not much exposure to single clients.

Capital allocation skills

A large component of capital allocation in this industry is in line with research & development and CapEx. We’ve thoroughly covered Zoetis R&D model and its results in the first article. A couple of bullet points that help visualize management’s ability to allocate capital:

Zoetis built the dermatology market up, launching Apoquel in 2013. It now has a 1.3bn monopoly still growing at double digits.

Launched Simparica Trio, a first of its kind triple therapy, which is now at multiple hundreds of million in revenue.

Launched Apoquel’s chewable version in 2020.

Launched Librela and Solensia, disrupting the OA pain market and going from 0 to a 250M run rate in 2 years, with an expected peak of 1bn in sales.

Developed and delivered 9 out of its 15 blockbusters after IPO.

Received over 2,000 patent approvals in a decade.

Expanded gross profit margin, operating margin and net profit margin by 700bps, 2500bps and 2300bps, respectively.

Outgrew the industry and expects continued outperformance due to the investment focus on companion animals.

It expects continued margin expansion due to its investment focus as well.

In a more concrete manner, Zoetis had a 47% return on equity, 13% return on assets and 18% return on invested capital in 2022. Over the past decade, it has averaged 49%, 12% and 16% respectively. It is worth mentioning that the high ROE is partly due to the decently sized debt position Zoetis has. Lastly, management mentions in all 10-Ks how crucial of a role does return on invested capital plays on the decisions they take.

“We are making these investments that are prioritized with the highest returns on invested capital… , but also at enhanced margins that drive ROIC accretion as we have done historically” Investor Day

Besides return on investment and initiatives that would drive higher-than-industry growth, Zoetis has a simple framework for deploying capital. Management firstly prioritizes internal opportunities, which consist mainly of R&D, reach expansion with things like direct-to-consumer advertising and increasing manufacturing capacity. All of these help drive organic growth for Zoetis. We could add their occasional inventory build-up, but this works more of a cushion for expected demand. I don’t see it as a way to achieve sustainable growth. Secondly, once high ROIC internal investments have been exhausted, the company looks at M&A which we’ll go over below. Finally, once Zoetis got to create the most amount of value, it looks to return it to shareholders. Each step of this framework was repeated by management in almost all conference calls by both the former and current CFO.

When returning value to shareholders, management stated in multiple years their preference for share repurchases rather than dividends.

“we continue to prefer share repurchase as it does give us flexibility to execute on our other capital allocation priorities” Q1 18

The reasoning behind it is the flexibility these offer, which helps them better decide where to allocate capital. If management believes internal investments make more sense, then they destine less capital to buybacks. On this point, Zoetis approach to buybacks appears to be mostly about consistency with occasional spikes. It’s not the best strategy in my opinion, but not the worst either. Ideally, management would only buy back shares below intrinsic value, but the following chart might somewhat illustrate their willingness to step up if necessary.

Note: Zoetis paused its buyback plan during Q2-Q3-Q4 of 2020 due to COVID’s uncertainty.

“So what drives that flex? It's a combination of the rhythm of the internal investments. So in a year where we see CapEx at a billion dollars for the company, that might translate into slightly less share buybacks. In the years where it's not, you may see a little bit more, but we also look at the timing of M&A transactions and we look at the intrinsic value of our stock compared to our internal long-term growth aspects and the broader markets to drive when we opportunistically flex on the level of buybacks that you see from us” Investor Day 2023

Before going into the last part of this capital allocation analysis and of the article, a chart illustrating buybacks done and dividends paid to shareholders over time. Both help better depict levels and management’s intention.

Acquisitions

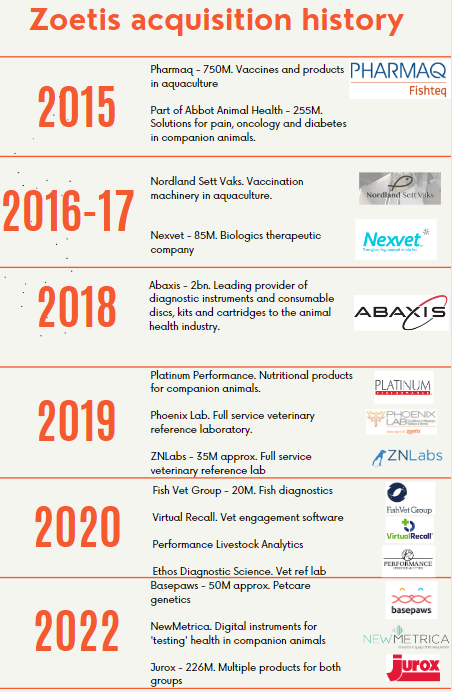

Mergers and acquisitions have always been a solid option for Zoetis’ capital deployment. The company utilizes M&A to enhance its current portfolio with more offerings and to expand market reach, mainly. Nonetheless, Zoetis also acquires companies with the intention of horizontally growing its portfolio, setting foot in new areas, like it did with diagnostics.

“External partnerships and acquisitions are also important for innovation and providing us new capabilities to predict, prevent, detect, and treat disease in animals.” Q2 18

“So we remain focused on M&A. We evaluate many opportunities, and we will look to continue to use that as a primary area for capital allocation moving forward.” Q1 21

“Our M&A approach is disciplined. It is focused on driving value creation opportunities within our core, giving us access to enabling technologies and driving innovation” Investor Day

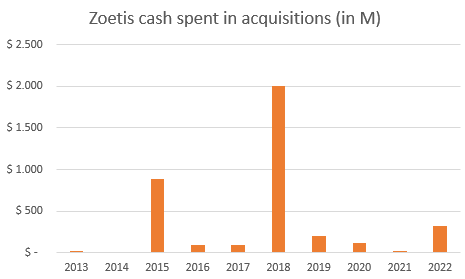

Curious finding here. Management’s narrative is that their approach to M&A is similar to the one of buybacks, consistent buying with occasional big purchases. In Q1 of 2020, they said “our focus is on strategic tuck-in acquisitions, not large scale transformational M&A”. Since IPO, Zoetis has acquired something like 15 companies, with the three largest accounting for a combined 3bn out of the 3.8bn spent in total. However, it’s true that none of these have been transformational. Abaxis, the largest one, had 240M in revenue in 2017 (4.5% of Zoetis rev) and was a ‘pure-play’ in diagnostics.

To finalize this research article, we’ll go over some of Zoetis acquisitions, but before that, an image I put together to help visualize Zoetis acquisition history.

Abaxis, Zoetis move into diagnostics

Zoetis paid approximately 2bn dollars for Abaxis in 2018. The latter was founded in 1989 by Gary Story, Richard Leute and Vladimir Ostoich, from whom only Leute remains involved as a consultant, according to Wikipedia. Abaxis ‘develops, manufactures and commercializes portable blood analysis systems that are used in a broad range of medical specialties in human or veterinary patient care to provide clinicians with rapid blood constituent measurements’. Their two main products are point-of-care instruments and consumables for the medical and veterinary market. An important thing is that “our business and revenue model is focused on recurring revenue”. It was with this acquisition that Zoetis started reporting their diagnostics business in 10-Ks.

In 1994, the company introduced its first product, the VetScan. VetScan VS2, the newest version, ‘is a chesmistry, electrolyte, immunoassay and blood gas analyzer that delivers results from a sample of whole blood, serum or plasma’ that it’s sold to veterinary market segments.

Moreover, Abaxis manufactures and commercializes VetScan Profiles, which are the consumables VetScans use. In 1995, Abaxis launched its first product for humans, Piccolo. It is still commercialized today and, for what I see in Abaxis’ 2017 10-K, it’s more or less the same thing as the VetScan, but for humans. In the same fashion, Abaxis also manufactures Piccolo Profiles.

Zoetis management recognized the big addressable market diagnostics have and that it still offers a great opportunity moving forward. Since the company had no real presence in the market, management decided to make this large acquisition.

“During the year, we made our largest acquisition to-date purchasing Abaxis for $2 billion in the fast-growing point of-care diagnostics space. We see diagnostics as an important area to broaden our portfolio, and we have tremendous growth opportunity ahead, especially in international markets.” Q4 18

“We've used M&A as well to move into areas that are complementary to our core business, like we did with the Abaxis acquisition” Investor Day

To expand its presence, Zoetis started a lab acquisition spree, observed in the acquisition history image. In 2019, it bought Phonix Lab and ZNLabs, both of which were decently sized networks of full service reference laboratories. The market was previously a duopoly, where Idexx and Antech dominated. Allegedly, the former offered to pay 29M for ZNLabs, which was then overbid by Zoetis’ 35M approximately.

"This is huge in an industry that's been dominated by two players for far too long." Gardiner, co-founder of ZNLabs

“This acquisition brings Zoetis a company that has a proven, competitive diagnostic platform for growth that we can help to accelerate in the U.S. and worldwide with our global scale and direct customer relationships in approximately 45 countries,” Zoetis former CEO

In 2020, Zoetis acquired another full service reference lab, Ethos Diagnostic Science, for an undisclosed amount. Ethos performs testing for all veterinary species in wide variety of verticals. The acquisition helped Zoetis expand its reach even more and offer a more holistic portfolio of offerings to clients. Moreover, these 3 lab acquisitions are a fundamental complement to Abaxis.

“Reference laboratories and point-of-care diagnostic testing are highly synergistic, offering veterinarians a single source for a full spectrum of tests, as well as access to the expertise of board-certified specialists and pathologists to support test results.”

“In the last part of 2022, despite the COVID lockdowns, we opened two diagnostic reference labs in Beijing and Shanghai with 200 plus test capabilities available, open day one of our opening.” Investor Day

Finally, Zoetis diagnostics business unit is currently at 350M in annual revenue. Keep in mind that human-related offerings Abaxis had are not included here.

Pharmaq and Zoetis’ emphasis on aquaculture

In 2015, Zoetis announced it had reached an agreement to acquire Pharmaq for 765M. The company was privately held, based in Norway and had approximately 200 employees at that time while it now has around 380. Furthermore:

“PHARMAQ is the market leader in sales of vaccines for farmed fish, a market segment growing 10% annually. The company generated revenues of approximately $80 million in 2014 and has a presence in the major aquaculture markets in the world. PHARMAQ revenue grew at a compound annual growth rate of 17% from 2005 to 2014”

Pharmaq product categories are immune support, biocider, injectable vaccines, therapeutic products and bath/immersion shots. It has operations across 25-30 countries, mostly EU, and offers solutions for 9 species like catfish, shrimps, salmon. At the same time, Pharmaq has a diagnostic laboratory that offers pathogen detection and advisory services. With this acquisition, Zoetis set foot in the only significant area in animal health they were not participating.

In the third quarter of 2016, Zoetis’ management increased their 2017 guidance by 175M in revenue, ‘driven by the acquisition of Pharmaq’ and some other things. We could hypothesize that Pharmaq’s revenue was around 100M. More importantly, it is a company that as of 2015 “has been supporting a substantial investment in R&D and continues to be a profitable business”. In terms of what it brings to the table, Juan Ramón Alaix said the following.

“The acquisition strengthens our core business in three key ways. PHARMAQ expands our customer base into the farm fish segment, it adds to our diverse portfolio a leading vaccine for farm fish and innovative parasiticide as well. PHARMAQ is the market leader in vaccine for farm fish, a market growing 10% annually. And finally, it expands our R&D program in aquatic health, with a strong late-stage pipeline expected to deliver new solutions to the market in the near-term. Zoetis has an excellent track record of identifying and integrating their businesses, and this one meets all our criteria in terms of strategic fit and value” Q3 15, Zoetis former CEO

Most acquisitions are characterized by the cost of synergy they have, when being integrated. Integrating a company that doesn’t have proper S&M, R&D or some other activity requires the acquirer to provide such resources so that the acquired can excel. In this line, when asked, management recognized this is not the case:

“this is not like a classic cost synergy deal; this is a transaction that puts us squarely in a space that's going to grow quickly, that comes to us with a well-developed pipeline featuring near-term opportunities to continue the attractive growth that they deliver” Q3 15

To further consolidate Pharmaq’s position, Zoetis acquired Fish Vet Group in 2020 for an undisclosed amount, but approximately 20M according to internet. In fact, the company is based in Scotland, but also operates in Norway, and was announced as a direct addition to the Pharmaq business. Fish Vet Group offers diagnostic technologies, environmental monitoring and training, PCR testing and services in bacteriology. Additionally, it helps fish producers meet environmental standards.

“Farmed fish is one of the fastest growing sources of animal protein” 2020 article.

Fish Vet Group was then merged with Pharmaq and rebranded as Pharmaq Analytic in 2021 for both of them to proceed as a single entity. This segment would now operate diagnostics and reference labs.

Zoetis’ revenue coming from its fish business was 212M in 2022, growing 13% YoY and at a 15% CAGR for the past 6 years. It continues to show momentum and management has mentioned the business had great quarters in almost all conference calls.

“The fish portfolio benefited from the continued uptake of the Alpha Flux parasiticide in Chile” Q1 20

“Finally, our fish portfolio continues to perform well with double-digit operational growth driven by strong vaccine performance in Norway” Q1 23

Hypothesis

In 2017, Zoetis paid 85M for NexVet, a biologic therapeutics company with this on the pipeline:

“Nexvet’s pipeline product ranevetmab (a mAb targeting nerve-growth factor (NGF)) for pain treatment for dogs would, upon approval, be the industry’s first monoclonal antibody therapy administered monthly by injection for chronic pain”

In a scientific article, I found this:

“Monoclonal antibodies against something like NGF are species-specific. For dogs, the current versions are ranevetmab and bedinvetmab (brand name Librela), which have already been approved in the European Union for use in dogs. Studies have shown that one injection of these compounds leads to an improvement in comfort and mobility for at least eight weeks. The dogs are better off than if they had been given nonsteroidal anti-inflammatories (NSAIDs), which have been the mainstay drugs for osteoarthritis.”

Hypothesis: It’s very likely that Librela and Solensia’s discovery and manufacturing was a byproduct of NexVet acquisition. This means that Zoetis paid 85M for a pipeline that’s now at a 250M run rate and it’s expected to reach 1bn in sales.

Personal commentary

I really enjoyed covering Zoetis, but I believe this will be the last research article for a while. I need to dive into other companies. Hope you enjoyed these 3-part research and it’s very likely that I follow a similar structure for future companies.

Disclosure: This is not financial advice.

Thank you so much for this. A beautiful analysis indeed.

Great finish to a wonderful research and series. This 3 parts research reinforce my thesis in the company and management. Thank you for the work you made on this one. Looking forward for your next idea and maybe, exchange topics on this one too. Take care!