In the first part of Zoetis research, we covered the business’ core, their R&D model. We dived into how it’s structured, how it works, how it’s funded and what the results have been. Additionally, a detailed analysis of three of Zoetis’ main products was included. I highly suggest you check that one out before this article as there is an implicit thread I try to follow so that everything makes sense.

Industry

Zoetis belongs to the animal health industry. It would be normal (happened to me) to think this industry is very much alike the human health. But it truly surprised me how much they differ from one another, having the animal health industry undoubtedly better fundamentals for incubating long-durable companies.

The first point I want to highlight is regarding patents. A patent is a governmental grant of a temporary right to exclude others from making, using or selling a claimed invention. In both industries, patents tend to last for around 20 years after the filing date. After the required bureaucracy for granting it, perhaps the patent is left with 17-18 years of utility. Even though this is similar in both ends, there is a huge difference after they expire:

“In human health when you lose patent exclusivity, your revenue erodes by 90 percent within the first year”... “In animal health when a drug loses exclusivity, it might take five years to have an erosion of between 20 to 40 percent.” Juan Ramón Alaix, Zoetis former CEO

I was truly amazed by the statement, which made me research further. Unfortunately, there is almost no information about the animal health industry, but I grabbed three keypoints of the human’s from three different papers:

A study indicates that drug prices decrease significantly after patent expiration, ranging from 6.6% to 66% after 1-5 years after the patent’s loss of exclusivity (LOE).

Another study showed that the median drug price after patent expiration decreased by 41% after 4 years.

The last one showed that after one year of patent expiration, an average of 17.2 producers enter the market. After two years, 25.1. This made the former leader lose a lot of market share and profitability in a brief period.

On the other hand, the lack of players in the animal health industry make a patent expiration event not that crucial. Furthermore, relationships between competitors are mostly rational. The ones that enter a market with a generic drug generally don’t push prices too low because of the industry’s dependence on margins. There’s not a lot of volume in the animal health industry, making drug prices a vital contributor to the bottom line. Additionally, Zoetis management claim this to be a market where pet owners, veterinarians and livestock producers loyalty is very determinant as well. When a patent expires, they tend to stick with the same company. Therefore, companies that earn their trust and goodwill enjoy a long period of recurring selling to them.

Here’s an example of recent patent expirations regarding Draxxin, Zoetis’ largest product in cattle and, to some extent, swine. Prior to Draxxin’s lost of exclusivity, the product was at roughly a 300-350M run rate.

“with respect to Draxxin, we expect it to have about a 20% impact to the top line in the first year, and another 20% in the second” Q2 2022

“The first year was slightly better than our expectations, coming in somewhere around 16% decline, but the second year was little bit worse. So I think we're sort of in that ballpark. I think second year was about 25%” Q4 2022

“We continue to see some impact on Draxxin, but not meaningful, not at the level that we've seen previously,” Q1 2023

Going back to the competition front, one peculiarity of this market is that, unlike human health, there is no large and well-capitalized company that globally competes by focusing on generic products. The reasons for this are the relatively small market size of each product, the importance of direct distribution (direct to consumer, covered later), the self-pay nature of the business and that these products are often directly prescribed and dispensed by veterinarians.

“Phillips said 75% of animal health products have market sales of $1 million/year or less, which isn’t much incentive for a company to go through the development and approval process”

“many were surprised when Alaix described the animal health business as having nearly zero involvement by third-party insurance payers. “Our customers are veterinarians and livestock farmers, and when they make the decision to buy, they are also paying for their purchase”

On a final note, gross margins in the animal health industry are around 60-65%, much lower than in human health. This makes companies that want to compete with generic products more interested in the human health industry because there is a lot of space to compete on price and still be profitable. There is not that same opportunity within the animal health industry, margins don’t allow it.

The lack of competition makes disruption a rare event. Big markets are generally oligopolies and Zoetis leads and has monopolized many small-mid ones. Consequently, products tend to have a very enduring life, helping Zoetis get abnormally high rates of return from its investments.

“our top 25 products have an average time in our portfolio of 27 years, demonstrating our ability to build enduring product franchises.” Annual report 2014

“The average market life of our product is 30 years.” JPM conference, Jan 2023

Moving forward, the R&D process in the animal health industry is much less costly than in the human industry. When beginning research of a particular disease that could affect several species, Zoetis opts for the one that drives the highest success rates. At the same time, clinical trials are shorter in time, leading into lower costs and faster development timelines. Cycles tend to be 2-3 years faster in animal health. Additionally, there is a lot of room, as seen in article 1, for lifecycle innovation, which also contributes to higher success rates. Nevertheless, Zoetis first researches what it could develop and ask customers if they’d pay for such thing, leading to a much lower development risk. All of this translates into the following:

“It's not unheard of to spend hundreds of millions of dollars, over a billion dollars to bring a new product to the market in human health. For the animal health R&D element of our work, we are more in a range of about tens of millions of dollars to bring those new products to the market” Investor Day 2023

Both industries further differ. From what I’ve seen, human health companies focus mainly on product development and drug discovery, which can take a long time:

“Our R&D Pipeline. The process of drug and biological product discovery from initiation through development and to potential regulatory approval is lengthy and can take more than ten years.” Pfizer 2022 10-K

Even though there are mentions of things like increasing product’s ease of consumption, the focus is on pure discovery. Zoetis, on the other hand, has a high percentage of investment destined towards lifecycle innovation. This is much more predictable, which helps the animal health industry grow at steady and continuous rates. Lastly, it is extremely resilient. Part of the reason for this is that, increasingly, more and more people are viewing pets as family and studies show these people would almost always pay what it’s needed to keep them healthy. Even in scenarios where they saw their income decimated.

Another difference between both industries is the required infrastructure to reach customers. This one can also be seen as a huge competitive advantage Zoetis has, and a tall barrier for competition to cross. In the animal health industry, companies need a very extensive sales force. Their role includes:

Visiting customers to provide information, promote and sell products and services.

Technical specialists provide scientific consulting to veterinaries, training and education on product use. They also partner with customers to provide further support and training in areas of disease awareness and treatment protocols.

Pet owners are taking a more active role in product purchasing decision, so Zoetis is investing in DTC marketing efforts.

Conclusively, this translates into longer sales and consulting visits, consequently leading to the need of having a large sales force. As a reference, out of Zoetis 13,800 employees, 4,200 (30%) belong to sales. Pfizer, on the other hand, had around 14% of their total employees on its global sales force in 2016 (last piece of data I found).

Opportunity for small monopolies

We covered in last article what Librela and Solensia were used for. An interesting takeaway from the osteoarthritis (OA) case is how old the problem was and how much it lasted without any solution.

“Curiously, the first registered case of OA is of a dino-bird that lived 130 million years ago. As for dogs, the oldest case traces back to 14 thousand years ago.”

Diseases, sicknesses, virus and all these infections that affect animals are not infinite, but definitely numerous. Furthermore, the amount of variations each of them has, not only within the same specie, but also from specie to specie, makes a large universe of ‘problems to tackle’. Because resources destined to healthcare have been mostly utilized to engage with human-related diseases, the animal health industry still has multiple unexplored verticals.

On dermatitis, treated by Apoquel and Cytopoint:

“Roughly 2500 years ago, the Ancient Greek physician Hippocrates was the first to describe the condition of the chronically itchy skin. “

Although this extract refers to humans, there’s almost no reason to think this was not happening with animals as well. This skin disease was not treated in animals practically until Zoetis launched Apoquel in 2013. Both of these cases illustrate how ancient some of animal health issues are. However, they’ve never been properly attended. For every unattended disease, there’s room for Zoetis to, first, go after a vertical with a known problem. Secondly, since there’s no current solution for these problems, that means there’s also no competition. If Zoetis correctly develops a substance capable of addressing these issues, they will hold an at least short-mid term monopoly over the vertical.

See how each of the following products are “the only”, “the first”:

In many businesses, it can be a problem to identify new problems to solve so that the company’s services create more value for customers. In the animal space, many problems have been identified for decades now, which, by itself, I believe adds some more predictability to R&D. It’s not blind R&D, there are clear objectives and rewards are monopoly-like positions in products that might earn revenue for decades.

Competitive positioning

“Our primary competitors include animal health medicines, vaccines and diagnostic companies such as Boehringer Ingelheim Animal Health Inc., the animal health division of Boehringer Ingelheim GmbH; Merck Animal Health, the animal health division of Merck & Co., Inc.; Elanco Animal Health; and IDEXX Laboratories. There are also several new start-up companies working in the animal health area. In addition, we compete with hundreds of other producers of animal health products throughout the world.”

Boehringer Ingelheim Animal Health

Boehringer is a family-owned, German and, unfortunately, private company. The company operates as a conglomerate of segments, like Pfizer. It was founded in 1885 and, as of today, it’s the largest private company within the pharmaceutical space with 47 thousand employees.

Their animal health business unit operates with 9,500 employees and serves 150 markets worldwide. They are one of the largest providers of vaccines, parasiticides and therapeutics, complemented by diagnostics and monitoring platforms. The company has a strong presence in both large categories of animals: companion and livestock.

Merck Animal Health

Merck is a global health care company that’s involved in prescription medicines, including biologic therapies, vaccines and animal health products. The animal health segment has 6,000 employees (ZoomInfo) and ‘discovers, develops, manufactures and markets a wide range of veterinary pharmaceutical and vaccine products, as well as health management solutions and services, for the prevention, treatment and control of disease in all major livestock and companion animal species’. The company also offers an extensive suite of digitally connected identification, traceability and monitoring products. As Zoetis, it sells its products to veterinarians, distributors, animal producers, farmers and pet owners.

Elanco Animal Health

Elanco was a business unit that operated under Eli Lilly. The spinoff took place in 2018 and Elanco has been independent ever since. As both previous companies, it offers products in many shared verticals and to the two largest groups of animals. The company has around 10 thousand employees.

IDEXX Laboratories

IDEXX was incorporated in Delaware in 1983. Even though it is mentioned by Zoetis as one of their competitors, Idexx is mainly focused on diagnostics and testing, making it not a whole-spectrum competitor. Given I found the company interesting, I’ll provide some more details. Most info is from their 10-K, which is beautifully put together.

Overall, the company develops, manufactures, and distributes products and services primarily for companion animals, livestock and poultry, dairy and water testing industries. Additionally, Idexx provides human medical point-of-care and laboratory diagnostics. Within each segment, the company offers:

Companion animal group diagnostics: Idexx provides diagnostic capabilities that meet veterinarians’ diverse needs through a variety of modalities, including in-clinic diagnostic solutions and outside reference laboratory services. The curious thing about their diagnostics revenue is that a large part is recurring in nature. This segment generates a total of 3.05bn, out of which 2.6bn is diagnostics recurring revenue. CAG diagnostics operates at a 26% margin.

Water quality products: Idexx provides testing solutions for detection and quantification of various microbiological parameters in water. The water segment generates 155M in revenue and has a 46% operating margin.

Livestock, Poultry and Dairy: LPD provides diagnostic tests, services, and related instrumentation that are used to manage the health status of livestock and poultry to improve producers’ efficiency and ensure quality. LPD generates 122M in revenue and has a 16% operating margin.

Competitive landscape

The animal health market was estimated to be at 45bn dollars in 2022. Zoetis performed the estimate based on industry data for core animal health market and diagnostics, genetic tests and biodevices. Aforementioned companies generated:

Merck’s animal health segment has 5.5bn in revenue

Elanco did 4.7bn

Boehringer’s animal health division, 4.6bn (in Euros and FY 2022)

Zoetis did 8.1bn in revenue

Idexx Laboratories generated 3.3bn

This results in the following market share as of FY 2022:

The chart might be slightly off due to the amount of product diversity these companies might have, plus some services that large corporations might not directly include in their animal segment. Leaving this aside, Zoetis is the clear industry leader and seems as if this has been the case for the past decade.

Since going public, Zoetis has managed to continuously outperform its peers, growing its share in the animal health industry. In 2013, the company had an approximate market share of 15%, meaning it has increased its presence by around 240bps.

Competition on patents

A very straightforward parameter to estimate companies’ presence in the industry, beyond revenue, is patents. They give an indication of how big of an intellectual powerhouse these companies are. Moreover, since patents grant exclusivity over certain products/solutions/discoveries, observing how many they have can help get a grasp of how protected their revenue is. There’s a lot of nuance though, as patents differ in quality, but, overall, it is a decent proxy.

Out of the five core players, only two of them disclose the number of patents they have in their 10-K, Zoetis and Elanco. There are some websites specialized in patents, like Greyb, which provide information in this respect, but it is mostly false. There’s a mismatch between the number it presents and the one Zoetis itself reports in their 10K. Likewise with Elanco.

Both companies seem to have a decent portfolio of patents (independent of Elanco’s strangeness in data). Again, there’s a lot of nuances with respect to the quality of each company’s IP and, given my lack of expertise, I cannot get into such details.

Market-specific

From a market-specific standpoint, Zoetis leads in almost all of the ones it participates in.

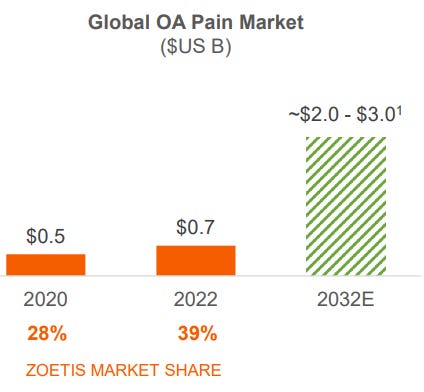

Diving a bit further, Zoetis holds a 25% market share in the parasiticide market at a 1.8bn run rate; a 95% market share in the dermatology market at a 1.3bn run rate; a 39% market share in the OA pain market at a 200-250M run rate (expected to rapidly grow when Librela gets released in the US); a 13% market share of the vaccine market at a 1.7bn run rate.

A leading position in markets accompanied with the best sales network makes Zoetis a key provider to many veterinarians and third-party veterinary distributors. Consequently, further fueled by the particular brand value products adopt in the animal health space, Zoetis advantage translates into pricing power.

One last thing I want to mention with regard to competition is the scarce visibility companies have with respect to what others are doing. I believe that, because the nature of this game is to work in secret projects until they reach the patent-level (which is when they are revealed), Zoetis cannot know what competition is working in. Furthermore, the whole space is composed of only two large players dedicated 100% to the animal health space. Boehringer and Merck are large companies that have business units in the industry, but they still belong to these large corporations. This, combined with the fact that the space is filled with under-the-radar startups working in disease-specific solutions, makes Zoetis not capable of correctly assessing competition’s capabilities nor pipeline.

“Now, we're never sure about when competition's coming”

“First of all, the timing of competition is never certain, but we're not resting on that. We're continuing to innovate”

“we never have real precision in terms of when competition's coming”

Singular remarks

A high degree of Zoetis’ attention goes to customers satisfaction, with one of their values being ‘customer obsession’. Each company’s product signify a unique experience for customers. Therefore, satisfaction with the service differs across companies. Ultimately, people will buy what they like the most, the experience they enjoyed more, or buy to the people that treated them the best.

“Customer satisfaction or CSAT scores, which as you can see here, are incredibly strong, of 80 and 81. But I'm really most proud of net promoter score, which is if you ask a customer of ours, "Would you recommend us to your friend?" And we have some of the highest scores, 60 in the US and 60 outside the US, but importantly, we're significantly ahead of all of our animal health competitors.” Investor day

Management realizes how vital showing tangible signs of caring towards their customers is, and more so considering the role brand value plays within the industry. In pursue of customer satisfaction, Zoetis offers a refund or product replacement if the person is not ‘completely happy’. What I particularly like about the framing is that it definitely feels like a friendly message, meaning that the company pays attention to those details as well.

Simparica and Simparica Trio are one of the three products we covered in the first article, which belong to the parasiticides market. Simparica Trio is at a 600M revenue run rate as of Q1 of 2023, being one of the biggest contributors to Zoetis topline. Trio supposes a mix of disruptive innovation mixed with lifecycle innovation; a triple therapy is a novelty in the market, but one of the ingredients derives from Simparica. The other two big products Zoetis has in parasiticides are the Revolution and Stronghold brands, both of which we’ll cover in a future article.

The company was a first-mover with Simparica Trio. Here's what management said with regards to competition and what makes Trio unique:

“we've been expecting competition for a TRIO for some time, right? We're now into our third, if not, we're going to be crossing into our fourth year on the product that we've been in the market, we're first to market in the largest parasiticides market in the world, in the US”

“I will stress, though, that TRIO, given heartworm is among the parasiticides that it covers, heartworm is the deadliest. And we have 100% efficacy on heartworm after the first dose. That's an important factor that I want to stress with respect to our products. And again, we'll see what the competition comes out with, but we're very confident in our position and our ability to continue to grow TRIO.”

The second category we thoroughly covered is Dermatology, composed mainly of Cytopoint and Apoquel. Zoetis basically built the market up and now holds an authentic monopoly over it.

With regards to competition and the products’ momentum, here’s management commentary:

“Look, we grew 17% operationally, after a 23% growth year and the growth over the prior two years. I wouldn't expect that level of growth, but I would expect double-digit growth to continue to come from our derm franchise. And we're not expecting competition to be launched in 2023 across derm. So another year of continuing to drive. And even beyond competition, we expect to continue to grow the product. We continue to innovate across this franchise as well.”

The Osteoarthrtitis (OA) pain market is the last one we made special emphasis on. Zoetis developed and manufactured new recipes that brought innovation to a space that was quite sterile. With these new introductions and the ones in Zoetis’ pipeline, the market is now expected to rapidly grow for the next decade.

The company currently holds a 39% market share, but with a remaining expected run rate of 800M for only Librela and Solensia, meaning Zoetis aims to have at least 50-60% market share by 2032.

Manufacturing and supply chain

As aforementioned, one of the barriers that keep many companies out of the animal health industry is the necessity of a proper sales team, an orchestrated supply chain and manufacturing capacity. Zoetis products are manufactured at sites operated both by themselves as well as third-party contract manufacturing organizations (CMOs).

Zoetis self-manages a global network of 29 manufacturing sites. Twelve out of the 29 are located in the US, while most of the remaining in Europe, a few in Oceania, 2 in China and one in Latin America (Brazil). Out of these 29 sites, Zoetis owns the majority of around two thirds of them, while the remaining are being leased. Overall, Zoetis counts with 132 CMOs, including those centrally-managed and others locally done so.

In order to select each of these, the company considers:

Their capacity

Their ability to reliably supply products of high quality and at optimized costs

Access to niche technologies and products

How efficiently they operate

In pursuit of operational efficiency, Zoetis has been reducing the number of contract manufacturing organizations it works with. There is no mention whatsoever of why exactly this could be happening.

“As a result of a review of our global manufacturing and supply network, we have announced plans to exit or sell certain sites and have exited eight manufacturing sites since 2015, including Yantai (China) and Guarulhos (Brazil) in 2017”

“we regularly inspect and audit our global manufacturing network and CMO sites. As a result of a review of our global manufacturing and supply network, we have exited eight manufacturing sites since 2015.” 2018 10-K

Management has always communicated their intention of always maximizing efficiency. There are several reasons why I believe Zoetis could have reduced their CMO network:

In 10-Ks, it has been sometimes mentioned the continuous audits Zoetis realizes to their manufacturing sites. As a byproduct of perhaps spotting inefficiency, the company might have been cancelling third-party contracts to concentrate production on sites that operate at high standards.

A larger percentage of product manufacturing might be shifting towards in-house sites. Not being oneself who performs the manufacturing makes the company dependent on third parties, which is not always desirable. It makes Zoetis lose control over their products and perhaps it is in pursuit of higher vertical integration that they are doing this.

“We believe that animal health customers value high-quality manufacturing and reliability of supply. The importance of quality and safety concerns to pet owners, veterinarians and livestock producers also contributes to animal health brand loyalty, which often continues after the loss of patent-based and regulatory exclusivity. We depend on positive perceptions of the safety and quality of our products by our customers, veterinarians and end-users.”

There was a slight change to how Zoetis speaks about the number of product lines they have. It seems as if, over the past decade, Zoetis has discontinued several of its product lines, which could ultimately affect manufacturing sites that were solely in charge of producing them.

“In order to sell our products, we must be able to produce and ship our products in sufficient quantities. Many of our products involve complex manufacturing processes and are sole-sourced from certain manufacturing sites”

Going back to Librela and Solensia, management mentioned something that really called my attention with regards to the industry’s fundamentals. For context, both products were released in Europe and received approval in the US, with Solensia having already launched there as well. The whole market showed extreme excitement towards Librela and Solensia everywhere. An excessive demand could be seen as something very positive, but it can be deadly for a company if managed incorrectly.

“you also want to make sure that you have all the supply to do that without having pets get on the product and not being able to sustain them on it.”

It is not enough to only provide an initial supply to the market because these products are of recurring usage in nature. Companies have to make sure they can recurrently manufacture and supply veterinarians and distributors accordingly. To this end, Zoetis has been ramping up capital expenditures to increase manufacturing capacity, mainly focused on Librela and Solensia. If Zoetis launches Librela in the US and demand exceeds supply, the brand (both of Zoetis and Librela) would be extremely hurt.

Zoetis management learned from Apoquel’s release. In 2013, when the product was released, market research showed that efficacy was not much higher than existing therapies. The company then built their manufacturing capacity and inventory based on this information. It turned out to be incorrect, efficacy was extremely high and demand highly outpaced Zoetis capacity to supply the market. Market reaction was very negative. Imagine being a vet or pet owner and not being able of providing the animal with something you know it works. It really damages the company’s image. If Zoetis wasn’t the only player with a product that worked, Apoquel could have been a dead product for consumers and, Zoetis reputation, seriously damaged.

Personal commentary

We now have Zoetis thesis, financials, their acquisition strategy and some more things to cover. I believe it will all be included in the last part of the company’s research, which will be published in two weeks probably. Make sure to subscribe below if you’d like to receive it!

Disclosure: This is not financial advice.

Need to do my research on this one. Sounds like incredibly high quality. I like niche players with a large moat.

Just got our new dog yesterday, so would be fitting ;)

Another beautiful write Giuliano.... they've just gotten better with time !!