This is going to be a very interesting, but somewhat long read. I highly encourage you to skim through the article and subscribe if you find it useful!

Mission

“At Zoetis, our purpose is to nurture our world and humankind by advancing care for animals.”

History

Zoetis story begins over 70 years ago. In 1945, Benjamin Duggar was working at Lederle Laboratories and discovered the first tetracyclines antibiotic, called chlortetracycline. Tetracyclines is a large family of medications that act upon broad spectrum of infections and diseases. I’d love to get technical here, but at the moment, my ignorance limits me.

From this family of medications, which are sold under various brand names, is where tetracycline derives. It consists in an oral antibiotic used to treat infections such as acne, cholera, mallaria and syphilis. Once tetracyclines beecome more known in the scientific world, more research was conducted on this specific front.

In 1950, a research team at Pfizer found, near one of their laboratories, in a soil sample a bacterium called Streptomyces Rimosus. After exhaustive analysis of the discovered product and some playing with it, the research team, alongside a Harvard chemist, they got to realize it was a potent producer of oxytetracycline. The latter was part of the second broad-spectrum family of tetracyclines discovered and was utilized to create the product that would let Pfizer enter the animal-health industry.

Terramycin was initially used to treat eye infections in humans and later expanded to other conditions such as pneumonia. As of today, it is not widely used in human medicine due to new medicines being more effective. However, it is still utilized to treat bacterial infections in animals, particularly in livestock such as chickens, cows, and pigs. You can buy this in all online retails stores and veterinaries.

After the succesful enterprise, the Pfizer Agriculture Division decided to open a research & devleopment facility in Indiana, called Vigo. Vigo was originally established to support the development and production of Terramycin. It later expanded its scope to include R&D of other animal health products and, over the years, got involved in the development of many important ones.

In the 60s, researchers from this facility developed a vaccine for canine distemper, a highly contagious viral desease that affects dogs. This vaccine was widely adopted by veterinarians and got Pfizer’s animal business unit into the companion-animals industry. The product was labeled Duramune and it’s still produced and commercialized by Zoetis.

Throughout the 60s, 70s and 80s, Pfizer’s animal health business unit continued developing medicine and vaccines while it also grew via acquisitions. In 1988, the division was renamed Pfizer Animal Health. The subsequent decades consisted as well on building manufacturing facilities and acquiring strategic companies and laboratories to expand offerings.

In 2013, Pfizer’s Animal Health division was spun off into a separate company called Zoetis, which became publicly traded in the New York Stock Exchange. The name Zoetis derives from the zoological term zoetic, which means “pertaining to life”.

Business Overview

Zoetis is a global leader in the animal health industry, focused in almost the complete spectrum of the value chain. Specifically, it discovers, develops, manufactures and commercializes medicines, vaccines, diagnostic products and services, biodevices and genetic tests. Zoetis counts with over 300 product lines

The company’s products are for eight different core species, which can be grouped under two major labels:

Companion Animals include dogs, cats and horses

Livestock comprises cattle (members of the Bovidae family), swine (domestic pigs), poultry (domesticated birds), fish and sheep

Products for the first group help extend and improve these animals’ life quality, increase convenience and compliance for pet owners and help veterinarians improve the quality of their care and efficiency of the business. This segment is fueled by economic development and increases in pet ownership and spending on pet care. Furthermore, companion animals’ life expectancy has been trending upwards for the past couple of decades, increasing the lifespan in which they could require medical attention.

Livestock products are primarily meant to help prevent and treat diseases in a cost effective way. This enables veterinarians and producers to provide their service and products in the most sustainable way, with the highest quality and for the lowest price possible. Growth drivers on this segment are human population growth, an increasing standard of living and a greater focus on sustainable food production.

Products are also catalogued into seven different categories. To get a better grasp of them, I’ll include one product Zoetis offers in each category:

Parasiticides are products that prevent or eliminate external and internal parasites. For example, ProHeart is a parasiticide used in dogs and cats that prevents heartworm infestation.

Vaccines are biological preparations that help prevent diseases of the respiratory, gastrointestinal and reproductive tracts or induce a specific immune response. The Vanguard line of vaccines is a portfolio of vaccines designed to help protect dogs from a range of infectious diseases such as canine distemper and leptospirosis.

Dermatology focuses on the diagnosis, treatment, and prevention of conditions related to the skin, mainly, but also to hair and nails. One of the products Zoetis offers on this category is Apoquel, utilized for the control of pruritus associated with allergic dermatitis in dogs.

Anti-infectives products prevent, kill or slow the growth of bacteria, fungi or protozoa. Clavamox is a broad-spectrum antibiotic for cats and dogs.

Other pharmaceutical products include pain and sedation, antiemetic, reproductive and oncology products. For instance, Cerenia is a medication that prevents and treats acute vomiting in dogs and cats.

Medicated feed additives provide medicine for livestock. The lincomycin line of products control necrotic enteritis and helps treat other conditions in swine and poultry.

Animal health diagnostics include testing and analysis of blood, urine and other related products.

The company also derives revenue from other non-pharmaceutical product categories, like nutritional, biodevices, genetic tests and precision animal health.

Innovation

Patents and intellectual property have always been a fundamental driver of the healthcare industry and, for this reason, Zoetis focuses heavily on R&D. With research and development, the company aims to discover and develop new chemical, bio pharmaceutical and biological entities.

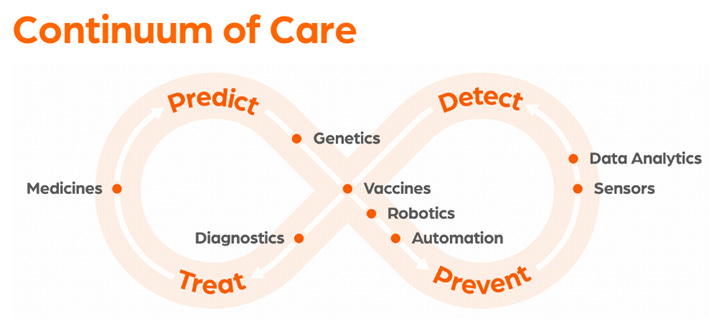

Zoetis focus' has been around the complete chain of diseases. The company’s intention is to build and integrate a portfolio that covers everything about animal care, at each stage of diseases.

Furthermore, Zoetis holds the vision that the future of animal health will depend on integrating all these solutions and technologies to better predict and prevent sicknesses/infections more effectively:

Through genetic testing, Zoetis helps livestock producers determine which animals are less prone to certain diseases so they can select the healthiest animals for their herds

For prevention, Zoetis has been longly committed to developing and producing vaccines, both for companion and livestock animals

Through a combination of diagnostics, digital tools and data analytics, Zoetis provides insights into an animal’s health band behavior to detect potential diseases as soon as possible. To this regard, the company acquired Abaxis, which possessed products like VetScans:

- VetScan HM5 is a hematology analyzer that’s fully automated and easy to use (apparently). Its 5 part differential is available for 6 species while the 3 part for nine

-VetScan VS2 is a comprehensive clinical chemistry results for point-of-care diagnosis

Finally, even if Zoetis is completely in charge of taking down diseases before they even appear, the company is also in charge of providing the necessary treatment to animals

Capital allocation within R&D

Zoetis management team has their objectives very clear:

“we allocate capital based on return on investment criteria, taking into account customer needs, revenues and profitability potential, the probability of technical and regulatory success, and timing of launch” 2012

“We make our strategic investments in R&D based on four criteria: strategic fit and importance to our current portfolio; technical feasibility of development and manufacture; return on investment; and the needs of customers and the market.” 2022

Although the framing has somewhat changed from a singular focus on ROI to a broader one, management’s narrative for their decision-making stands trough time. Additionally, they have structured investments in R&D projects in a very organized way. This allows management and the different teams to have a ‘comprehensive view of the status of projects progression and spend’. Moreover, it facilitates their ability to set targets for timing and goals for investment efficiency and makes the process cost-effective and relatively predictable.

As mentioned, R&D is focused on the creation and development of new products and product lifecycle innovation. The latter involves leveraging existing animal health products by adding new species or claims, achieving approvals in new markets, or creating new combinations and reformulations. Regarding both, there was an interesting change in management’s narrative:

“The majority of R&D investment is focused on brand lifecycle development” 2012

“A significant share of R&D is focused on product lifecycle innovation” 2022

In their 2023 Investor Day, management said they utilize 60-70% of their R&D investment budget for new products. The remaining 30-40% is destined to lifecycle innovation. With new products, Zoetis creates and expands markets. With lifecycle innovation, Zoetis protects the extremely valuable franchises they build, not letting them succumb to competition’s innovation. Out of the latter investments, Zoetis provides further breakdown:

New claims are new indications for existing products such as building new flea and tick claims for the parasitology portfolio.

New formulations imply old recipes/medicines, but with a new application method. An example of this is Apoquel Chewable.

Geo expansion is taking new products to new markets, new countries.

New species would mean leveraging an old discovery/invention/medicine and try to adapt it to a new species.

Moving on, out of the total R&D budget, a third is invested in bio pharmaceuticals, around 25% in the bio space (vaccines mainly), meaning over 50% of R&D investments are destined towards biologicals in one form or another. Management continues to see great potential in pharmaceutics focused on parasitology, which already represents a fourth of Zoetis’ portfolio. The last 10% is invested on new diagnostic offerings.

Finally, Zoetis investment thesis for their R&D’s animal group target has been shifting over time, with growing investments in companion animals. As of 2023, 60% of their budget was allocated to this group while the remaining 40% is destined towards R&D in livestock. Management expects this gap to widen to about 65/35 in 2024 after which the mix will be based on the value each proposition each group supposes moving forward.

A unique R&D model

Here’s one of Zoetis key distinctions with competition. Its R&D model very much resembles that of Tesla’s manufacturing model. Zoetis has built all relevant and necessary components of the R&D ‘value chain’. They have full capabilities across the continuum of care, having capabilities of genetics, genomics, robotics, automation, biosensors, bio devices and diagnostics. Furthermore, the company has manufacturing, supply and commercial capabilities. This allows Zoetis to approach diseases from all perspectives.

For instance, if Zoetis is working with a pet, the R&D team can leverage their genetics, genomics and strong analytics platform to probe not only the species’ biology, but also complex diseases areas. They can ask the following questions:

"Is there a genetic basis or predisposition to disease in these animals? We have the capability to understand how are these disease initiated? How do they progress? And does our therapeutic intervention either slow or arrest progression of the disease?”

Since they have this unique R&D model, Zoetis can go and explore all these new biomarkers that can be used for further research on different verticals. Once they identify what’s the basis of the disease and how it’s progressing, they know how to intervene. And given their vast portfolio of offerings, they will most likely have a solution or have the full capabilities to build one.

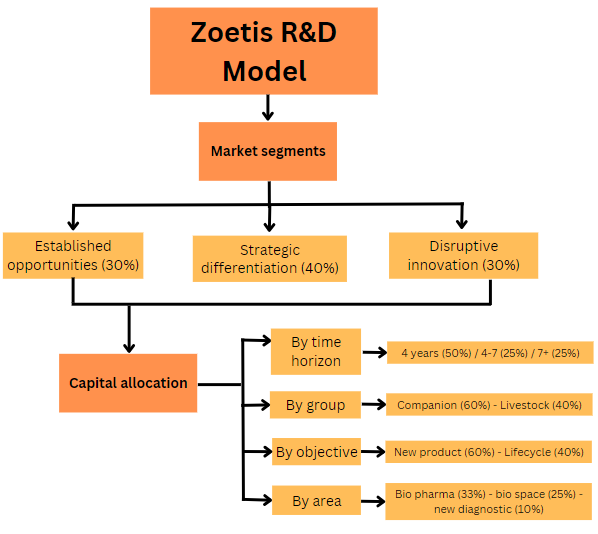

Moving forward, within their R&D space, Zoetis focuses on three specific market segments:

Established opportunities. These are markets Zoetis really understands the value of bringing a new product to and have high confidence on delivering. An example is the parasitology market, where they recognized the value Simparica would create.

Strategic differentiation. These are the same markets than above, but here Zoetis looks for target differentiation for incremental value. An example of this is Simparica Trio, a triple combination therapy.

Disruptive innovation. This implies an opportunity Zoetis sees to go out and create the market. It’s pure invention, doing 0 to 1 moves. An example of this is the dermatology and allergy market, where Zoetis practically invented the market. At the same time, it includes heavy market expansion with the introduction of new products. An example of this is Solensia and Librela, where the pain inflammation market was very well known, but these new introductions expanded its reach drastically.

Finally, Zoetis recognizes their R&D projects differ in time horizon. As with segments, the timeframe at which they aim these projects to deliver a product is divided into three categories:

Zoetis invests 50% of their R&D budget in near-term projects, which are destined to deliver a product to the market over the next four years.

25% is destined towards mid-term projects, aiming to bring a product to the market within four to seven years.

25% goes to their long-term portfolio, which is composed of projects that are planned to bring products to the market in seven or more years.

“[investing this way] seems to be a winning strategy for us with respect to being able to ensure that consistent delivery year-on-year from our portfolio.”

To wrap it all up (in parenthesis goes the percentage of allocation):

Ultimately, to ensure their long-term objectives are accomplished, Zoetis created a new research arm in 2019, their incubator. The company reached an agreement with Colorado State University and built an incubator research lab that operates in their campus. The objective of it is to explore and exhaust verticals of research, with an initial focus on biotherapeutics for cattle. Its creation allows Zoetis to run more R&D projects in parallel, increasing the odds of success. Additionally, it provides the company with an early research approach, needed to feed the longer-term deliverable part of the portfolio.

How Zoetis funds innovation

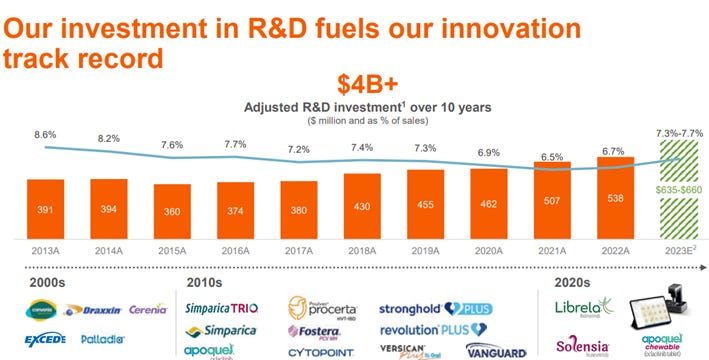

Funding research and development is not only risky, but costly as well. With no guaranteed results, investing in R&D can completely backfire. However, Zoetis is one of the most cautious companies when allocating capital. The company is very efficient at an operating level. As of 2010, Zoetis had around one thousand employees dedicated to research and development and, in 2022, employees were 1,430. In the meantime, revenue grew more than 2x and margins heavily expanded, 9/15 blockbusters were delivered, etc.

As observed, Zoetis spent approximately 400M dollars in R&D in 2014 and, in 2023, expenses rounded 530M. Output is increasingly outpacing input.

The second way in which Zoetis innovation is funded is through partnerships, which allows it to share the high risk of R&D initiatives. The company joins forces with partners at all stages of the process, from early R&D to commercial products. It looks for partners throughout the animal health, pharmaceutical, biotechnology, and agribusiness industries. Additionally, it collaborates with leaders in academia and at public and private institutions. General areas of partnerships are therapeutics, preventatives, diagnostics and genetics, technologies and digital.

“Zoetis also affirmed its position as the animal health partner of choice, engaging in more than 100 research collaborations with companies and institutions across pharmaceuticals, biotechnology, agribusiness and animal health.” 2016

This powerful network of R&D Zoetis has built allows it to be on top of everything, given how relatively small the industry is, making all potential new products and improvements fall rapidly into their scope. Furthermore, the risk mitigation this generates is massive.

Lastly, Zoetis is granted funds from different foundations, like Bill & Melinda Gates Foundation, due to their mission of improving animal’s lives. This attracts altruistic and philanthropic capital.

“Zoetis is pleased to receive a $15.3 million grant from the Bill & Melinda Gates Foundation” March 2023

“* (Zoetis) Will receive $14.4 million grant from Bill & Melinda Gates foundation over next 3 years” May 2017

At the same time, being the leader in the animal health industry makes Zoetis a phenomenal candidate to receive grants from the US government. According to US the department of agriculture department database, Zoetis was granted over 3M dollars for R&D in 2022.

Results of R&D

It is futile to invest money in R&D if it leads nowhere. That’s the reason why evaluating R&D results is crucial and even more so in a company within the healthcare industry. Patents are a somewhat tangible proxy that can help measure how effective Zoetis’ model is. Obtained and pending patents illustrate whether the company is successfully inventing new medicines and what the ‘backlog’ of potentially future medicines/solutions looks like.

In their first annual report after going public in 2013, Zoetis disclosed having a portfolio of 4,800 patents. In their last (2022) one, they disclosed a total of 6,320 patents. Moreover, Zoetis disclosed having 2,000 more patents that were pending in 2014, number that dropped to 1430 in 2022. That means that, assuming no patent has expired (unlikely, but still), Zoetis R&D team has been able to come up with 850 regulated inventions. Lastly, the company still has a quite large backlog of potential solutions coming in the future.

Seeing products hit the market is another method to evaluate R&D’s effectiveness.

Zoetis spent around 4bn dollars during the past decade in research and development, but mainly focused on quality, and expansion. This can be seen in the product lines they have. They were at ‘over 300’ in 2015 (oldest record) and, in 2022, they reported having ‘approximately 300’, meaning product lines technically declined. However, out of the 15 100M+ run-rate products Zoetis has, 9 of them were delivered in the last 10 years. Finally, over the past decade, Zoetis received over 2,000 regulatory approvals and dramatically expanded many of its products’ reach.

Blockbusters

Blockbusters are the products that generate 100M or more in annual revenue. These are market dominants, which in many cases build vertically small monopolies. At the moment, Zoetis holds more than a third of the blockbusters in the animal health industry.

Perhaps a deep dive into each of them can be a topic of a future article, but going over some of them is vital to understanding the industry and sub-segments peculiarities.

Librela and Solensia

A cartilage is a strong, flexible connective tissue that protects joints and bones. It allows bones to move over or around each other without pain. Arthritis is a common disease that affects these joints, causing pain and inflammation and bones in affected joints become weaker.

The most common type of arthritis, and the one Librela and Solensia are used for, is osteoarthritis (OA). OA begins as a disruption of the cartilage, which ultimately causes the bones in the joint to erode into each other. Curiously, the first registered case of OA is of a dino-bird that lived 130 million years ago. As for dogs, the oldest case traces back to 14 thousand years ago.

Librela is the first injectable monoclonal antibody (mAB) therapy for monthly alleviation of osteoarthritis pain in dogs. It was first approved in the EU and Switzerland in 2020. The mAB, called bedinvetmab neutralizes the Nerve growth Factor, a key player involved in OA in dogs, and in doing so, reduces pain. Since bedinvetmab is an antibody, it is eliminated by the body with minimal involvement of the liver or kidneys. Solensia is the same but for cats, as far as I can tell. Since commercialization and added together, over 6.1 million doses have been delivered as of March 2023 in EU.

At the end of 2020, prior to Solensia and Librela’s launch, the global OA pain market was estimated to be a 500M dollar market, out of which Zoetis held 28%, implying revenues of around 140M. Two years after both releases in Europa and Canada, the market was valued at 700M and Zoetis had 39% market share, implying revenues of 273M.

In Q1 of 2023, management said Librela and Solensia did 51M in revenue for the quarter, meaning Zoetis market share continued to increase. Moving forward, a key element the company will focus on is the education of pet owners and vets. People are generally not aware of the negative impacts OA has and confuse it with ‘normal signs of aging’. Once awareness increases, so should demand.

Management’s ability of correctly assessing market and industry conditions really called my attention:

“If you look at it today, there's about 165 million dogs across the EU and the US, and about 40% of them will get OA. And right now, depending on whether in the US or Europe, really diagnosis is somewhere between 25% and 40%” Q3 2020

“We're extremely excited about our monoclonal antibodies for pain with both Librela and Solensia having long-term blockbuster potential.” Q4 2020

With the first quote, we can more or less have a vague sense of the information management had available prior to the launch of the products in early 2021. In the second one, the team confidently gave their view about Librela and Solensia’s future and it rapidly came true once they launched. This is an interesting indication of how “transparent” can the animal health industry be in this regard, truly allowing for ROIC maximization when thinking about markets to tackle. Management also seems to have margin estimate that help further maximize ROIC.

The last thing to highlight is the high risk/reward ratio of their disruptive innovation R&D segment. The change in the company’s revenue and its immediate translation into market share suggests the OA pain market was very mature. Given how old the problem was and no solutions had emerged, it is expected that they don’t appear in the near term either, making Zoetis the favorite candidate to capture future growth. However, in their Investor Day, management did say they expect competition to come in, though they recognize they have a huge head start and will take advantage of it.

“It is the first time doing this with the FDA. So, it's just honestly a new process for both, and understandably, it's the first time they're looking at some of these types of products.” Q4 2020

By Zoetis being capable of identifying these key unattended markets in which a new product could emerge or an old market with expansion probabilities, the company can create monopolies, or close to. The addressable market they projected for 2032 is of 2-3bn. However, the current market is at 0.7bn, with Librela and Solensia being at a 200M annual run rate. Management also thinks both products could potentially peak sales at 1bn, in a 2-3bn dollar market. That supposes a 50%-33% market share, achievable thanks to disruptive innovation and with little to no possibilities of displacement.

Simparica

Ticks and fleas are two different types of parasites that commonly infect both cats and dogs. They bite and suck blood from their hosts and transmit diseases.

Simparica was released to the market in 2016. Solarica (sarolaner) is a chewable cure for fast and effective treatment against fleas and ticks. The active substance, sarolaner, acts as an ‘ectoparasiticide’. It kills parasites that live on the skin or in the fur of animals. In order to be exposed to the active substance, these must attach to the dog’s skin and start feeding on their blood. Sarolaner kills these parasites that have ingested the dog’s blood by acting on their nervous system. Simparica’s solution lasts for one month and it has no known side-effect.

In 2020, Zoetis introduced an ‘improved’ version of Simparica, called Simparica Trio. This new chewable tablet contains three substances: sarolaner, moxidectin and pyrantel. Moxidectin kills parasites present in the body of animals, such as roundworms, hookworms. Pyrantel also kills roudnworms and hookworms present in the gut, but it acts differently. Simparica Trio received approval from the FDA on February 2020 and became the first all-in-one protection in the US against the mentioned parasites.

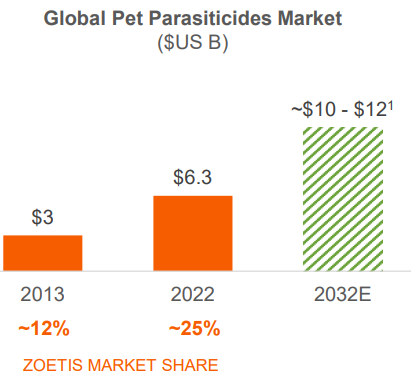

Simparica has had competition since inception, but Trio apparently does not, at least in the US. In Q1 2023, Simparica Trio generated 175M in revenue globally, implying it is at a run rate of over 600M. The product allowed Zoetis to drastically increase its share of the global pet parasiticides market, going from 12% in 2013 to 25% in 2022.

Simparica Trio’s competitors are Trifexis, produced by Elanco, and Frontline Plus, produced by Boehringer. I’ll be diving further into Zoetis’ competitors in the next research article.

Apoquel and Cytopoint

Atopic dermatitis is the second most common allergic skin disease in dogs. It is an inflammatory, chronic skin disease associated with allergies, generally caused by an allergic reaction to normal things like grass and dust. Atopic dermatitis causes itching, scratching, rubbing, redness and tough skin. This disease cannot be cured as far as science has gone.

Apoquel was approved in 2013 and released in 2014, and works by preventing the production of cytokines. It suppresses the enzymes that cause this itching and inflammation. This helps break the cycle of itching and scratching and allows dogs’ skin to heal. Apoquel is currently the only drug available for dogs that works this way, stopping allergic itching at its source.

Apoquel was the first solid product that supplied this unmet need in the pet dermatology market. The medicine started being distributed and given to pets in the form of a pill. However, Zoetis kept in mind the difficulty that making a dog swallow a pill supposes, and worked on developing an easier method. To this end, it developed Apoquel Chewable, which is unclear when it was exactly released, but in Q4 of 2021, Kristin (CEO) said “you saw us add Apoquel Chewable in Europe”. Apoquel Chewable has the same ingredients as Apoquel, but it comes in the form of a chewable tablet. This product is a great example of lifecycle innovation. Management’s commentary on its adoption:

“The movement to Apoquel chewable has been a real – it's been growing much faster than we expected, and the conversion there remains very, very strong.” Q4 2022

The second product the company developed was launched in 2016 and it’s called Cytopoint, which is a solution that is injected under the skin once a month. The active substance in Cytopoint, lokivetmab, is a monoclonal antibody that recognizes and attaches to a protein that plays an important role in triggering dermatitis in dogs. By attaching to and blocking the action of this protein, lokivetmab reduces itchy skin and inflammation.

The main difference with Apoquel is that the latter requires daily oral dosing. With both products, Zoetis practically created the market, which had a huge unattended demand. Starting as a 100M dollar market in 2013, it grew its size to 1.4bn in 2022. Apoquel and Cytopoint helped Zoetis position itself as a true leader, now possessing a 95% market share.

Something I found very interesting is that in 2016’s annual report, management said they expected Apoquel to be a 300M revenue product at peak sales. This last quarter, revenue of key dermatology products (that’s Apoquel and Cytopoint) was 290M, down from 307M last year. Under the assumption that each product does half of the revenue, Apoquel is at a 600M annual run rate. Going back to this ‘market transparency’ I mentioned with the other products, it seems as if management is really capable of inferring true addressable market and, moreover, rapidly achieve it. This variable plays a key role when deciding what to invest in to maximize ROIC.

Already by Q1 of 2018, Apoquel and Cytopoint were seeing massive adoption, having surpassed the 100M in quarterly revenue. This made management raise their prior ‘dermatology guidance’ to call for 500M in dermatology revenue for that year. What we are seeing is not only that management recognizes market opportunities, but also that how fast adoption could be. This is also something spotted on Librela, Solensia and Simparica Trio. They were massively and rapidly adopted. Too many coincidences for them to be called that way.

Personal commentary

This is the first part of Zoetis research. On the next one, I’ll focus on their manufacturing and supply capabilities, the industry fundamentals and as much as length allows me to. I’ll try to provide you with all relevant information about the company.

Great job Giuliano! Looking forward to the industry fundamentals section.

Great deep dive on the R&D and product line of this amazing company. Looking forward for the second part!