Zoetis Q2 Earnings Review

Zoetis reported results last Tuesday before the market opened. This is the last company I’ll be covering for the quarter. We’ll initially go over its general performance from a financial standpoint and then dive into some details. Reading the research is always recommended to fully understand reviews.

The company generated a record 2.2bn in revenue during the second quarter of 2023. Yearly growth was 6% and 9% operationally (excluding FX impacts), while sequential growth was 9%. Zoetis experienced an excessive demand during the pandemic, for which growth digestion is, or was, needed. It got to grow at 20%+ rates in an industry that has a 15yr CAGR of around 5%. Management had called for a weaker first half of the year and an acceleration during the second.

Zoetis reported doing 1.57bn in gross profit, implying a record margin of 72.2%, up 260bps YoY and 160bps sequentially. Operating income was 826M during the quarter, with its margin being up 250bps on a yearly basis to 37.9%. Finally, net income was 671M. The respective margin was 30.8%, which increased 500bps YoY and 320bps QoQ. Nevertheless, it’s worth noticing that there was a 106M swing in other income and 61M extra destined to provision for taxes on income, which ultimately benefited earings by 45M.

Turning into the cash flow statement, Zoetis generated 183M in cash from operations. Because there is some seasonality in the business and strange patterns during this year (not sure what happened), YTD cash from operations were 732M, up 13% on a yearly basis. Capital expenditure was 166M for the quarter and 389M for the first six months, compared to 261M in last year’s first half. This puts YTD free cash flow at 343M.

Moving forward, we’ll break down Zoetis revenue as I see would add the most value. Firstly, I must highlight that the trend in revenue by geography is one to keep a close eye on. Geographical diversification can prove very advantageous in moments of economic weaknesses. This Q, Zoetis derived around half of its revenue from the US and the other half internationally, which has been the case for at least the past 4 years.

Keeping a general overview, Zoetis differentiates among two major groups of animals. During the quarter, revenue generated selling products meant for companion animals was 1.48bn dollars, up 9% on a yearly basis. On the other hand, livestock revenue was flat year over year, being 671M. Companion animal products now generate 68% of Zoetis’ total revenue, increasing from a 50% share 4 years ago.

Zoetis then distills revenue by major product categories. Slight overview of all of them to then dive into the most insightful ones.

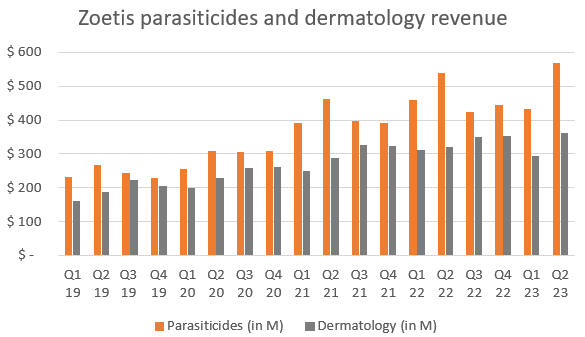

Parasiticides did 568M in revenue, up 6% YoY

Dermatology revenue was 359M, up 13%

Vaccines revenue decreased 4% YoY to 430M

Other pharmaceuticals revenue grew 19% to 315M

Anti-infectives was up 5% YoY to 244M

Diagnostics generated 96M and was up 10% YoY

The two categories that have been with a lot of momentum are parasiticides and dermatology. The first of them due largely to Simparica Trio, which generated 248M in revenue and was up 5% YoY. Nonetheless, Revolution also caught traction, growing at 18% yearly to 103M. On the other hand, what’s curious about the dermatology market is that Zoetis has held a monopoly since 2013 and there hasn’t appeared any competition since, which continued being the case this quarter. Revenue grew 13% to 359M, with management still foreseeing opportunity moving forward.

The last category I’d like to put the spotlight on is in Zoetis other pharmaceuticals. In here, we have pain and sedation, which means Librela and Solensia are included. Since the launch in EU, both have been gaining a lot of traction, with Librela having generated 48M in revenue during the quarter, an increase of 85% YoY. Zoetis mABs for OA pain products generated a total of 69M.

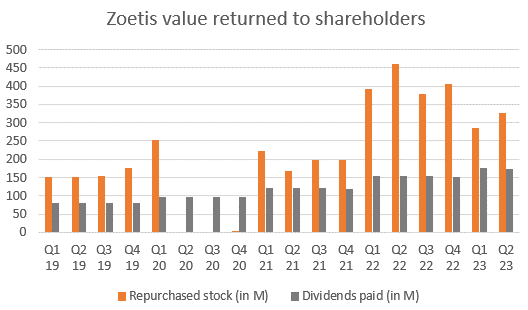

Capital returned to shareholders

During the quarter, Zoetis repurchased 324M worth of shares, at an average price of $171 per share. There are now almost 2bn left for the stock buyback program. At the same time, the company paid dividends for a total of 173M, making the total value returned to shareholders of almost 500M for the quarter.

Management commentary and outlook

Zoetis management began by addressing what they believe makes the company be in a strong position. The diversified portfolio of products Zoetis has helps it better endure tough times like the ones management mentions we are currently going through. Even though the team is taking into consideration global inflation, “the underlying demand has remained steady and resilient to date, and this is what we have seen historically”. Moreover, because of their extensive reach in terms of fields, areas and species, and the continuous innovation, Zoetis seems to always have an actual growth driver going into each fiscal year.

On this last point, the dermatology, OA pain and pet parasiticides market have been strongly enhancing Zoetis’ topline. In the dermatology market, management mentioned the continued momentum, expecting a double-digit growth this year, with still a large opportunity moving forward. To try reach the untapped demand, the company is promoting direct-to-consumer campaigns to drive awareness on Cytopoint and Apoquel. On the latter, its chewable version has seen great receipt by the public. During the quarter, it generated 213M in revenue, growing 2% YoY. Apoquel Chewable received FDA approval during the quarter.

With regards to Zoetis parasiticides portfolio, they particularly mentioned its growth was driven by the revolution franchise, which grew at 52% YoY, but mainly due to the lack of supply there was last year. More importantly, competition finally arrived for Simparica Trio and analysts asked management what were they expecting for Zoetis pet parasiticides portfolio. Kristin and Wetteny said they are confident on Trio’s label strength. It is now the No. 1 in companion animal pairs in the US and, fueled by their three years of demonstrated efficacy, they still expect growth moving forward.

“We think we can be very competitive with our product based on the strength of our label, the strength of the experience with the product. Our relationships clearly with the corporates and really with a very pleased pet owner who's on this product. We are expecting very strong quarter in third quarter despite the competitive launch,”

Finally, Librela and Solensia have had a lot of momentum in all markets in which they were launched. In May, Zoetis received FDA approval for Librela (something management called for in the past quarters) and expect the launch to be in November. Librela, for the second consecutive year, is the number 1 osteoarthritis pain product in the EU.

In the next quarter, management expects “revenue between $8.50 billion and $8.65 billion, representing a range of 6% to 8% operational growth”. Keep in mind operational growth excludes FX impact.

My take

Zoetis performed. Quarters like the one the company just had are what I believe will be the norm. This is not an industry that grows at double digits, which makes it quite difficult for Zoetis to reach such levels. Nonetheless, it is an industry with spectacular fundamentals, practically designed for an oligopoly to dominate. Moreover, it is one with inherently high returns on capital if capital is managed correctly, and one in which companies benefit from high margins. That’s what, in my opinion, should make a Zoetis quarter good, stable yet high quality performance.

At the same time, I’d catalog the animal health industry as temporarily capital intensive. Zoetis needs to build manufacturing capacity to supply its distributors and veterinarians, which requires large upfront investments. For this reason, the company has been incurring in increased capital expenditures, when compared with the last decade’s average. What’s important about such periods is that management guides for them beforehand, like Texas Instruments. On this occasion, so did Kristin and Zoetis team. CapEx are mainly destined to scaling their mAB platform for Librela and Solensia.

It appears as if the most worrisome issue was free cash flow, something affected by not only CapEx, but inventories as well. Inventories increased from 2.2bn as of June of last year to 2.7bn now, with 424M spent this quarter versus 312M on the comparable. This item implies an outflow of capital, as Zoetis builds up inventory. Cannot help but notice multiple resemblances between Zoetis and Texas Instruments.

“we have significant launches, including Librela, for the US and across other markets that's going to keep our inventory levels somewhat elevated through 2024” Investor Day 2023

At the same time, Librela and Solensia are expected to help Zoetis expand margins. Both the expected addressable market and their contribution to the bottom line put into perspective the required upfront investments. What’s also curious is that Zoetis average product life is around 30 years, which means it could benefit from their OA pain solutions for a long time.

The other thing I’d like to point out is the continued emphasis on companion animals. Management believes it will be a larger growth driver than livestock for the next decade and beyond, for which focus has been placed on growing their portfolio. At the same time, products meant for companion animals are generally sold for higher margins, helping the company achieve their guided expansion. This is yielding good results already, as companion revenue is still growing at double digits and now represent 68% of the company’s sales, up from 50% 4 years ago.

Finally, the company’s key areas in my opinion, which are dermatology, pet parasiticides and their OA pain portfolio are very rapidly growing and still have a long runway.

Personal commentary

I’ve been researching Zoetis for some months now. It appears to be the company that I know the most about at the moment. The second part of the research will be published next week and the third part by the end of August probably. Hope you enjoyed the article!

Disclosure: This is not financial advice

Great summary! I've added shares and ZTS is now my second largest holding. Great company, great moat and great execution.