The Operator Premium

Why Brad Jacobs raised $5bn on a plan and Elon got a $1tn comp package approved

After 2.5 years, I returned to reading Buffett’s letters. And I ran into a quote that immediately got to me:

“If [Tom] Murph[y] should elect to run another business, don’t even bother to study its value - just buy its stock”

I’m coming to a very firm impression that all great investors say one thing and dismiss another that’s equally true or even truer. Warren articulated this idea of ‘you want a great business because, one day, a fool will run it. But if it’s a really good business, the fool won’t destroy it.’

To a large extent, the premise is sound. Now add to it his other idea, namely that ‘when a manager known for his reputation of brilliance tackles a company known for terrible economics, the latter prevails.’

The investment community had no option but to conclude that business > manager. This seems to me as an increasingly fragile thesis. Anecdotally, in Warren’s biography, Alice writes about how Coke’s moat almost vanished over a 5-year period. The exceptional, indestructible business was brought to its knees after a CEO change.

John Morgan and the Transferability of Skills

In the 90s, Winmark (resale stores franchise) was almost bankrupt. Morgan came in and changed the business model. The company used to focus on selling merchandise to franchisees and John turned it into a royalty business.

What remains on my mind, however, is not Morgan’s genius decisions. John had previously successfully founded and exited an equipment leasing operation. And when Winmark stabilized, he brought that capability to his new business. Morgan single-handedly built a leasing business unit within Winmark and quickly scaled it to $40-$50M in assets, and $10-$20M in sales.

Just because John Morgan was there, Winmark’s shareholders benefited in a two-fold manner: (i) they earned extra profit (otherwise nonexistent); (ii) they had a profitable, high-ROIC avenue for capital deployment. After his retirement, new management discontinued the leasing business, fully acknowledging it was John. Winmark now returns most cash flow.

The market tries to consider everything when pricing an asset, which includes people. Fundamental business skills are transferable. When a John Morgan takes over a company, you know he can add tens of millions in profit because of his toolkit, irrespective of the company’s industry. There’s a dumb-sounding but true term that captures this idea: Intellectual book value.

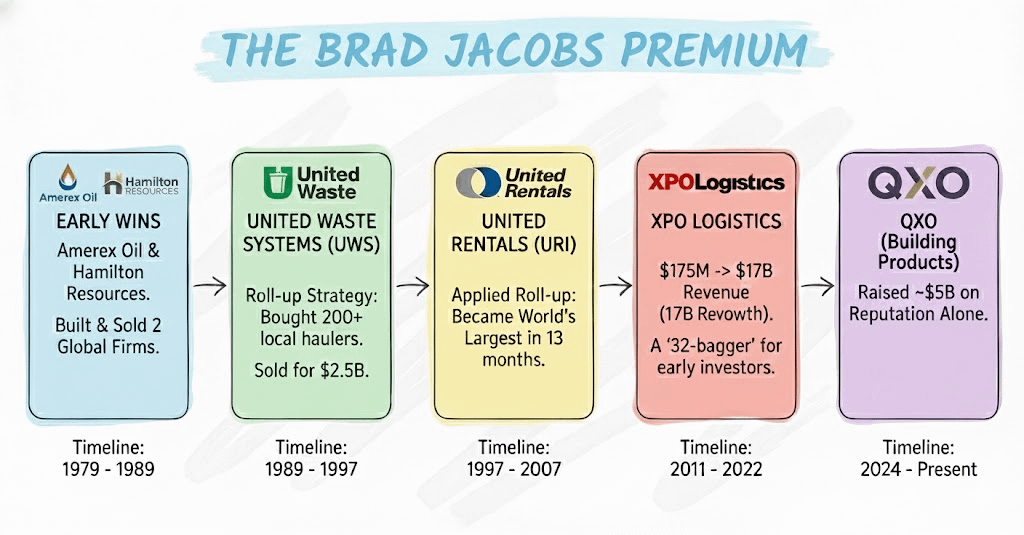

Brad Jacobs is an extreme version of this idea. He has consistently shown his ability as an operator and the market is thus able to sit back and trust. In 2024, Jacobs was able to raise $5bn on just a plan. Even though he had identified the target sector, he had no experience or operation in that industry. But the market knew that, no matter what, Brad was able to spot fragmented industries where his skills were applicable.

A dollar is not worth a dollar. Depending on who holds it, its intrinsic value can greatly exceed $1 or be close to zero. If a 40-year old Buffett owned a public company with only $100M in cash, funded with equity, the company’s value would certainly be well in excess of $100M. Capital allocation is a transferable skill, just like operating capabilities.

Trying to Understand Crazy

This is the very reason why Tesla shareholders approved a $1 trillion (!!!) compensation package for Elon, why Bezos was able to raise $6bn on an idea alone, why Larry Ellison committed $1bn to the Twitter acquisition out of just a text message from Elon, and why Apple paid $430M for NeXT (company with no viable product but with Steve Jobs).

If Sam Walton had resigned from Wal-Mart and set to start a new retailer, I’d bet on that going well. If a Lee Kuan Yew were to start a new nation from scratch, I’d bet on that. Top people’s capacity needs to be assessed and premiums should be considered accordingly. Almost always, these guys surprise you. What you think is possible falls way short of what’s possible.

Who expected Murphy’s run to end in the (by-then) 2nd largest deal in history, selling Cap Cities to Disney for $19bn?

Personal Commentary

I’ve been playing around this idea for almost a year now. Even though I feel that my grasp thereof has improved, there’s much that’s uncovered.

Been reading many books about business and investing but, for whatever reason, I can’t seem to find many valuable things to bring. It’s on my mind to record a podcast episode going through my notes on this last dozen or so books.

Always feel free to reach out at giulianomana@0to1stockmarket.com

Best, Giuliano

When Ron Baron recapped his history of investing, he said it was about investing in people which primarily led to his success.