Microsoft reported results for the first quarter of 2023, the third quarter of their fiscal year. There is always a lot to cover with this company. I will be splitting the article into an overall financial analysis and a more particular breakdown of each segment. Keep in mind I’ll plot charts as if Microsoft had a fiscal year in line with the calendar year.

Overall financial analysis

Revenue for the quarter was 52.8bn dollars, increasing 7% on a yearly basis and declining slightly QoQ. Microsoft reports revenue in two broad categories, products and services & other. The company continues having a revenue headwind occasioned by their products category, which has been falling for the past few quarters. Even though service and other revenue grew 16%, product revenue decreased 11%, partially offsetting the gains.

Nevertheless, Microsoft thesis goes around its cloud-based offerings and the fact of them being sold under a subscription or consumption-based model. The first of them represents the amount of revenue the company produces on a recurring basis and this is of extreme importance. Recurring revenue offers ‘predictable cash flows’ and tends to be far more resilient than one-time tickets. Furthermore, these types of services can be generally sold at higher margins.

Recurring revenue as a % of total has been continuously and rapidly increasing over the past 7 years, starting at a low 30-40% and now finalizing their last quarter at a new high, 70%.

Moving down the income statement, Microsoft reported a gross profit of 36.7bn, an increase of 9% over the comparable quarter. In the same line, the company had 22.3bn in operating income, growing 9.5% YoY. Lastly, it generated 18.3bn in net income, up from 16.7bn last year.

The mentioned higher increases at bottomer lines translated into expanding margins across the board. Gross profit margin stood at 69.4% for the quarter, up 100bps YoY. The operating margin was at 42.2%, also increasing 100bps. Finally, net profit margin was 34.6%, up 70bps.

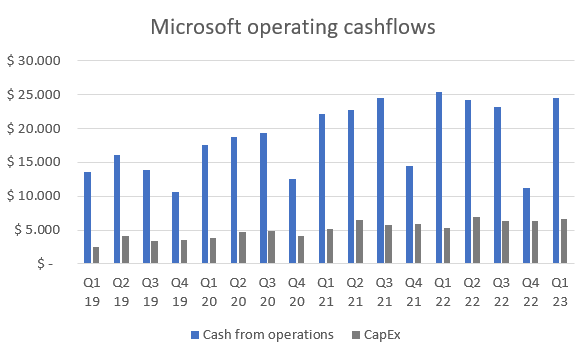

In the first quarter of 2023 (again, calendar), Microsoft generated 24.4bn dollars in cash from operations. This number was 3% below the record established on the comparable quarter. Moreover, out of the cash produced, the company spent 6.6bn dollars in property and equipment. Both variables leave Microsoft’s free cash flow at 17.8bn for the quarter.

Although there’s a remarkable bounce off the fourth quarter of last year, it is visualized in the chart the seasonality of cash flows, coming in lower in all fourth quarters.

Before going into a detailed analysis on each segment’s performance, a brief overview. In the quarter, the Productivity & Business Processes business unit generated 17.5bn in revenue, up 11% YoY and representing a 33% of total Microsoft’s revenue. The Intelligent Cloud segment produced over 22bn in revenue, growing 16% yearly and equating 42% of total revenue. Finally, More Personal Computing brought in 13.3bn, down 9% YoY and representing the remaining 25% of revenue.

From an operating standpoint, P&BP generated 8.6bn dollars, IC 9.4bn and MPC 4.2bn. The operating income each of them produced represented 39%, 42% and 19%, respectively, of the total.

Breakdown by segment

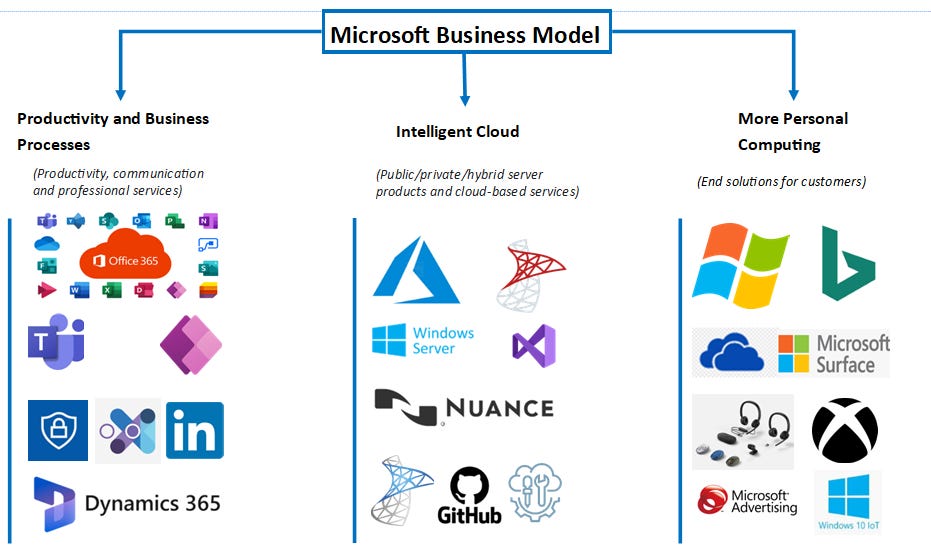

If you are not sure what products compose each business unit, this image (self-made) might be useful.

Productivity and Business Processes

Along with Intelligent Cloud, this is one of the two business units I believe matter the most for the company. In here we have products that still have a long runways, can be sold at high margins, have a thesis on their own and are immersed in this hybrid industry of professionals and productivity with a leading position.

Productivity and Business Processes brought in 17.5bn in revenue, up almost 11% on a yearly basis and 3% sequentially. Impressive to see quarterly growth given the current environment. As mentioned, margins are a huge reason for the relevance of this segment. Operating margin was 49.3% for the quarter, up 100bps YoY and 130bps QoQ.

The main offerings I pay attention to are Dynamics 365, Microsoft Office (Teams is key) and LinkedIn. All products have been growing double digits for a long time and growth accelerated during 2020/21. LinkedIn even got to 40%+ growth rates.

This past quarter, Office 365 commercial seats grew 11% YoY while Microsoft 365 consumer subscribers grew 12% to 65.4M. Remember commercial seats are enterprises and consumer subscribers are professional individuals, mostly. Dynamics 365 grew 17% on a yearly basis and it accelerated QoQ, having posted a 13% growth on the previous one. Lastly, LinkedIn grew at an 8% rate, generating 3.69bn in revenue. Deceleration on LinkedIn has been notorious, but it seems to be more growth digestion than other thing. It grew at unusually high rates for over two years, deceleration is more than normal until this extra growth gets digested.

Management quotes:

“All-up, we now have nearly 33 million monthly active users of Power Platform, up nearly 50% year-over-year.”

“Teams usage is at an all-time high and surpassed 300 million monthly active users this quarter.”

“We once again saw record engagement, as more than 930 million members turn to the professional social network to connect, learn, sell, and get hire”

Intelligent Cloud

The IC segment generated 22.1bn dollars in revenue, growing 16% year over year and 2.6% sequentially. This business unit has grown at an accelerated pace for the past years and is still closer to the high end of the double-digit growth rate. Since the last quarter of 2019, IC’s revenue almost doubled. Furthermore, this quarter produced 9.47bn in operating income, growing at 12.8% yearly. The operating margin at which the segment operated was 42.9%, down 120bps YoY and up 150bps QoQ.

Intelligent Cloud also constitutes a very large part of Microsoft’s thesis, for the nature of the revenue it generates as well as its profitability. But, more importantly, there are many businesses embedded here that have shown very high growth, profitability at scale and are still expected to grow at double digit rates for the next decade. Among some of the secular trends Microsoft has candidate leaders are cloud computing, cloud security and open-source development.

Azure, probably the most important component of Microsoft’s ecosystem, grew by 27% YoY, still showing signs of deceleration from the 31% posted last quarter. However, the size Azure is reaching makes it very unlikely for the business to sustain such high levels of growth. A 27% growth at this scale is impressive. At the same time, cloud computing players have been showing a much steeper deceleration, making Azure’s performance look somewhat resilient. As a comparison, AWS already guided for mid-teens growth in this quarter.

Management quotes:

“Azure took share, as customers continue to choose our ubiquitous computing fabric”

“We now have more than 15,000 Azure Arc customers, up over 150% year-over-year”

Cosmos DB: “And, we are taking share with our analytics Solutions”

“Today, 76% of the Fortune 500 use GitHub to build, ship, and maintain software.”

“In three months since we made Copilot for Business broadly available, over 10,000 organizations have signed up”

“nearly 600,000 customers now have four or more security workloads, up 35% year-over-year”

“the enterprise mobility and security installed base grew 15% to nearly 250 million seats.”

More Personal Computing

This segment has been posing trouble to Microsoft since 2020/21. MPC grew at too high rates with no actual increase in a sustainable long-form demand, for which the segment’s revenue has been falling since, while it tries to digest these spikes. In this last quarter, it generated 13.32bn dollars in revenue, declining 9% YoY and 6% sequentially.

Moreover, More Personal Computing brought in 4.2bn in operating income, implying the business unit operated at a much higher margin than it did a quarter before, but still below its past years average. The operating margin was at 32%, down around 100bps on a yearly basis.

In this segment, not many singular products are of extreme appeal to keep track of, at least from a perspective of what conforms Microsoft’s main thesis. Nonetheless, it is in here where they have Bing’s revenue and their gaming segment. The first of them has suddenly materialized as a potential growth driver for the company after it announced the collaboration with Open AI and integrated their features in the search engine. Their gaming segment is a secondary element, but the approach taken of having a cloud-based gaming platform plus having to pay for it with a monthly pass, opens up avenues for future capitalization.

As a reference, search and news advertising generated 3bn in revenue, up 3% YoY. Gaming revenue was 3.6bn, down 3% YoY. Windows produced 5.3bn in topline, declining 12% year over year. Finally, devices’ revenue came down from 1.8bn last year to 1.28bn in this one, adding a further headwind.

“All-up, Bing has more than 100 million daily active users.

We are winning new customers on Windows and mobile. Daily installs of the Bing mobile app have grown 4X since launch”

“We’re making progress in share gains. Edge took share for the eighth consecutive quarter, and Bing once again grew share in the United States.”

Gaming: “Our revenue from subscriptions reached nearly $1 billion this quarter” “We have now surpassed 500 million lifetime unique users across our first party titles.”

Outlook and management commentary

Satya made sure to remind investors and analysts what Microsoft is about. He thoroughly talked about how their whole ecosystem is performing and it emphasized their leading position in a wide array of verticals within cloud. At the same time, it heavily put focus on the AI integrations they have been making for the past quarters, which are contributing strongly to Microsoft’s topline and bottom line.

One curious response on how to think their Open AI partnership:

“When we grow, it helps them, and when they grow, it helps us” (..) “it’s easiest in this situation to think about them as a customer of ours, like any other customer who would use the Azure infrastructure and our Azure AI Services in service of supporting their end customers.”

Commercial remaining performance obligation increased 26% to $196 billion. Roughly 45% will be recognized in revenue in the next 12 months, up 18% year-over-year.

For the next quarter, management expects:

Productivity and Business Processes revenue between 17.9-18.2bn, or a 10% growth. LinkedIn growth of mid-single digits and Dynamics mid to high teens.

Intelligent Cloud to grow between 15-16% to 23.6-23.9bn in revenue. Azure is expected to grow 26%.

More Personal Computing revenue of 13.35-13.75bn, a yearly decline of 6%. Search and news ads revenue should be around 10%.

COGS to grow 3-4% in cc and operating expenses 2%.

My take

I think my take is all over the article, results were wonderful in my opinion, as they have been for the past quarters. Microsoft continues grabbing share in every market they serve and has consolidated players with a huge runway ahead of them that keep delivering. Moreover, this high growth is accompanied by thicker margins and a tendency to recurring revenue.

Personal commentary

I really enjoyed putting this earnings review together, love reading about Microsoft. I’ll be covering Google, Visa, Texas Instruments and some more companies this earnings season, you can subscribe below to receive them.

Disclosure: This is NOT financial advice.

Great review, all the important data are there. Long MSFT! They are everywhere now and really important for a lot of business.

Felicitaciones por varias razones! Realmente es una investigación sobre el estado actual de la empresa. No sólo muestra números y datos sino que incluye su visión personal que es muy valiosa y desinteresada. además, para los que aún damos los primeros pasos, es aprendizaje puro! Gracias!