Burford’s business model is one of capital deployment. The company reinvests proceeds from previous investments and raises private funds to act as asset manager. Although it has temporarily escaped competition, finding refuge in the high end of the market, it is unclear how sustainable their returns are.

In this article, I’ll go over:

Similarities and differences with VC/PEs

Complete breakdown of Burford’s returns

Durability of returns

Claim families

Business Model

Burford business model resembles that of a venture capital or PE firm. Core legal finance is, essentially, purchasing an asset with an expected cash flow or stream of cash flows in the future. The asset in question is held until maturity, meaning case resolution, and returns widely vary.

That being said, there are a couple of differences between Burford and VC/PE firms, namely:

Venture capital companies have an investment horizon of 7-10+ years. PE firms, a horizon of 5-7 years. In contrast, legal cases tend to resolve in 2-3 years, on average.

VC and PE firms need to create an exit strategy to collect cash. For Burford, the legal process is in charge of that.

Litigation claims are idiosyncratic and don’t follow any strict timeline. Returns for Burford are uncorrelated between themselves and the overall economy.

VC and PE firms tend to suffer during economic recessions due to multiple contraction and cost of capital. Burford is hit by both as well. However, its business is counter cyclical. In economic downturns is when more disputes arise. And a higher cost of capital can be considered for pricing.

Burford’s returns are positively skewed due to settlements.

On the negative side, returns are somewhat capped for Burford, in absolute terms. They are necessarily tied to the cash flow generated by the win or settlement. VC and PE firms can have returns that tend to infinite, if companies do very well.

Burford Historical Returns

The metrics that are utilized to measure legal finance firms’ investments are: (i) IRR, which stands for internal rate of return; (ii) ROIC, or return on invested capital; (iii) WAL, weighted average life. The latter represents the average time it takes for realizations to occur, after capital deployment. Altogether, these three metrics help analyze how well capital is being allocated.

Burford’s historical IRR has been 27%. It’s worth noting that the YPF case, the biggest case outstanding on a Burford-only basis, at 1.3bn estimated fair value, added 5-6pp to overall IRR. On the other hand, return on invested capital stands at 87%. In contrast to IRR, Burford’s ROIC has trended upwards over time, though the YPF case has been adding 20-25pp.

Note: both metrics are computed on an accumulated basis each year.

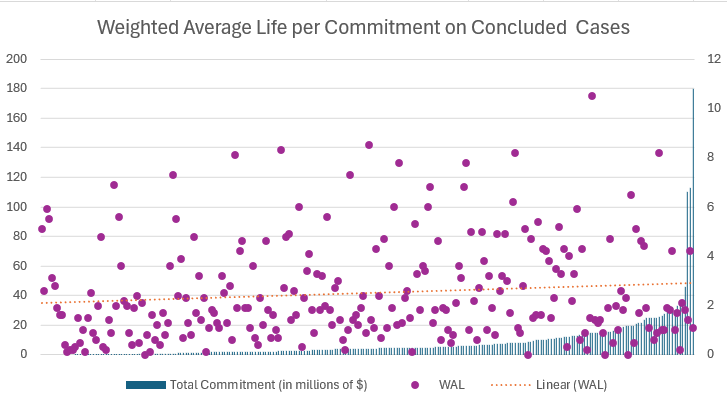

The disparity is partly explained by how much time cases have taken to resolve, either by adjudication or settlement. Average deal size has steadily increased over the past decade. Litigation Capital Management pointed out that, as size increases, the reality is that people fight harder for cases. In Burford’s concluded cases, we observe that the WAL has been in fact increasing in accordance with commitment size.

Commitment size increasing does not necessarily mean that the underlying average litigation size increases as well. However, I suspect it is the case because a large part of this dynamic is explained by monetization of claims.

In addition to this, Covid has invariably affected Burford’s time-measured performance. The closing of courts and the slowdown of legal processes have delayed the resolution of cases that would’ve otherwise been resolved earlier. In addition to this, Burford has several old ongoing investments which, as they resolve, should tend to depress total IRR.

Settlements Cause Positive Skewness in Returns

Potential outcomes in legal finance are theoretically binary. But in practice, unlike private equity, there are three potential scenarios: win, lose or settlement. Burford has committed a total of 1.52bn dollars since inception and has deployed 1.32bn. In total, the business has realized 2.48bn dollars, implying gains of 1.15bn and a ROIC of 87%. Case resolution distribution was as follows:

21% of capital deployed ended up in Burford’s backed party winning the underlying cases, producing 965M in realizations.

8% of deployments were destined to cases that lost, generating a loss of 84% of the capital deployed, or 96M.

71% of capital was deployed in cases that were resolved by settlement. Burford realized 1.5bn dollars through this mechanism, with a ROIC of 60%.

The theoretical binary outcome and confidential nature of lawsuits makes one mis-appreciate the likelihood of a favorable settlement occurring, prior to the event. Hence why this capital is expensive. Cristopher Bogart stated that, due to this dynamic, it is unlikely for returns to come dramatically down. Investors will always demand a premium.

“You just don’t see that kind of binary risk in most financial assets. And I think investors, quite rightly, will demand a premium for that level of risk. If you had a choice of investing in Burford’s assets or some distressed debt pool, and the returns were exactly the same, you’d probably choose to invest in the distressed debt pool. Because you’ve got some underlying asset value there” Cristopher Bogart interview

Furthermore, litigation financing does not give room for auction-style competition. Pricing is complex and depends on idiosyncratic, generally confidential, factors.

“The pricing associated with contingency fee lawyering often creates a pricing benchmark or expectation entirely divorced from competition. Neither the litigation finance providers nor the lawyers are generally willing to spend the time necessary to facilitate auction-style competition for investments.” Burford 2016 Annual Report

“The better way to compete is by growing in market size, as opposed to competing in price” Cristopher Bogart interview

Considering that 60-90% of disputes end up in a settlement, I believe returns will be driven by these as companies scale. If the state of nature of settlements offers good prospects, it’s expected for them to continue skewing legal finance returns. More importantly, settlements “remove risk from the equation”. On top of settlements providing the basis for returns, leftover scenarios are highly similar to equity investments. They are highly asymmetrical.

Burford’s good judgment has produced a spectrum of outcomes that does not follow the average distribution. My sense is that, as Burford scales, the law of large numbers will tilt the percentage of outcomes towards more settlements.

What we observe from concluded cases is that, similar to what occurred at the broad level, IRR has been trending downwards, but ROIC and WAL upwards. Time for resolution is expected to keep trending in this direction, as older cases get resolved and courts catch up.

Settlements have produced a 50%+ return on invested capital. Coupled with the “removal of risk”, the skewness in overall returns and uncorrelation factor, these elements illustrate the attractiveness of Burford’s operations. Correct risk assessment and management are vital for them to be present (except the uncorrelation factor, which is always present). They are consequential to managements’ skill.

Something worth keeping in mind for return dynamics is that settlements may have, on average, lower WALs. Hence, higher IRRs but lower ROICs. This is due to the fact that settlements imply discounting the certainty of resolution, diminishing risk.

On a final note, here are management’s considerations on returns and the impossibility to control them:

“the $325 million deal we did in June settled in December, at a point when we had only deployed $225 million. We made a Burford-only profit of $46 million in six months, a 37% IRR – but a 0.36x ROIC (…) The point here is that this is the way our business works. How individual cases resolve, and thus the returns in any particular period, is out of our hands, although we do endeavor to structure deals so that we are protected from duration extending. Sometimes they will resolve quickly, with comparatively low ROICs. Sometimes they will go to trial and produce superlative ROICs.” Shareholder letter 2023

Returns on Direct and Indirect Capital Provisions

Segmenting investments into size buckets should help assess the durability of Burford’s returns. Larger deals are what should increasingly drive returns moving forward. In addition to this, considering the funds alongside which the balance sheet occasionally invests sheds further light on legal finance broader returns.

“Capital provision-direct assets refer to those assets that Burford has originated directly (i.e.. not through participation in a private fund) from its balance sheet Capital provision-indirect assets refer to those assets that include Burford's balance sheet's participation in two of its private funds — namely. BCIM Strategic Value Master Fund, LP (the "Strategic Value Fund") and Burford Advantage Master Fund LP (the "Advantage Fund").”

Among concluded cases, I find that:

Overall, the weighted average ROIC has been 75%, while the weighted average IRR, 50%. The calculation was done excluding three cases whose IRR were multiple thousand percentage points

163 of concluded investments were in the 0-5M dollar range. Weighted average ROIC and IRR were 66% and 92% on these

38 concluded investments were in the 5-10M dollars range. Weighted average ROIC and IRR were 110% and 86%

33 concluded investments were between 10-20M dollars. Weighted average ROIC stood at 74% and IRR at 39%

18 concluded investments were in excess of 20M dollars. The weighted average ROIC was 70% and the IRR was 41%

The following chart was computed with deployments in concluded and partially concluded cases. Total deployments, obtained here, amount to 1.81bn. Indirect capital provisions included were done through the Strategic Value Fund and the Advantage fund.

Note: I excluded some outliers whose IRR or ROIC were well in excess of 1000%.

In Burford’s 2021 Investor Day, management shared a visual showcasing a similar dynamic on a commitment and capital provision-direct basis. On a cumulative basis, since inception, the company has seen its ROIC rising as commitment size increased.

Out of the total 1.81bn dollars deployed since inception on a direct and indirect basis, 1.27bn came from Burford’s balance sheet. Among these cases, I find that:

184 investments were above 100 thousand dollars

Burford lost the completeness of its capital in 23 investments (12.5%) and got partial recoveries in 27 (14.6%); the company realized gains in the rest of them

Overall ROIC and IRR were 88% and 24,126%. Excluding 4 outliers, ROIC and IRR were 72% and 42%

Investment distribution and returns by size was as follows:

Note: Keep in mind some capital provisions are done jointly, for which there’s an overlap element.

The remaining 542.7M were provided by the private funds, representing 107 investments. Overall weighted average ROIC and IRR for these investments stand at 84% and 64%. Burford lost all of its capital in 11 cases (10.2%) and experienced a partial loss in other 9 (8.4%). Investment distribution and returns by size was as follows:

My sense is that the disparity in returns, in spite of the overlap, can be largely explained by two factors. Namely, the nature of each investment and the exclusion of outliers on direct investments. Assets in which the Advantage Fund invests tend to have lower risk, lower returns, but shorter duration. This makes it have, on average, higher IRRs, but core legal finance offers higher ROICs.

Claim Families

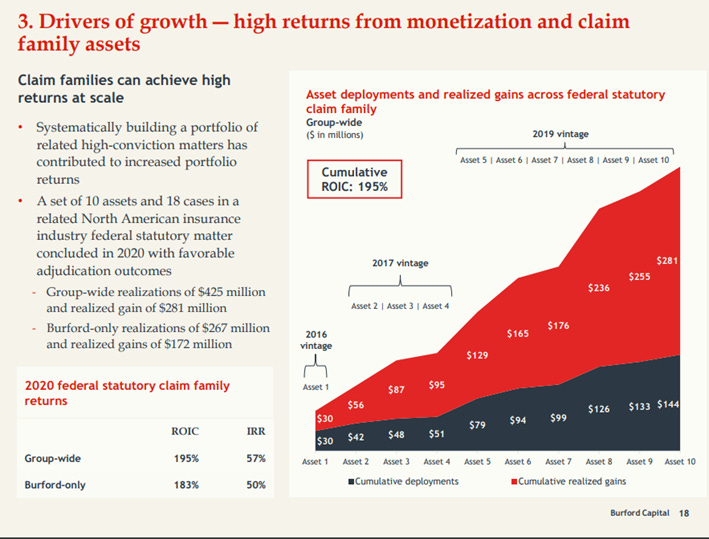

Claim families is the element that, alongside monetization of claims, is helping Burford scale. Once Burford gets familiarized with a specific claim, the incremental cost of bringing a new claim of this sort, but from another client, is very low. Claim families allow management to increase the weight of an investment they have conviction in.

“I'll give you an example of what I'm talking about. The European Commission has concluded that manufacturers of diesel trucks were engaged in an illegal price-fixing cartel. So if you're a buyer of diesel trucks, if you're a fleet operator, Tesco or somebody like that, you now have a claim against the truck manufacturers for that overcharge. That claim is going to be the same fundamental claim from lots of different fleet operators. But each claim is going to be a little bit different. Tesco maybe buys their trucks from Volvo. Somebody else buys their trucks from Mercedes. They negotiate different economic terms and discounts. So this isn't like a securities class action where all of you, if you've invested in Wirecard, have been injured in an identical way. These are all individual claims that need to be brought separately. But we can go into the market and amass a number of these claims and effectively treat them as one family of investments.”

Claim families allow Burford to diversify risk within cases of the same nature. They are a good mechanism to get the expected favorable returns. Additionally, this represents scaling with underlying operating leverage and provides agility, which might prove as a further advantage with respect to peers. Having done the due diligence accelerates the underwriting of similar claims.

“They needed to close that from the moment the phone rang, and we've been cultivating the relationship for a long, long time, 10 days from phone call to “can you write us a very large check”. We understood the claim family. We had to understand some of their underlying facts, and we were able to close that well before the 10 days.”

The following image illustrates Burford’s cumulative deployments and returns from engaging in this type of operation. Noticeably, incremental capital invested in this claim family experienced higher returns than prior deployments. For instance, asset 2 implied an extra deployment of $12 million dollars and brought in $26 million in gains.

Personal Commentary

My sense is that, out of my 5 articles on Burford, this is the one you’d get the most value from. In consequence, I opted to keep it open. This is a practice I’ll most likely repeat in the future. If you’d like to read more of my articles on Burford, here’s the link: Equity Research.

Disclaimer: This is not financial advice nor should be taken as such.

Nice work, thank you for posting!

Extremely valuable. What valuation method would.you use to value Burford?