This is the first of a series of articles in which I will cover the completeness of Burford’s business. I thought it would be better to begin with the company’s history, followed by how the legal process works, what caused legal finance to emerge, and a description of Burford’s operations. In the next articles, I will delve into the portfolio’s intricacies, the company’s financials, competitive advantage, and accountancy-related matters.

For those who might be interested, I will include the draft I’m working on, which contains 31 pages of unstructured data. The actual write-ups are the articulation of the latter. However, a large amount of information included in the draft does not ultimately make it to these reports, for which it may trigger your interest. The draft will be included after the paywall.

History

Burford Capital is a litigation finance company that was founded in 2009 and incorporated in Guernesy. It began operating in the United Kingdom and the United States. With the passage of time, the company expanded operations throughout the rest of the world. Burford was founded by Cristopher Bogart and Jonathan Molot in response to a common issue that was taking place after the financial crisis, which devastated corporations and law firms.

Cristopher Bogart graduated from Western University with a Juris Doctor degree and exercised as an investment banker at JPM, for two years, focused on project finance and insolvency. He then worked for almost 6 years as a trial lawyer, a litigator, with clients such as IBM, General Electric and Time Warner. Christopher was afterwards hired by Time Warner to serve as General Counsel and manage its legal department. It was there where he first started noticing how inefficiently was the legal industry structured.

Two years later, Bogart was named CEO of Time Warner Cable Ventures, which had 9bn in revenue, and took charge of overseeing activity related to new technology, M&A, and all investments. After two years and a half, he left to work as a Managing Director at Glenavy Capital, former investment adviser to Burford and focused on technology investments. In parallel, he started and managed a tech/media investment fund, which lasted from 2006 until 2009. While Christopher was performing both roles, he started a side-business, which he labeled as mostly a “hobby”.

Bogart was talking to a friend, who had become a partner at Latham and Watkins, a large US law firm, when he realized that his friend was facing the same trouble he did when working at Time Warner. Law firms are structured in a way that makes them largely financially inflexible. This was causing Latham and Watkins to lose several international clients. In response, Christopher, alongside a couple of colleagues, raised a small amount of capital and started financing his friend’s cases.

When the financial crisis hit, a curious thing occurred. Corporations, now facing uncertainty, which triggers a high sense for liquidity protection, started showing reluctance to pay law firms in the same way as before, on a fee per hour basis. The problem is that law firms’ business model is designed in such a way that they require a predictive stream of income. They need to count with lawyers, who charge by the hour. Hence, a large discrepancy made itself present.

Law firms knew about Cristopher’s arrangement with Latham and Watkins. In the need of accessing capital, many of them reached out to Bogart. The latter, after witnessing how much demand there was for a proper litigation finance business, had a conversation with Jonathan Molot. Both of them decided to raise institutional capital. That is the time when Burford was created.

In October of 2009, Burford did its IPO in the Alternative Investment Market of the London Stock Exchange, raising 130M dollars. A year and two months later, Burford announced a secondary placing of 100 million ordinary shares, raising an additional 175M dollars. Both turned Burford into the largest fund of its kind. In the company’s first annual report, filed in March of 2011, Sir Peter Middleton, Burford’s former Chairman, stated that the company had committed 140 million dollars for investments to date.

.Legal Process

The legal system in the United States began in 1789 when Washington signed the Judiciary Act, which established the basis for the American judicial system. American’s legal system would afterwards be based on the English Common Law, and it holds four principles as pillars: (1) Equal justice; (2) Due process; (3) The adversary system; (4) Presumption of innocence. At the same time, the American system imported the roots of English Common Law, which is in turn established upon the concept of stare decisis. This implies that courts must rule as has been done in the past, when a new case is similar to a past one.

Importantly, there are two types of general lawsuits: (1) Criminal, which is the vehicle the government utilizes to prosecute criminal action; (2) Civil cases, which encompass almost all other lawsuits. When an entity, person, or organization, finds a third-party’s action to be illegal and damaging to themselves, they are entitled to initiate a lawsuit. The initiator of the claim is called plaintiff and is usually seeking a money compensation to counteract the damage suffered. Types of civil cases include personal injury tort claims, contract disputes, equitable claims, class action suits, divorce and family disputes, and property disputes.

The process is as follows:

The first party files the lawsuits, known as the complaint or pleading. In the document, the entity needs to include the name and address of the plaintiff and defendant, the jurisdiction or reason to file in the determined federal court, allegations against the defendant and the relief the plaintiff is asking for. The latter is generally the sum of money expected.

Plaintiffs are required to serve the defendants, by law, meaning they need to provide them with the complaint and the court summons. It is not enough to send both via mail. They must be given directly to them or to a pertinent person in their office or home.

After the opposite party has been served, they are required to write an answer to the complaint and file it with the issuing court. “If you fail to answer, you could lose the case without ever having the opportunity to tell your side of the story”. Mass Gov

In the discovery phase, parties exchange relevant documentation. When one of them asks for information the counterparty is not willing to provide, the dispute is taken to court, where the judge decides whether or not such information is pertinent and if it therefore should be shared.

and 6) Both parties can request different sets of motions, including a ‘pre-trial motion for summary judgment’. Motions are utilized for requesting a determined judgment, and a summary judgment is done when the movant intends to show beforehand that there is no validity in the claim, or part of it. It is up to the judge to decide whether or not the motion is in place. Other motions might be utilized in the search of clarification.

During the trial, both parties must “present evidence to support their claims to a jury and/or judge”.

Post trial motions are requested in the same trial court and could have the intention of dismissal, asking for a new trial, setting aside the verdict, or they could be requested for other purposes.

Generally, if civil cases end in trial, they last around two years. Even though one could begin a lawsuit by oneself, it’s advisable to hire a lawyer even before the complaint is filed, for its proper writing. Clients are therefore required to pay for legal assistance all along the way until the case settles or the trial concludes. Finally, at any point in the legal process, both parties can agree to settle.

Mismatch in Desired Methodology for Payment

Legal fees tend to cost large sums of capital, ranging from tens of thousands to the hundreds of millions of dollars, depending on numerous factors. When the GFC hit and companies found themselves lacking liquidity, they couldn’t afford to continue with the fee structure that law firms prefer. In fact, many managers ended up letting go of potentially profitable claims due to the costs associated, something that still occurs.

In 2022, Burford’s report pointed out that “three of five in-house lawyers interviewed say that their companies have neglected to pursue meritorious recoveries in the prior year, with the cost of pursuing claims, judgments and awards a deciding factor.”

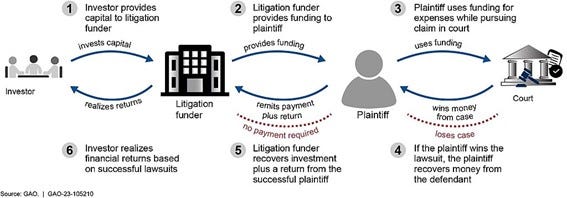

Law firms’ business models are very headcount intensive. They hire lawyers and pay them by the hour, making their costs mostly fixed when combined with the needed RE footprint. Consequently, their desired methodology for charging is an hourly fee, irrespective of the case’s development. To the contrary, clients/corporations, incline towards a contingency fee basis, where the payment is in accordance with the law firm’s merits. The crisis made them have no alternative at the moment, but thereafter, corporations’ preference for this approach strengthened. This occasioned a mismatch between both parties’ desired methodologies, and it is mostly the reason why litigation finance emerged.

Importantly, the term litigation finance is meant for single cases, whereas legal finance is how the industry is called now, due to the existence of numerous other avenues for investments within the sector. Litigation finance implies for an investor to provide funding to the plaintiff or law firm in exchange for a share of the proceeds if the case ends up being a success, plus some extra clauses. In this context, litigation claims are viewed as an asset that would provide a single or stream of future cashflows.

An industry-wise consequence this has had is that more law firms can now compete for cases that are set on a contingent/performance, or an alternative fee basis. On the corporate side, not having to pay for legal fees helps companies get liquidity and utilize it within their realm of operations, where their expertise lies. This way, businesses are liberating operating capital.

Moreover, legal expenditures are accrued as operating expenses, depressing companies’ profit margins and hence altering the financial community’s perception of value for the business. Lastly, accounting rules don’t allow for litigation claims to be included on the balance sheet, making the payment for them through the p&l a value destroying exercise from an accounting perspective.

“When you do litigation finance on the plaintiff side, you are providing the company with a permanent solution to its p&l. In other words, if you don’t do litigation finance, and I’ll attend to my 100 dollars example, that 10 dollars is going to flow through your income statement as an expense and it’s going to reduce your profits. And therefore it’s going to reduce your market value somewhat. If I take that expense away, because I take it, it never comes back to you. Either you lose the case, or you win the case, in which case you get a net recovery.

If you do this on the defense side and you win the case, I of course am going to be wanting my capital back. And that is going to flow through your P&L. And so, as a result, it is somewhat less appealing because you’re getting a deferral and risk management, but not a permanent P&L solution” Christopher Bogart

As legal finance grew, the compensation scheme for the funder evolved. Some might now include several other elements, such as, for instance, a clause for the recovery of the capital provided, or a multiple of it, plus a share of the proceeds. In Burford’s 2022 annual report, management mentioned that, upon the conclusion of a successful claim, Burford would receive its funded capital plus, generally, a combination of the following: “(i) a time-based return; (ii) a multiple of our funded capital that may increase over time; (iii) an entitlement to some percentage of the net realization that may increase or decrease over time or may depend on the size of the total resolution amount”. The latter makes management think of delays in matters as a “deferral of income rather than its permanent diminution”.

Contracts are specifically designed to address each particular case, which makes the use of all or any of the three points not a requirement. Moreover, the more complex the case, the more taylor-made the contract will be. The objective is for all contracts to not only provide Burford with a positive expected return, but to account for risks and align incentives towards rational action, which is differently targeted in each case, as cases are all idiosyncratic.

The entity in charge of paying for the litigation is generally: “(i) a government or a state-owned entity, (ii) an insurer or (iii) a large company in an industry less likely to be rendered insolvent by economic disruption associated with increases in interest rates”.

Within this context, Burford offers two specific products and services: core legal finance and alternative strategies. Even though the tasks performed under both of the latter differ in nature, they also differ risk/return wise. The ‘alternative strategies’ business supposes, in general, lower risk and potential return, and is mostly aimed outside of pre-settlement matters.

To effectively pursue each activity, Burford operates through a series of private funds, which are wholly owned subsidiaries and focus on a specific approach. Altogether, Burford operates under three areas, which management believes compose their addressable market:

“The value of litigation claims and the enforcement of settlements, judgments and awards

The amount paid to law firms as legal fees and expenses

The value of assets affected by litigation”.

Core Legal Finance

Burford’s core legal finance segment is in charge of providing capital and advisory to corporations and law firms. Fundamentally, it’s exclusively focused on pre-settlement matters. The company works with some of the world’s biggest law firms and corporations and has received inquiries from 93/100 largest law firms, by revenue, within the US.

Importantly, the range of investments that core legal finance encompasses is extremely broad. The risk and expected return from a case depends on the stage of the litigation process, the number of parties involved, the amount of litigation matters included and whether Burford funds the corporation or the law firm. The company can deploy capital into cases that have not yet been filed or into those whose final judgment has already been reached. At the same time, Burford provides capital both for funding legal expenses and for monetizing the future value of claims, offering an upfront payment to clients. In addition to Burford’s balance sheet, and as a general rule, the private funds they use to deploy capital into core legal finance are BOF, BOF-C, BCIM Partners II and BCIM Partners III.

In return for funding the cases, Burford contractually sets itself to receive a share of the proceeds the ultimate settlement generates. If the case is lost, Burford generally loses its capital. When funding multiple assets—claims—made and held by the same client, the agreement tends to contemplate the lower risk that a portfolio of claims entails compared to that of a single case.

The portfolio approach allows Burford to provide capital on a more efficient basis and clients to fund cases they would not be able to fund otherwise. I suspect that smaller cases might be more easily funded this way and that the law firm/corporation gains pricing power due to the lower risk for Burford, hence improving the overall deal for them. It might be otherwise difficult to convince a respected legal funder, with scale, to commit capital for a single-and-small case.

Note: A commitment is the capital that Burford has agreed to provide to a corporation or law firm.

Insurance Business

In addition to providing capital for the funding of legal claims, Burford also owns a legal insurance business, which they acquired in 2011. When cases finalize, the loser is generally obligated to pay for the winner’s legal expenses. To mitigate such risk, Burford offers customers to pay for these adverse costs if required. If the insured party wins, Burford is entitled to collect a premium, correspondent to a percentage of the cost’s risks.

“Our operating profits from this business have exceeded $81 million in aggregate since 2011 against an acquisition cost of $19 million” 2020 20-F

In 2016, a falling demand due to regulatory changes as well as increasing platform costs made management terminate their arrangement with MunichRE and stop writing new business. Premiums that remained in the portfolio kept being managed accordingly and producing profit for several years.

In 2018, Burford re-entered the insurance business with their wholly owned insurer: Burford Worldwide Insurance Limited. The latter is aimed at the high-end of the market, as opposed to before. Burford takes 20% of the insurance risk and contracts to take remaining reinsurance risk.

Note: Reinsurance is insurance for insurance companies.

Finally, in 2018, management claimed BWIL would only write coverage for matters they are financing, enhancing Burford’s suite of solutions and making it more appealing to clients.

“The insurance business has written almost 57,000 insurance policies to cover adverse costs risk during its life. Of those matters, 77% have resolved favorably and only 21% have suffered losses (and 2% remain unresolved). That represents an enormous body of litigation assessment data and experience in addition to our core business” 2018 Annual Report

Alternative Strategies

The second main offering Burford has is called alternative strategies. With this set of assets, management aims for lower risk and return than core legal finance. Alternative strategies are composed of:

Lower risk legal finance: this business is focused on pre-settlement matters. In contrast to core legal finance, assets that are included here are perceived as carrying less risk and lower expected returns due to structural or other reasons.

Post-Settlement: When both parties settle, the monetization each of both is titled to might take a considerable amount of time to come. Generally, the judicial process delays such monetization. However, the payment is due and is ‘certainly’ occurring. In an attempt to help corporations and law firms materialize the funding at an earlier stage, Burford provides them with capital in exchange for the completeness or part of the future claim. A similar logic is applied when speaking of a stream of payments that are due to a certain party.

Additionally, Burford offers law firms the chance to purchase their receivables, especially at the end of their fiscal year, when legal firms require capital to pay to partners.

Complex Strategies: When management encounters an asset associated with a claim they believe is mispriced, they acquire it. Thereafter, Burford takes full control of the asset, becoming the owner, and manages the claim actively. Complex strategies are carried out through the Strategic Value Fund, which focuses on merger appraisal situations. Depending on context, Burford might long or short equity securities as well. The Strategic Value Fund has deployed no capital in 2021 and 2022, and management expects it to continue this way in the short term.

Asset Recovery: When a matter has been litigated through a final judgment, after which there are no longer more appeals possible, “the judgment is enforceable as a debt obligation of the judgment debtor”. Even though most litigants pay on time, some do not. In such cases, Burford offers clients the possibility to monetize the claim beforehand and puts effort on collecting the debt.

Asset Management

Although Burford had been historically able to grow its capital base at a rapid pace by issuing debt and due to the high returns on capital they’ve had, demand for legal finance was still in excess of their supply capacity. Taking this into consideration, management decided to acquire the largest investment management firm in the industry in 2016, called Gerchen Keller (GKC). For the latter, the company paid $160 million in cash, shares and loan notes.

GKC brought with it four private closed end funds with total commitments of 1.1bn dollars. Additionally, GKC’s investments were broader in nature than that of Burford. The latter was completely focused on core legal finance, investing in pre-settlement matters. Alongside GKC, Burford got to expand its avenues for investments, including things such as post-settlement thereafter. For managing private funds, Burford earns a management and performance fee, both of which depend on the fund and are detailed in the asset management image.

Burford has been utilizing its balance sheet to invest alongside these private funds ever since. At the beginning, Burford agreed with GKC that the first $15 million of commitments in pre-settlement matters would be split in half and half between both. Commitments that exceeded the first $15 million would be taken by Burford’s balance sheet until it reaches the risk tolerance level. After this point, the fund would be entitled to invest.

In their 2022 annual report, Burford stated that they generally utilize the balance sheet to invest in 75% of new core legal finance assets, while leaving the remaining 25% for the private fund called BOF-C. Importantly, the latter is a fund through which a sovereign wealth fund invests in pre-settlement matters. It is worth noting that the allocation distribution has varied over the years.

On the other hand, 100% of the allocation in lower risk legal finance assets is done through the Advantage Fund, in which Burford’s balance sheet is an investor. Allocation to post-settlement matters is 100% done through BAIF II, a private fund. Complex strategies are 100% done with the Strategic Value Fund, in which Burford’s balance sheet is also an investor. Finally, the completeness of asset recovery investments is done through the balance sheet.

“Although we manage each of COLP, BAIF and BAIF II and receive asset management and performance fees, we are not an investor in COLP, BAIF or BAIF II and, as a result, none of COLP, BAIF or BAIF II is consolidated for purposes of our consolidated financial statements.” 2022 Annual Report

Burford generally manages their private funds through limited partnerships. Private funds that are LPs have a general partner that’s Burford-owned. The latter is in charge of administering their respective fund, conducting operations and selecting the assets in which to invest. Importantly, “the limited partners of the private funds take no part in the or control of the business of the private funds, have no right or authority to act for or bind the private funds and have no influence over the voting or disposition of the securities or other assets held by the private funds”.

Origination and Underwriting

Burford continuously receives inquiries from corporations and law firms. Upon their receipt, the team performs a high-level screening process in order to filter potentially good opportunities and get them into the pipeline. After this occurs, the case is assigned to an individual underwriter who then performs exhaustive due diligence, covering both legal and factual standpoints. In parallel, Burford utilizes a quantitative probabilistic model that leverages proprietary and third-party data to infer a case´s expected value.

If the underwriter arrives at the conclusion that the claim is worth pursuing, they present it to the Commitments Committee, whose task is to accept or reject the opportunity. If the committee decides to proceed with the investment, the underwriter negotiates the terms with the counterparty in order for Burford to properly make the commitment.

This is a process that’s overseen by multiple people and teams within Burford, which forces potential cases to go through a chain of parties, all of whom review it and decide to proceed or not:

“There is someone that is going to be underwriting this memo that I described, but at the same time, we are not going to make an investment until a lot of people with a lot of experience have reviewed this matter and said yes to it. So, at the end of the day, I am responsible for every investment that we make. John is just as responsible” Cristopher Bogart

After the commitment is done, the method of funding varies. One of the possibilities is for Burford to make a complete upfront payment, or to provide the funding overtime. Further, undrawn commitments, meaning the not-yet paid part of the committed capital, are cataloged as discretionary or definitive. The difference between the two lies in whether Burford is contractually obligated to provide the rest of the capital commitment or not.

Personal Commentary

Burford is a fascinating business to read about. The next 2-3 articles will be on this company and perhaps I’ll publish a short write-up on Winmark in 2 weeks. I’m trying to increase production.

Contact: Giulianomana@0to1stockmarket.com

Disclosure: This is not financial advice