Zoetis reported results on November 2nd. The company generated 2.15bn in revenue during the third quarter, growing 7.4% on a yearly basis and exhibiting a 4yr CAGR of 7.9%. Zoetis revenue growth had been decelerating for a couple of quarters, mainly attributable, in my opinion, to the excess demand it experienced during 2021. In an industry that tends to grow at 4-6%, achieving 20-25% growth rates do nothing but pull demand ahead in time. Ever since, growth had slowed and stayed below 5% during 2023.

Gross profit for the quarter was 1.513bn, slightly outgrowing revenue. Its respective margin expanded 60bps YoY and declined 190bps QoQ. The latter is of no concern given Zoetis’ GPM tends to oscillate between 68-72%. I suspect this is due to the sales mix of each quarter, which should come as no surprise considering how vast of a portfolio Zoetis has. Operating income was 798M for the quarter, implying a margin of 37.1%, which expanded 90bps YoY. Lastly, the company generated 596M in net income, with a net profit margin that increased 130bps YoY to 27.7%.

Turning to the cash flow statement, Zoetis generated 724M from operating activities. Investments in inventories and working capital are partly why I stated last quarter that no conclusions should be drawn from Q2’s cash from operations, which seemed unusually low. Furthermore, the company continued investing in capacity, with this quarter’s CapEx being at 145M. This puts YTD cash from operating activities at 1.45bn, whereas capital expenditures amount to 534M.

Capital expenditure’s guidance, however, was lowered for the year, which somewhat fueled free cash flow for the quarter and will play some role as well in Q4. Management had previously guided for 950M-1bn of CapEx for 2023, but they have now guided for 725M-750M. Joseph ascribes this to timing, meaning CapEx was simply pushed forward, perhaps for 2024.

Moving forward, we’ll break down Zoetis revenue as I see would add the most value. Firstly, I must highlight that the trend in revenue by geography is one to keep a close eye on. Geographical diversification can prove very advantageous in moments of economic turbulence. However, Zoetis’ focus on companion animals should tilt concentration towards the US in the long run. This Q, Zoetis derived around 54% of its revenue from the US and the other 46%, internationally, which has been mostly the case for at least the past 4 years.

In the broad sense, Zoetis differentiates among two major group of animals. During the quarter, revenue generated selling products meant for companion animals was 1.41bn dollars, up 11.2% on a yearly basis. There was some pullback compared to last quarter, which I suspect was due to the unusual growth Librela and Solensia experienced during Q2, alongside Trio’s demand. On the other hand, livestock revenue was 716M, growing 1.1% YoY. Companion animal products now generate 66% of Zoetis’ total revenue, increasing from a 50% share four years ago.

Zoetis distills revenue by major product categories. A slight overview of all of them to then dive into the most relevant ones:

Parasiticides did 465M in revenue, increasing 10% YoY

Dermatology revenue was 397M, up 14% YoY

Vaccines generated 449M during the quarter, flat on a yearly basis

Other pharmaceuticals revenue grew 24% YoY to 313M

Anti-infectives revenue decreased 7% YoY to 264M

Zoetis’ diagnostics segment did 95M in revenue, up 14.4% YoY

The two categories I’d like to double-click on are the ones that have seen a lot of momentum during the past years: parasiticides and dermatology. Within the former, Simparica Trio is the product that has been carrying the segment forward. This quarter, Simparica Trio generated 206M, growing 20% on a yearly basis.

On the other hand, what’s curious about the dermatology market is that Zoetis has held a monopoly since 2013 and no competition has emerged, which continued being the case this quarter. Revenue for dermatology grew 14% YoY and 10% QoQ to 397M, driven by Apoquel and Cytopoint. As a pertinent sidenote, Apoquel Chewable was released in the US during this quarter. The four-year CAGR for both segments stand at 17.6% for parasiticides and 15.6% for dermatology.

The last category I’d like to put the spotlight on is in Zoetis other pharmaceuticals, as curious as it sounds. In here, the company includes pain and sedation products, which means Librela and Solensia, essentially. The smallest individual segment management discloses is medicated feed additives, which did 86M in revenue. Perhaps OA pain products are not far from being disclosed individually as well.

Anyway, since the launch in EU, both products have been gaining a lot of traction, with Librela having generated 50M in revenue during the quarter internationally, growing 61% yearly. On the other hand, Solensia international sales were 12M during the quarter. Lastly, Librela was launched in the US in October and, alongside Solensia, generated 15M in sales, making global OA pain revenue 77M for the quarter.

Capital Returned to Shareholders

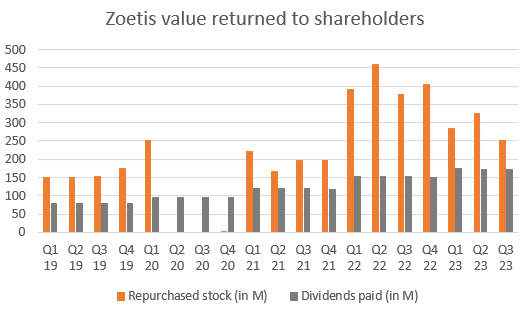

During the quarter, Zoetis repurchased 250M worth of shares, putting LTM repurchases at 1.26bn, and leaving the repurchase program at 1.7bn remaining. This quarter’s buybacks were done at an average price of $181 per share. At the same time, the company paid dividends for a total of 173, making the total value returned to shareholders 423M for the third quarter.

Acquisitions During the Quarter

Zoetis did two acquisitions. The first of them being small and not having any material impact on financial statements, but the company is adivo GmBH. Adivo is a German company that focuses on “discovering species-specific therapeutic antibodies for pets”. The acquisition should help Zoetis further advance on oncology, something they mentioned as a potential growth driver in their investor day. Here’s a useful press release.

The second acquisition was a much more meaningful one. Zoetis acquired PetMedix for 111M. Interestingly, PetMedix team is leveraging monoclonal antibodies, alike Zoetis for Librela and Solensia, for developing species-specific antibodies that would help pets deal with some diseases. Among these, cancer and arthritis.

Instead of an ahead-of-time judgment, I encourage you to read what I wrote about their previous series of acquisitions. Here’s the link. As a form of disclosure, I trust their capital allocation skills and more so given the image shared and the potential higher margins we could expect.

Management Commentary and Outlook

Management was very optimistic. The business is growing healthily across several verticals and the most relevant of them are still in the double-digit range, with many of them accelerating. In fact, the team has indirectly reiterated their mid to high single digit growth rate for next year given how things are trending. Further, they are “very excited about 2024”. In any case, the main points of discussion were three, I’d say.

Most importantly, the OA pain portfolio (Librela and Solensia) have seen spectacular receipt by vets and consumers. During the quarter, Librela was tested in the US and finally launched in mid-October. Both products have generated sales of 15M in the US, suggesting very strong adoption from the general public. This is the reason why the team has been building their inventory for the past couple of quarters. In this business, reputation is essential. There was a time (2013) where Zoetis hadn’t met customers’ demand and that was an authentic tragedy. It severely hurt the Apoquel brand, which was the product being released. Afterwards, management has remained committed to delivering on expectations and, therefore, emphasis has been placed on building inventory and capacity for properly supplying Librela and Solensia.

The second main point of discussion was Zoetis’ direct to consumer initiatives. Management repeatedly mentioned that growth in products such as Trio and the dermatology portfolio were being driven by DTC efforts. In their investor day, earlier in February, I think they mentioned awareness as a potential avenue for continuing enhancing sales. This came rather curious to me, but it’s logical. Of nothing is worth a products that your customers are not aware of. Therefore, initiatives for increasing awareness should continue propelling demand.

Finally, an unusual amount of time was dedicated to competition. On dermatology, management mentioned they expect competition for the second half of 2024, though I think they’ve said this a couple of times in the past and no competition arrived. In any case, they are confident on Apoquel and Cytopoint’s brands to protect their market share. On parasiticides, Joseph mentioned a “recent competitive launch in the triple combination space”. He stated being confident on their ability to compete.

This article goes over Boehringer Ingelheim release of NexGard (Trio’s competition)

Turning to Zoetis’ outlook, the full year guidance for operational growth was narrowed to the mid-point. Management expect sales for 2023 to be between 8.475bn and 8.55bn, implying an operational growth of 6.5%-7.5%. Net income, on the other hand, is expected to be between 2.38bn-2.41bn. This implies that last quarter’s revenue is expected at 2.14bn-2.21bn, and net income between 561M and 596M.

My Take

Zoetis had a fantastic quarter. When I read the press release and listened to the call a month ago, I thought it was okay. Now that I have dived further, I think it’s much better than okay. The company’s topline returned to healthy growth and the companion animal group got back above the double-digit range. Accompanied by Joseph and Kristin’s optimistic tone for 2024, the near term looks decent at least. Furthermore, US sales share of total ticked upwards this quarter. I expect both of these to continue on this path and believe it would be fantastic for it to happen.

Management’s focus on companion animal products has the direct effect of continuing to drive margin expansion. US products are sold at an 80% gross margin, whereas international ones operate at 68% margins. A large component of this is due to the fact that the US business is the one that encompasses most of the companion animal sales. That is why management stated in their investor day and across conference calls that companion animal sales should continue enhancing the bottom line over the long run, and it’s the reason why they guided so.

Regarding the OA pain portfolio, I’m delighted to see how rapidly that business is growing. Not for the growth itself, but because it says wonders about management’s decisions and estimates. Prior to this being a hundred million dollars business, they stated that they foresaw an addressable market of around 1bn dollars for Librela and Solensia. They reiterated this quarter after quarter and in their investor day. Spotting such cases allows the team to deploy capital accordingly, and a rapid adoption only validates their hypothesis.

The last two things I’d like to mention are regarding management’s willingness to invest against short-term margin pressure and on competition. About the former, the company’s actions had been analyzed with skepticism over the past couple of quarters, especially when speaking of their inventory management. I think they proceeded well and Librela’s receipt in the US indicates points in that direction as well.

Lastly, competition is perhaps the dark point of the quarter. Time will tell whether Boehringer’s product is superior to Simparica Trio. But, in any case, brand value is very relevant in the animal health space, or at least that’s my hypothesis. It will be good for this it to be tested. Moreover, even if BI grabs market share, Zoetis is not Simparica Trio. It is the vast portfolio of offerings that tilts me towards Zoetis, making “relevant headwinds”, such as this, somewhat less important in the grand scheme of things. Growth elsewhere can more than offset it.

Personal Commentary

I’m trying to catch up with earnings reviews. I hope you enjoyed this one and will try to get Texas Instruments, Visa and Mercado Libre for the coming weeks.

Contact: Giulianomana@0to1stockmarket.com

Disclosure: This is not financial advice and should not be taken as such.

I think your quarterly reviews are great Giuliano! Detailed but not wordy, and has all the important details. I doubt most equity analysts can do better than you.

Great review! Zoetis have a strong brand recognition inside of the veterinarian world because of the year's of commitment and development. If they can continue this trend, in the long run they should be able to gain market share and competitors will be leave behind.