Zoetis is the global leader in the animal health industry. It discovers, develops, manufactures and commercializes medicines, vaccines, diagnostic products and services. Zoetis counts with over 300 product lines, with 15 of them generating over 100M in annual sales. The latter are called blockbusters, and the company holds a third of the industry’s total.

It is important to note that the animal health industry has spectacular fundamentals for incubating long-term compounders. There is no company that competes only with generics, competitors take a rational approach to pricing and most products have an addressable market of 1M dollars or less and require to go through an FDA approval, disincentivizing competition. Furthermore, it has huge upfront and associated R&D costs. Manufacturing plants cost hundreds of millions of dollars, it is very resource-intensive and a very large sales force is required for distribution. All of this translates into each vertical generating space for virtual monopolies and helps products’ have a long lifecycle. As a reference, Zoetis’ portfolio of products has an average life of around 30 years.

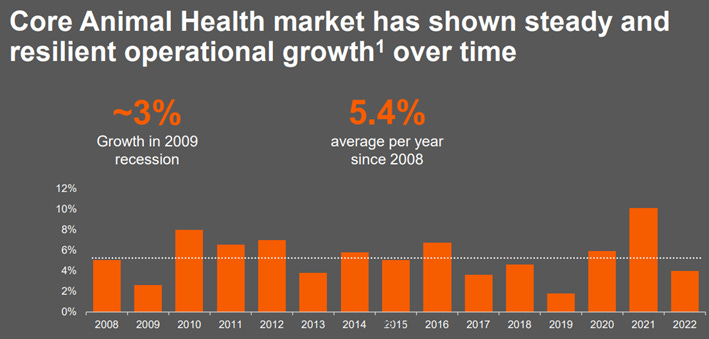

Tied with the company’s thesis, the animal health industry is extremely resilient. The reason for the latter is largely because of the human-pet bond, which severely strengthened throughout the past decades. More than 90 percent of pet owners view their pets as members of their families. Additionally, studies suggest they are willing to keep spending on their pets’ health even after a 20% income cut.

Management has shown great efficiency to operate their supply chain and allocate capital. Ever since going public (spin off from Pfizer in 2013), the company’s operating margin expanded by 2500bps, now being at 36%, developed 9 out of its 15 blockbusters, launched Simparica Trio and Apoquel Chewable, both dimension-wise innovations, and outgrew the industry.

Furthermore, they’ve proven phenomenal ability to engage in M&A operations. Zoetis has successfully entered the diagnostics space, which promises double digit growth, with a large acquisition in 2018. Several acquisitions were made in the fish segment, allowing Zoetis to enter aquaculture, an industry that’s expected to keep healthily expanding. Lastly, my hypothesis is that an 85M dollar acquisition the team did in 2017 drastically helped Zoetis release two products in 2021-22 with an estimated addressable market of 1 billion dollars.

In conclusion, Zoetis is a company immersed in a very resilient industry that’s set for decent long-term growth and holds a leading position. On this front, I would like to highlight that, during their 2023 Investor Day, management guided for above-industry growth in the next five years, with improvements in the bottom line. The company’s broad portfolio of products provides proper diversification and there are some of them, such as Librela and Solensia, which make up for these two products above mentioned, that should allow the business to keep growing in the mid-term.

Contact: giulianomana@0to1stockmarket.com

Disclosure: This is not financial advice.

Giuliano, great idea for these one pagers. Easily digestible and helps build an understanding of the business behind the name. How often are you planning to do them? - Thanks