In 1983, Martha Morris wanted to pursue her new interest and bought camping and backpacking equipment. However, she quickly realized she didn’t actually enjoy it. Shortly after, Martha tried to sell her equipment, attempting to do so by talking to shop owners. One of these retailers told her they didn’t sell used equipment.

Noticing there was no supply for her need, Martha decided to start Play it Again Sports. The idea was to build retail stores with a “garage sale-looking environment” to captivate franchisees who would like to sell used products.

In parallel, Ron Olson and Jeffrey Dahlberg started a consulting firm in 1986. Martha was one of the first customers they had. After noticing the success and potential of her idea, Ron and Jeffrey bought the rights for Play it Again Sports in 1988. This became Winmark’s first division, then called Grow Biz International.

By the year 2000, the company had opened multiple lines of franchises but was severely struggling financially. John Morgan took over as CEO and turned the business around. He sold the company’s corporate headquarters, three franchises’ rights and re-built the organizational structure, replacing most people. Winmark went from an $8.5 million loss in 1998 to consistently profitable after 2001. Morgan led Winmark until he stepped down in 2016, when Brett Heffes replaced him. Brett continues to hold his position as CEO of Winmark.

Business overview

Winmark is a franchisor focused on sustainability and small business formation. They ‘champion and guide’ entrepreneurs interested in operating one of their five resale franchises:

Play it Again Sports (began in 1988): Buys and sells gently used and new sporting goods, equipment and accessories.

Once Upon a child (1993): Buys and sells gently used children’s clothing, toys, furniture, equipment and accessories. The primary target is parents with children under 12 years.

Music Go Around (1994): Buys and sells music instruments, both gently used and new, speakers, amplifiers, and music-related electronics.

Plato’s Closet (1999): Buys and sells gently used teenagers’ clothing and accessories. The primary target is mostly teenage girls.

Style Encore (2013): Buys and sells gently used women’s clothes, shoes, and accessories. The primary target is women between 20-50 years.

Each of these work by buying ‘gently used’ items from customers and re-selling them. People that sell the items can receive cash or a higher amount in credit store. Some of these franchises also sell online. On average, it is estimated that Plato’s Closet pays customers around 30%-40 of the price they’ll be selling an item at. The other franchises operate similarly.

Management is very selective of the people with whom they do business. Several requirements need to be met for a person to be considered as a potential operator. The company seeks franchisees who:

Have a sufficient net worth. For example, to operate a Play it Again Sports store, operators are required to have a net worth of 400,000 dollars and 90-105k in liquid assets.

“Play It Again Sports expects franchise candidates to have an approximate investment of $300,000 to $410,000 to open a store”

Prior business experience.

Intend to be integrally involved in managing the store. This implies operators cannot open one as a hobby. Rather, they need to run the store full time. At the same time, they are required to sign a non-compete agreement.

Winmark has partnerships with different businesses for each brand. When franchisees buy new products, a portion of them need to be bought from these set of partners. Nonetheless, the majority of the products sold are bought from customers.

Once Upon a Child, for instance, buys approx 30% of new products from 4 partners. MGO, 50% from 5 partners. No significant vendors in Plato’s Closet nor Style Encore. On the sports brand, no number mentioned.

John Morgan Shaping the Culture

John Morgan crafted Winmark’s brand and culture. When he sold his business to TCF, he asked for equity in exchange, for John considered TCF to be undervalued. After the stock did fantastically over the subsequent years, Morgan and his partner became very rich. Shortly thereafter, both began an investment firm. Morgan was soon called for a meeting with Grow Biz’ management and large shareholders. They wanted him to take over as CEO. John agreed, but on one condition:

“It wasn’t going to be groupthink. It was going to be my way or the highway”

Morgan recalls having found an absolute mess in Winmark. By 1998, the company had more than 1,200 franchises, but growth started slowing down, which is when the bleeding started. In 1999, revenue declined 32% and, after having 7.2M dollars in net income in the previous year, the company reported a loss of $8.5M. John Morgan’s employment agreement started in 1999 and, in the year 2000, Winmark had a loss of $350,000.

Once John took over, he did a complete turnaround. Grow Biz International was renamed as “Winmark”. Morgan shut down three lines of franchises the company previously offered, namely: (i) Computer Renaissance, computers resale; (ii) Retool, consistent of tools resale; (iii) It’s About Games, which was disposed and Winmark recorded an asset impairment of over $11 million. Computer Renaissance was sold for $3 million and Retool, 3 years after being acquired, dissolved. Moreover, John Morgan decided to sell Winmark’s headquarters. Koch Trucking bought the property for $3.5 million.

Prior to Morgan joining, the team had acquired the franchising rights of Plato’s Closet. As soon as John took over the firm, he realized the potential this franchise had and decided to bet heavily on it. As of 1999, Plato’s Closet had a total of 5 stores, which scaled to a couple hundreds in the subsequent 15 years. Morgan kept three other franchises: Play it Again Sports, Music Go Round, and Once Upon a Child.

In addition to all of this, John completely changed the business’ strategy. Grow Biz used to give franchises to whomever had the money to open one, independent of their capabilities. Furthermore, the majority of the company’s topline was generated by selling products to franchisees. Morgan decided to award franchises, instead of giving them away. Winmark started intensely screening for candidates and placed more emphasis in helping them thrive. At the same time, Winmark would no longer generate most of its sales by selling products to franchisees, but rather by charging a royalty fee.

When John Morgan was appointed CEO, he was awarded 600,000 options to buy stock at $5 per share, which would vest over the subsequent five years and expire in 2006 if unexercised. Morgan made full use of the options. Thereafter, he was awarded no more options and complemented this with continuous purchases of Wina’s shares in the open market. Throughout the years, John got to own 34% of Winmark’s equity in 2013, equivalent to over 1.7 million shares.

Another peculiarity this man had is that his compensation was the lowest among executives. In an interview, Morgan highlighted how he was aligning incentives between everyone within the company.

-Interviewer: Is your share-buying a slow way to take the company private?

Morgan: I want the company to be public. To motivate the employees, it has to be a public company. Stock options are the best way for them to grow their net worth.

-Interviewer: The Winmark March 2013 proxy disclosed that you and your top three managers all earned the exact same salary ($267,250) and exact same bonus ($267,250) for fiscal 2012. Why the same?

Morgan: You don’t do things just because you can. You do things because you have a reason to. And my reason to do this is that this motivates them. It works.

Winmark does not have an IR team and management do not do conference calls. Quarterly press releases and annual reports are as short as it gets. Hereafter, I will dive into:

The Franchise Agreement

Winmark’s historical financials

Trends worth paying attention to

How the business has evolved

The closure of the leasing business

Capital allocation policy

Winmark’s current position and Brett’s vision

The franchise agreement

To open the first store, managers have to pay a fixed fee of $25,000 in the US and 34,000 CAD in Canada. To open subsequent ones, the fee drops 40% to $15,000 and 19,200 CAD. Typically, stores open 10-14 months after signing the agreement.

The initial term is 10 years with the possibility of 10-year renewal periods and provides the franchisee with an exclusive geographic area. Management reports to have 2,800 available territories. Franchisees are then required to pay weekly continuing fees, namely royalties, equal to a percentage of their gross sales, generally between 4% and 5%.

Winmark has three further requirements for franchisees, namely: (i) each franchisee needs to pay Winmark an annual marketing fee of 1,500 dollars; (ii) they are required to utilize Winmark’s operating system for managing the store; (iii) 5% of their gross sales need to be spent in advertising and promoting the store. There’s the possibility of extending the latter to 6% and destine 2% to an advertising fund, which Winmark manages.

Moving past the agreement, the company helps franchisees succeed with:

Training. Each new manager is required to attend two training programs regardless of prior experience. They are instructed on how to actually run the store, including “how to evaluate, purchase and price used goods directly from customers,” which implies learning how to use the software.

Support for opening the store and ongoing assistance.

“Our franchise support personnel visit each store periodically (in person or virtually) and, in most cases, a business assessment is made to determine whether the franchisee is operating in accordance with your standards”. They also help with operations.

Franchising Numbers

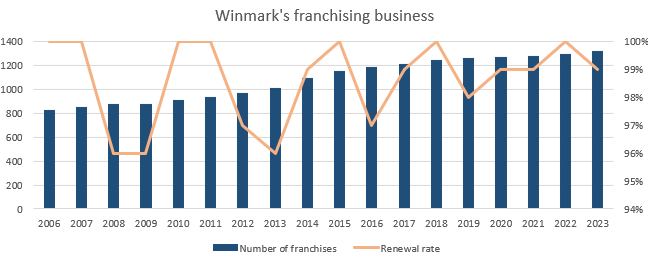

The franchising business has been doing fairly well since Morgan took over. The number of stores have grown from 824 in 2006 to 1319 in 2023 with 89% being in the US. More importantly, the renewal rate for finalizing agreements has averaged 98.6% over the same period. Such a high renewal rate illustrates how solid each partnership is, which is fundamental for turning each store into a long-enduring productive asset for Winmark.

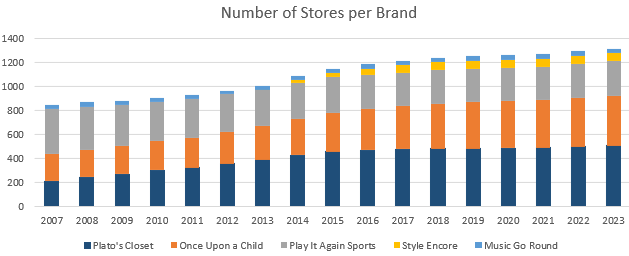

The two brands that have been mainly fueling Winmark’s growth are Plato’s Closet and Once Upon a Child. The former has grown store count at a 6.2% CAGR since 2006, now representing 38% of total stores, up from 33%. Once Upon a Child increased its footprint at a 3.9% CAGR, from 214 stores in 2006 to 416 as of last year. It is worth noting that Play it Again Sports store count declined from 388 stores in 2006 to 273 in 2021. Thereafter, growth restarted.

Total store count growth has been relatively stable. An average of 49 stores were opened every year since 2010, while each year has finalized with an average of 62 signed agreements for opening new ones. I suspect the increase that has occurred throughout time is mostly due to management’s focus on opening “quality stores.” Growth is sacrificed in pursuit of building a reliable chain of operators. It is interesting to note that headcount had barely grown until 2017. Thereafter, coincidental with Brett becoming CEO, employee count has fallen from 107 to 83 in 2023.

I suspect this element starts to show the nature of Winmark’s business, one which I find extremely appealing. Winmark does not require capital to grow. Capital expenditure is not incurred by them and no extra operating expenses are required for scaling. The only problem I may point out is that a fixed headcount will not allow for rapidly scaling store openings without sacrificing quality. A yearly ceiling may be reached, which may have already happened.

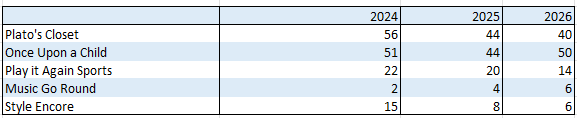

Winmark finalized 2023 with 71 signed agreements, most of which are expected to open in 2024. At the same time, a total of 146 contracts will be ending in 2024, all of which are subject to renewal. In the subsequent two years, 120 and 116 agreements will be expiring. The following table displays this dynamic for each brand.

Winmark provides people with the average revenue each franchise generates as well as the gross margin at which they operate. Further, it’s mentioned the product mix they had. This implies how much of the business was in buying and reselling ‘gently used’ closed, and how much was derived from new items.

Note: For Style Encore, the company provides the top quartile’s numbers, for which I decided to exclude it from the table.

Management reports that 42% of total Plato’s Closet stores reached or exceeded average sales and GPM. This may suggest the median is not very far from reported averages. Once Upon a Child, Play it Again Sports, and Music Go Round, had 41%, 37%, and 39%, of stores at-or-above reported averages.

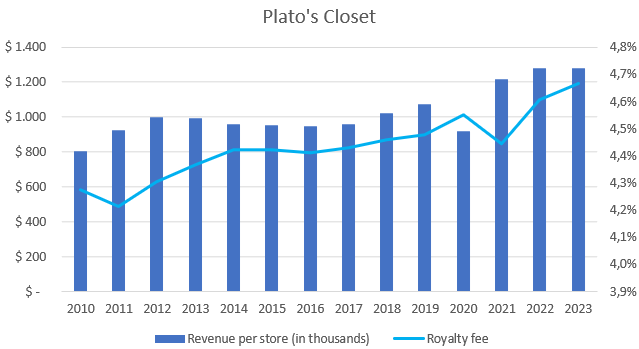

Plato’s closet has consistently gained share of Winmark’s number of stores and sales. Incidentally, average revenue per store had been flat at around $1 million dollars for numerous years, but after the pandemic, it got to $1.25 million per store. It is unclear to me whether this is sustainable or not. I’d be inclined to believe it is not, for a neighborhood approach imposes some sort of ceiling to revenue per store. Management has tried in the past opening bigger ones in more crowded areas but with poor results. Consequently, they focus on this low key strategy.

Winmark’s royalty fee has been around 4.3-4.7% since 2010, though it includes a component of the initial fee for opening, for which it’s not entirely accurate. It is worth pointing out that Winmark’s royalty is in the low end of what’s typically charged in a franchising business model.

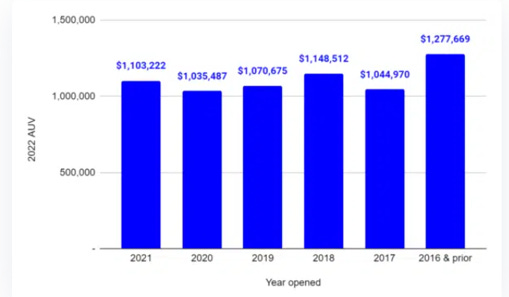

It is also fundamental to note how fast stores ramp up. The following chart shows how much revenue the average Plato’s Closet store did in 2022, and the year when they were opened. The average Plato’s Closet opened in 2021 had revenue of 1.1M dollars in 2022.

I cannot stress enough how fundamental this is for Winmark. The quicker stores get to their local addressable market, the better for everyone. Assuming 1.1M in revenue up from the second year and a 4.3% fee, Winmark would get 47.3k in high margin revenue per store every year for nine years, on average. Securing a franchisee would earn Winmark revenue around $450,000-$500,000 in the course of the decade.

Turning to another brand, I found interesting to observe that the number of Style Encore stores has stayed flat over the past 5 years, after rapidly ramping up. Notwithstanding this, revenue has continuously grown, exhibiting a 10.5% CAGR. Additionally, sales stayed flat in 2023, in spite of a 7% store count reduction.

Elements such as these point out the untapped revenue Winmark still has in already-built stores. Total gross sales for the Style Encore franchise have increased to 49 million dollars in 2023, implying an average revenue per store of 742,000, up 12% YoY. This makes me suspect that the closure of stores mostly consisted of those that were in the lower end of sales. The following chart addresses this as well as the implied royalty fee Winmark is charging, considering the opening fee as well.

Financials

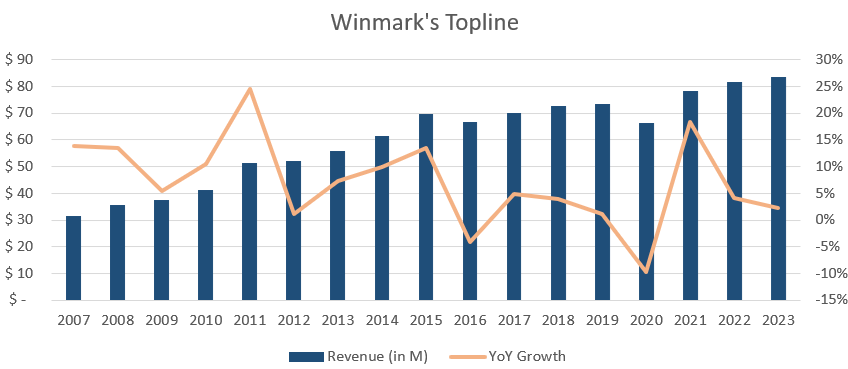

In 2023’s fiscal year, Winmark had 83 million dollars in revenue, growing 2% Yoy and exhibiting a 17yr CAGR of 6.7%. COVID-19 had a severe impact on 2020’s operations, but things seem to have normalized shortly thereafter.

Winmark has historically reported results via two business segments, franchising and leasing. The former encompasses:

Royalties, charged as a % of franchises’ gross sales.

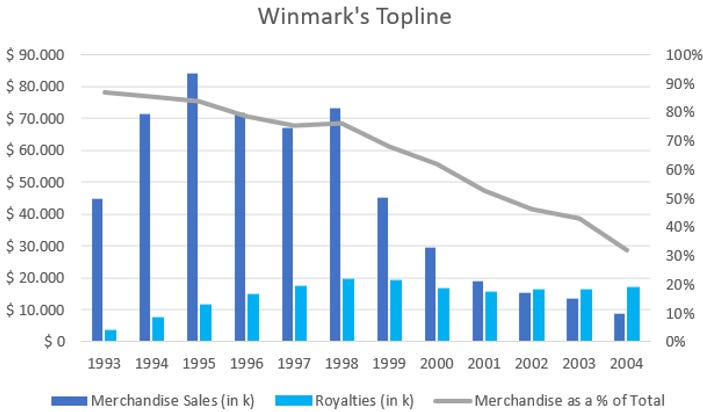

Merchandise sales, which include the sale of the PoS tech equipment to franchises and the sale of a limited amount of sporting goods to some franchises.

Franchises’ one-time fee, which is recognized over the estimated life of the franchise. Deferred franchise fees stood at 7.08M at the end of 2022.

Other revenue includes marketing (managing ads) and software license fees from the PoS.

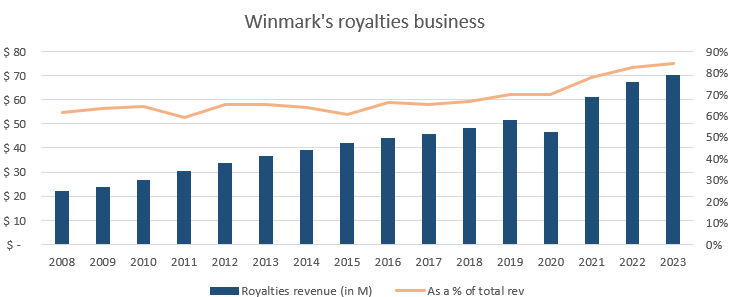

In the last fiscal year, royalties represented 84% of total sales, up from 66% in 2016. Leasing income, merchandise sales, franchise sales, and other, represented 6%, 6%, 2%, and 2%, of total revenue, respectively. The following chart depicts royalty income and the percentage of total revenue it represented throughout time. Over the past 15 years, royalty revenue has grown at at an 8.1% CAGR.

In a recent interview, Brett made clear that the company’s focus is in the resale business, in dedicating all efforts on scaling it and working with franchisees. Winmark has made several attempts to get into new business lines to re-deploy the cash generated by the franchising business. Nonetheless, Brett mentions they have always returned to the core of Winmark. Focus is now completely placed on resale.

Consequently, numerous decisions were made. The most relevant was to discontinue their 15-year old leasing business in 2021. Winmark used to destine a large part of the resale’s cash flow in running a middle-market and small-sized ticket equipment leasing enterprise.

John Morgan had co-founded a computer leasing business in the 80s, scaled it successfully, and sold it for $340 million in the 90s. He was the one leading the leasing operations at Winmark, which started right after Morgan’s non-compete agreement expired. A large part of the company’s generated cash was utilized for leasing equipment.

The leasing portfolio rapidly ramped up to 30-40 million dollars and stayed thereabout for over a decade. In 2023, the leasing portfolio’s value was reported at $100,000, down dramatically over the past couple of years.

Capital destined to this endeavor consumed the completeness of operating cash flow ever since 2004 up to 2018. Thereafter, cash flow has steadily risen and investing activities required 200-300 thousand dollars in 2022-23.

This has generated a notorious headwind to Winmark’s reported topline. Morgan took the leasing business to $21.5 million in revenue at its peak in 2015, representing almost a third of Winmark’s total sales. Thereafter, leasing income has declined to $4.7 million in 2023.

Winmark’s margins have dramatically expanded over the past 16 years as a byproduct of the franchising business gaining share of total sales. The company’s gross profit margin was 82% in 2006 and 94% in the last fiscal year. The operating margin expanded from 20% in 2006 to 64% as of 2023. Finally, Winmark’s net profit margin stood at 48% during 2023, up from 12% in 2006.

Capital Allocation Policy

Winmark runs a very profitable business. In the past, as exposed, most of the generated cash flow was reinvested. After the leasing business was discontinued, the company adopted a very simple capital allocation policy. Firstly, management does not intend to retain excess cash in the balance sheet. They continuously look for good opportunities to deploy cash flow. Ideally, cash would be re-deployed in the core resale operation, but Brett mentions that, historically, “there have been very limited opportunities to do so.”

If management does not find anything wise to do with capital, they look to return it to shareholders. Paying down debt is one of the ways for doing so. However, Brett finds debt to be locked at a very attractive yield and long maturity, for which he does not believe it worth to pay down.

Secondly, share repurchases are analyzed. The team is willing to buy back shares only at a price they consider appropriate. This simple approach has caused repurchases to be highly opportunistic. Over the past 20 years, Winmark repurchased shares every year except 2023, though repurchases are concentrated in specific quarters. In total, 4.3 million shares have been retired from the market for $350 million. As of Q1 2024, 3.48 million shares are outstanding plus another 160 thousand if we take option plans into consideration.

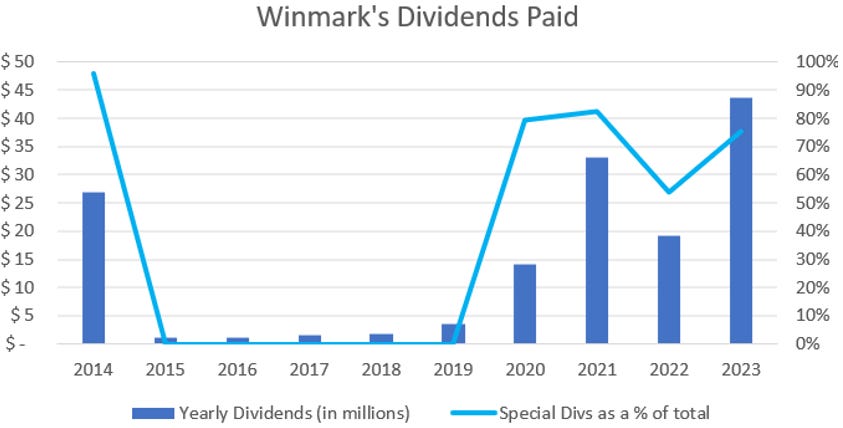

After deliberate meditation on the above avenues, management considers paying out dividends to shareholders. Winmark pays a small quarterly dividend. Management prefer it to stay at a low level, giving room for flexibility. If no investments are found and repurchases aren’t deemed as attractive, the team very willingly considers paying out excess cash in the form of a special dividend.

Over the past four years, which is when this policy seems to have gained traction, the majority of the dividends paid were via this mechanism. In total, since 2020, Winmark paid 8 dollars per share in quarterly dividends, and 22.9 dollars per share in special dividends.

Brett and Winmark’s Current Standing

In a recent interview, Brett mentioned that Winmark already has a model that works. It was built by a very capable man and it’s now up to management to simply follow the model. Incidentally, the same is requested to franchisees. Brett joined Winmark in 2002 as CFO and treasurer. He saw how the culture was shaped and how Morgan ran the business.

Brett highlights a fundamental idea in business. Winmark is in a position where it engages in win-win-win relationships. Everyone benefits from Winmark’s existence. Neighbors who need money and want to dispose of used items can go to a store and sell them. Last year, each store paid out $1,100 per day to neighbors, on average. Over the past 24 months, Winmark returned more than $1 billion in cash to communities wherein franchises operate.

Furthermore, Winmark is a leader in the circular economy. Most items that are purchased and sold through their franchise system would end up in landfills, damaging the environment. Since 2010, the company has found new use to 1.7 billion items. Brett mentioned why it is so important to only award franchises to skillful operators, which adds to this fundamental idea:

“And it's why it truly breaks my heart when a store closes. It's not because of the financial impact to us, we have 1,300 stores. Like one store closing from a financial standpoint, it's not going to impact us. But you have young families that now don't have access to our clothes, which is a problem. You have a couple going on a date that are teenagers for the first time that they want a new outfit and they can't go. Or young kids playing hockey that can't get those new skates anymore”

All of this is achieved by establishing win-win relationships with franchisees. The company trains them, provides them with the software to operate a store, and ensures their success. The fee Winmark charges seems low to me, when taking into consideration how much value it adds to franchisees. Nonetheless, Brett recognizes the importance of letting operators run the store independently, making the calls they think are best. It is their capital at the end of the day.

This converges into a web of decentralized operators, all of whom can utilize their creativity to sell more. Management is continuously in contact with all of them and leverages franchisees’ talent. If one of them comes up with a new clever mechanism or insight, the team pushes it to all stores. In fact, Brett said that “all the best ideas that have happened at the company and operational ideas and local store marketing and – they’ve all happened from franchisees.”

As of the most recent numbers, the secondhand apparel market was over $40 billion in the US, while resale accounted for $23 billion. Winmark’s share stands at 7% and is one of the biggest players in the resale market. Heffes interestingly mentioned that landfill still represents the largest competitor. Most people don’t know about resale options and don’t pursue that route.

Conclusively, Brett is fully aware of the low growth Winmark has experienced over the recent past. It is certainly his hope to grow faster. However, he highlights discipline as a vital trait in this business. They already have a model that works and that is improved every year. This focus on building a sustainable company has been crucial since Morgan took over.

The most important metric to look after, which Heffes suggests illustrates whether management is doing good job or not, is the renewal rate. A healthy renewal rate implies that franchisees are happy with their store. This is the keystone upon which all the ecosystem is built. Over the past five years, 622 out of 627 contracts were renewed.

Personal Commentary

I find that each company requires a different format for research. I’ll continue experimenting on this front. Hope you found the research useful.