The 20% discount for the research will expire in a week, you might want to secure that 80% price forever.

Visa reported results on October 24th after the market closed. This quarter represented the last one of their 2023 fiscal year. The company’s FY is one quarter ahead of the calendar. However, for there not to be any confusion, I’ll proceed as I usually do, labeling charts according to the calendar.

Net revenue during the third quarter was 8.6bn, increasing 10.6% on a yearly basis and 6% sequentially. The latter is a pattern that repeats itself throughout the company’s third quarters. Visa’s topline has, ever since its IPO, grown at a very healthy clip, now hovering in the low double-digit range. After demand’s fall off in 2020 and its rapid catch up, revenue growth has been slowly decelerating, though now stabilizing. The 4yr CAGR stands at 8.8%.

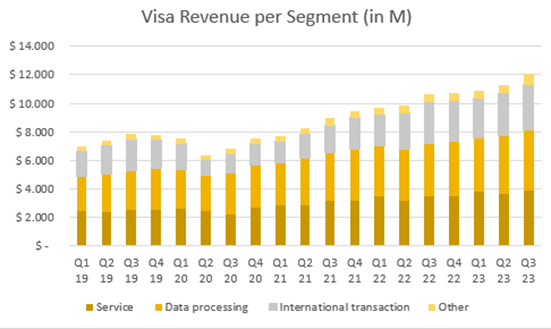

Prior turning into other financial statements or margins, I find it useful to break down Visa’s revenue. Management has been placing emphasis on diversifying their revenue streams for the past decade, which is starting to translate into results.

Service revenue consists of services provided to support clients’ usage of VisaNet (does not include processing). Service revenues were 3.87bn during the quarter, up 12% over the comparable period and 6% QoQ.

Data processing revenue includes processing clearings, settlements and authorizations, network access and value-added services. DPS sales amounted to 4.25bn, growing 13% year-over-year and 4% sequentially.

International transactions derive revenue from cross-border transactions and currency conversions. Revenue for this segment was 3.17bn, representing an increase of 10% YoY.

Other revenue encompasses license fees, other value-added services, account holder services and certifications. Other revenue was 744M during the quarter, up 35% YoY.

“Other revenues grew 35% led by pricing, consulting and marketing services” Conference Call

Each of these segments make up for 32%, 35%, 26% and 6% of total revenue, respectively.

The number Visa reports as the headline is ‘net revenues’, which are the above-shown sales minus the client incentives they offer. There is something here that has been somewhat worrying me.