Visa reported quarterly results last Tuesday, along with Google and Microsoft. The company’s fiscal year differs from the calendar’s, being one month in advance. To avoid confusion, I’ll utilize calendar quarters in charts and everything.

Net revenue for the quarter ended in June was 8.12bn, up 12% YoY and 1.7% sequentially. This puts Visa’s 4yr CAGR at 8.5%. Growth seems to be comfortably stabilizing in the low double-digits. VisaNet already processes over 15 trillion dollars in yearly volume, for which high growth rates should not be expected moving forward, or at least not from data processing services.

Visa has been placing emphasis on diversifying their revenue streams for the past decade, which is starting to strongly translate into results. Diving into each segment:

Services revenue consists of services provided to support client’s usage of VisaNet (does not include processing). Service revenues for the quarter were 3.66bn, increasing 15% YoY and declining 2% QoQ.

Data processing revenue includes processing clearings, settlements and authorizations, network access and value-added services. DPS rev was 4.1bn dollars, up 15% YoY and 7% sequentially.

Curiously, what appears to be the main contributor here is value-added services, which generated 1.8bn in revenue, up 19% in constant dollars.

International transactions derive revenue from cross-border transactions and currency conversion. Revenue for this segment was 2.9bn, growing 14% yearly and 6% sequentially.

Other revenue consists of license fees, other value-added services, account holder services and certifications. This segment generated 597M in revenue, up 15% YoY and 8% QoQ

They make up for 32%, 36%, 26% and 6% of total revenue, respectively.

The number Visa reports as the headline is ‘net revenues’, which are the above-shown sales minus the client incentives they offer. Client incentives for the quarter were 3.16bn dollars, accounting for 28% of total sales. Over the past 4 years, incentives as a percentage of total revenue have been steadily going upwards, starting at 21% in 2019.

Moving down the income statement, Visa did 6.46bn in gross profit, implying an 80% margin, very much in line with the historical. The company had 5.02bn in operating income, meaning the OPM stood at 62% for the quarter, which, unlike the previous margin, it is quite volatile from quarter to quarter. Nonetheless, it was up 500bps YoY and fell 500bps QoQ. Lastly, Visa reported earnings of 4.15bn, operating at a 51% net profit margin, also volatile, but in line with the average.

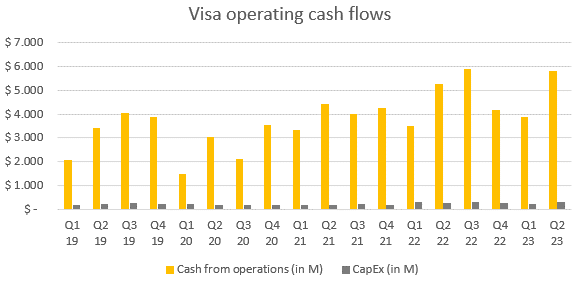

During the second quarter of 2023, Visa brought in 5.79bn in cash from operations, up 10% on a yearly basis. Sequential analyses make no sense in data with seasonal patterns. On the other hand, capital expenditure was 295M, leaving free cash flow at 5.5bn for the quarter. This is always a highlight from Visa’s results. It is truly a capital-light business.

Before going into details, the company returned a total of almost 4bn dollars to shareholders. 3bn were utilized in stock repurchases, meaning 13 million shares, or 0.6% of shares outstanding, were bought back. Average cost was $229 per share. At the same time, Visa distributed 937M in the form of dividends. The company has been continuously increasing the amount of cash it returns to shareholders.

Almost the entirety of Visa’s business model goes around VisaNet, their payments processing network. For this reason, probably the most important indicator of how well is the company doing is the volume VisaNet processes. During the last quarter, the network processed a total of 3.8tn, increasing 7% on a yearly basis and at the same rate sequentially. Last twelve months’ volume stands at 14.5tn. In absolute terms, it slightly outgrew Mastercard, who grew its volume by 209bn.

Another useful indicator to get a sense of the network’s health and usage is the number of transactions it processes. During the quarter, VisaNet processed a total of 54bn transactions, growing 10% yearly and 8% QoQ. This puts the network’s 4yr CAGR at 11%.

The final variable I like to analyse is the average transaction size VisaNet processes. The more intricated it becomes with the world’s economy, the more will VisaNet be used for mundane transactions, which tend to be smaller. For this reason, it would be objectively good to see a downtrend in this metric. This past quarter, average was at $70 per transaction, comfortably down yearly, and slightly sequentially.

Management commentary and outlook

In general, management pointed out the business resilience, a recurrent theme of Visa’s conference calls. Moreover, it is their belief that the continuously reported high growth rates are a good demonstration of the large opportunity that’s still out there. Moving on, there were three particular elements on which emphasis was placed.

Firstly, Visa’s brand is one of the values management takes good care of, knowing brand value differentiates a winner from a loser in the long term. They mentioned how crucial this results for acquiring merchants and keeping clients. This quarter, in the US, Visa retained their position of serving 8 of the top 10 credit unions and have recently renewed one of them. On merchants:

“our clients ask their customers which brand do you prefer? Would you spend more if we issued this brand or that brand? And our clients consistently tell us that consumers overwhelmingly prefer Visa.”

Secondly, a large part of the discussion was around Visa’s value-added services, a business that grew its revenue by 19%, generating 1.8bn during the quarter. Management mentioned their go-to-market approach as focused in deepening client penetration of existing products, expanding geographically and launching new solutions. What sets this business unit apart from the rest of Visa’s business is that it is mostly driven by the selling of a large number of smaller solutions to customers, rather than one big product.

“This quarter, we succeeded in selling more than 300 new issuing services, 600 new acceptance services and almost 500 new risk and identity services, in some cases, even within the same client. Our sales teams continue to work day in and day out with our clients to understand and resolve their pain points and realize new growth opportunities.”

Furthermore, Visa’s team seems to be very excited about this business unit’s opportunity:

“I mean the truth is we are at the beginning of the journey across all of our value-added services business. They all have enormous TAM. We all have – they have enormous runway in terms of the opportunity to continue to penetrate. We're in the very early innings of our penetration, and we don't see any of those businesses anywhere close to running out of runway anytime.

Lastly, Pismo acquisition was a matter management touched several times. I have not done research on Pismo, so I’ll leave you with what management said:

“We have signed a definitive agreement to acquire Pismo for $1 billion in cash. our recent announcement of our definitive agreement to acquire cloud-native issuer processing and core banking platform, Pismo. We believe that Pismo will allow us to strategically serve our clients through additional capabilities with core banking ledger and issuer processing through cloud-native APIs, additional geographies. What we're trying to do is serve our clients. I mean, that's what it all starts with. What our clients are looking for is they're looking for innovative processing solutions. They're increasingly looking for cloud-native API-based services. Processing is certainly one of the those”

Finally, two more topics of perceived secondary relevance. Visa’s team mentioned the growth potential Visa Direct currently has. Last quarter, transactions via Visa Direct grew 20% YoY to 1.8bn. Addressable market on Visa Direct seems very large. New flows capabilities like this one, management mentions, is what makes Visa distinct from other companies. Management is focused on expanding geographies and use cases to further solidify the product.

The other topic was client incentives, which have been trending upwards as a percentage of total revenue for a while now. When the team was asked about why were incentives tending towards the high-end of guidance, the CFO answered the following:

“In general, on incentives, they were in line with what we expected. So, there were no surprises there. And incentives, everybody focuses on the percentage. If you look at what really counts, which is net revenue growth, we had healthy net revenue growth in the quarter”

For the fourth quarter, Visa expects a net revenue growth of around 10% and incentives as a percentage of gross revenues between 27.5% and 28.5%

My take

Visa’s quarter was solid, as usual. What I find extremely positive is management’s emphasis on expanding Visa’s optionality and the way they are doing it. Value-added services are continuously grabbing share of total sales, outgrowing the network’s income and, given how diversified in nature these are, it diminishes the hit of a potential impact on VisaNet. Moreover, it is good to see Visa utilizing a very successful playbook: going after customer’s pain points and creating or buying a solution for it. They mentioned this with Pismo and with many of the added-value services.

The only thing that it is somewhat worrisome is the trend client incentives has. I did not like the CFO’s response to the question. It feels he simply avoided the issue. The trend in incentives is something that has been happening to Mastercard as well, if I’m not mistaken, so it could be an industry concern. Leaving this aside, the quarter, guidance and future prospects are and look good.

Personal commentary

This is the fifth earnings we covered. The only remaining are Texas Instruments’, which should be published on Saturday, Zoetis and Mercado Libre. Hope you enjoyed the article and that are finding some value in these reviews.

Disclosure: This is not financial advice.