Visa reported quarterly results last week. The company has a fiscal year that is one quarter ahead of the calendar, which is why they finished the 2Q. For ease of reading and analysis, I’ll compute charts as if Visa followed the calendar year.

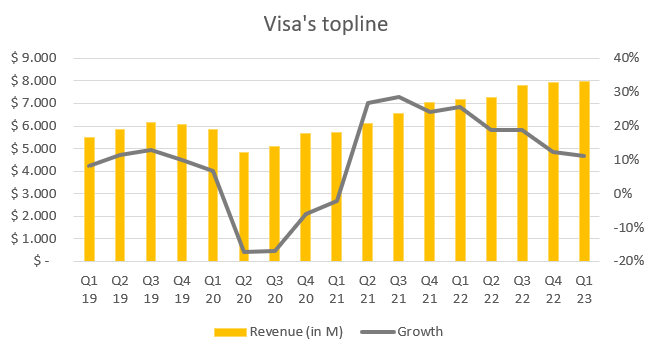

During the first quarter of 2023, Visa generated 7.98bn in revenue, growing it by 11.1% on a yearly basis and slightly sequentially. The latter is of no concern, given the fact that, generally, Visa’s fourth quarters are the strongest while the first ones are the weakest. Growth is decelerating though, quarter after quarter, but it is still showing some sort of resilience, being at double digits.

Visa is one of the companies with the best margins out there and they have been stable at sky-high levels for the past decade and a half. Gross profit was 6.29bn for the quarter, comfortably up yearly. Its margin was 78.8%, down from 80.3% last year. Visa’s operating income was 5.33bn, with its margin at 66.8%, flat YoY. Lastly, the company operated at a 53.3% net profit margin, meaning net income generated was 4.2bn.

Curiously, the net profit margin expanded on a yearly and sequential basis. The image below is from Visa’s income statements for the quarter. It is clearly illustrated the reasons behind the margin expansion were lower non-operating expenses and a slightly lower income tax provision.

Turning to the cash flow statements, Visa brought in 3.86bn cash from operating activities. Again, there is some seasonality here and Q2/3 seem more as outliers than other thing. Nevertheless, operating cash flow seems to be somewhat stuck in these levels. Moving forward, it would be expected for this metric to return to an uptrend, in line with Visa’s whole business. From an outflow standpoint, Visa had 210M in capital expenditures, illustrating how capital-light of a business this is. Both variables leave free cash flow at 3.65bn for the quarter, up from 3.22bn in the comparable.

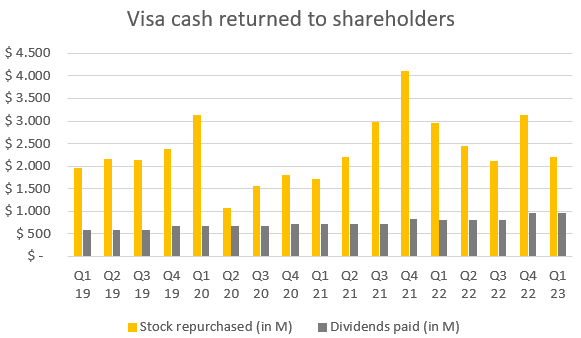

In the first quarter of 2023, Visa returned a total of 3.3bn to shareholders. Stock repurchases for the period accounted 2.19bn, very much in line with previous ones. As of March 31, the company’s repurchase program had remaining authorized funds for 11.9bn, out of the 12bn authorized in October of last year. Furthermore, Visa distributed 941M in dividends to shareholders.

Total transaction volume measures the aggregated dollars processed through VisaNet. I mention this because it is very common to confuse it with TPV. Visa’s transaction volume for the quarter was 3.55tn, up almost 5% YoY.

On the other hand, the number of processed transactions is still growing smoothly, being 50bn for the quarter and up 12% YoY. Interesting to notice some sort of rebound in both metrics.

Upon both charts, I went up to draw the following, which intends to show how much money is being transacted per transaction, on average. The calculation is very simple, dividing total transaction volume by the number of processed transactions, yet the resulting chart is very telling. Over the past 4 years, the average transaction went from $82 to $71 or so.

Management commentary and outlook

Ryan first started by pointing out Visa’s strength, the immense opportunity ahead and how is Visa approaching it. He explained how the consumer payments flywheel works and how they benefit:

Grow credentials, more buyers on the network

Grow acceptance rate, more sellers on the network

Drive engagement, more transactions

Visa got to grow credentials 7% YoY. Furthermore, there are now more than 6bn tokenized credentials, up nearly 90%. On the sellers’ side, merchants on the network are over 100M. And, on the third step, Tap to Pay continues to drive engagement up. Globally, 74% of all face-to face transactions are now taps and, in the US, 34% of them are taps, up 1000bps YoY.

A lot of contracts were mentioned, both renewals and new partnerships. Additionally, Visa is rolling out in Japan, along SMBC, a product that acts as a flexible credential. It can be utilized as a debit, credit or prepaid card. At the same time, management mentions Visa is growing at rapid and healthy levels in regions like Latin America, where they are getting partner renewals with banks like Itaú (largest in Brazil) and many other deals with large organizations.

Moving on to one of the core things Visa focus on (remember the research article), new flows. Earlier this year, Visa announced Visa+ and management expanded on what this is and how it can enhance new ways for money to flow:

“This new network allows users to send and receive payments among different P2P apps through a personalized payment address, a Visa+ pay name. This enables P2P payments from one app directly to another app as well as gig, creator and marketplace payouts. This can be done through an app, a neobank or a wallet. We're connecting endpoints and form factors and enabling interoperability, our network-of-network strategy at work. We're launching pilots with several partners including Venmo, PayPal, TabaPay and Western Union, with more to come soon.”

The third engine that is fueling Visa’s growth is value-added services, which grew 20% YoY in cc, getting to 1.7bn. Management says their current portfolio of offerings is impressive and has a lot of momentum, exemplifying with 3 of them:

Visa Acceptance Cloud, which moves embedded payment processing from individual devices to the cloud. First National Bank in South Africa is one of the first customers this solution has.

Managed Services implies the company to send employees to others’ organizations to perform concrete projects. Managed services grew twice as fast as advisory services

Risk-as-a-Service, a fraud detection solution, is getting traction. Since launching 6 months ago, nearly a dozen direct clients were added.

Finally, for the third quarter’s outlook, management referred to a few things. Firstly, they said growth on domestic payments volume has been stable around the globe. Secondly, they saw a down tick in domestic volumes for the US and an unchanged trajectory for international. In conclusion, they expect revenue to grow in the low-double digits and client incentives to have a step up from this Q.

My Take

Visa is a wonderful company and has its mission clear. The 3 growth engines are correctly identified and the business has been gaining momentum in the three of them, with innovation across the board. Furthermore, the opportunity ahead is still immense, management allocates capital in a disciplined manner, it’s a shareholder-oriented company and margins/financials are almost never compromised. One other thing I’d like to remark as very positive is that the company continues to work towards their ‘network of networks’ objective. I think Visa+ contributes to this end and is a spectacular initiative.

Lastly, a major part of what composes Visa’s thesis is the fact of them being at this great spot in which, by including people in the financial system, they get business. You can see this is trending in the right direction in the chart ‘average transaction size', which shows Visa is processing more and more mundane transactions. The good thing about this is that it strongly strengthens Visa’s moat. Visa is already so intricated with the global economy that a displacement seems like a virtual implausibility. Continuing in this path should only help grow its moat.

Love this company! The margin still amazed me every quarter. Great read, thanks!