Today we’ll be reviewing in depth the second part of Warren Buffet’s strategy, not overpaying.

Factors Determining Investment Returns

As we discussed, your investment returns depend upon two things:

What you buy.

What price you paid for it.

These returns will be measured in the following way: (Price1 – Price0)/Price0

Where Price1 will be the future price of the stock, and Price0 will be the price you paid. Once seeing the actual formula to determine one’s returns, you can easily arrive to the conclusion that the price you pay for something is extremely important since it’s literally what will determine how much you make on a certain investment.

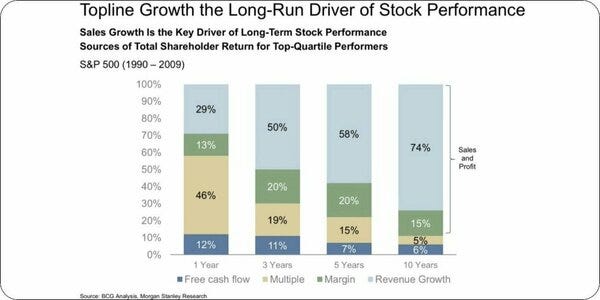

The second pillar that affects your returns (What you buy) will be so in the form of how the stock you bought will tend to behave in the future. In the third article we learned that one of the drivers of future stock performance (the main one) is the earnings that the underlying business has.

“The future trajectory of the underlying business will be the north of your stock’s price.”

Sales and Price to Sales

We described in the past articles, how can a stock’s value/price be measured, theoretically. The way you measure it is by discounting the future cash flows the company will produce on a per share basis. But, to keep it simple for now, let’s just use two variables: The price to sales ratio and the actual sales the company has.

Sales are the total money a company generates, without subtracting any costs. Price to sales is how much is the business worth (market cap) in relation to the sales it produces. For example, a company that has 1 billion in sales/revenue and a market cap of 10billion will be implicitly trading at a PS of 10.

The price to sales a stock trade’s at, reflects or embeds the potential of future growth the business has. Investor’s will be willing to pay a higher multiple for a company growing 50% than for a company growing 5% on a yearly basis. Because, as we said, the business growth (when translated to earnings) drives the stock price in the long run.

As time goes by and a business continues to grow, growth tends to normalize and correlates in a more direct way to economy growth, which means that it eventually slows down. It becomes so big that growing at a fast pace gets constantly harder. This means that, when the business growth slows down, people will not be willing to pay the multiple (PS) they previously did because the future prospects don’t look as bright as before, since that growth is behind.

Example

Now let’s use an actual and recent example with the company Snowflake (NYSE:SNOW). Of course, Ceteris Paribus.

In2021, the company produced 600M in revenue and was trading at 120 LTM sales. So, the company had a market cap of about 72 billion dollars. Now let’s suppose the company manages to grow sales at a 35% compound annual growth rate for the next decade (which is A LOT) and we bought at that price in 2021.

You are now standing in 2031, you managed to buy a company which grew 20X revenue! You would think that you made an incredible investment, well you have not. The SPX index, measured by the ETF SPY, managed to grow at its historical rate (9%) and actually earned more money.

There relies the importance of not overpaying for a stock even if the company has an absurdly bright future like Snowflake did in 2021.

“The outcome of buying the right company at the wrong price will be a poor investment decision.”