Earlier this year, I published an article laying out my thoughts and concerns about DCF models. My sense was that their true applicability is close to nulity. The reasoning behind was the sensitivity of these models, the necessity of knowing 100% of companies, which is a rare knowledge DCF-makers have, and some other things. Nonetheless, to each their own and, if one’s strategy works, fantastic.

Anyhow, this type of ignorance can only be addressed by learning. Last Sunday, I finished The Innovator’s Dilemma and, on Monday, started reading all of Michael Mauboussin’s research articles. Michael is, in my opinion, one of the best researchers and communicators in the capital markets. He dissects specific items like ROIC, WACC, employee stock options, valuation, market behavior and biases, in a way that’s very much unique. Today’s article is about something he wrote in 1998.

Competitive Advantage Period, the neglected value driver

During the 80s, the US stock market vastly outperformed its historical returns. In the early 90s, a study was published that attempted to explain where did this excess of returns came from. Interestingly, after carefully considering M&A’s, EPS, margins, etc, an extremely high 38% of returns remained unexplained (statistically I assume). The problem is that the researchers omitted the CAP, which, in Michael’s words:

“It remains the most neglected component of valuation”

There are two reasons why he believes the CAP is often disregarded:

Most market participants aim to value companies on an accounting basis, generally utilizing the PE multiple and the expected earnings growth (already wrong since the market values more cash flows). Therefore, the competitive advantage period is rarely considered, even when the market very clearly recognizes mid to long-term cash flows.

Businesses themselves generally do financial planning for the subsequent 3-5 years, which is what they communicate to investors. However, 3-5 years substantially differs from the companies’ CAP in almost all cases.

“The competitive advantage period is the time which a company is expected to generate returns on incremental investment that exceed its cost of capital”. In simple terms, it’s the life expectancy of the company’s MOAT, the durability it may have. The term was first articulated by M&M in 1961.

A company’s competitive advantage period is a fundamental input to valuation as it allows to better infer what are the market’s expectations for that business. It is determined by multiple factors, both company-specific and external, but Michael’s team believes there are three of them that are core:

Return on invested capital. Within its industry, the companies that enjoy the highest returns on capital are generally the best positioned ones from a competitive standpoint.

The rate of industry change. How fast an industry is disrupted, on average, highly determines how are these extra returns valued by the market.

Barriers to entry. The difficulties newcomers face when trying to compete or disrupt an established player allow for better predictability of the business’ cashflows.

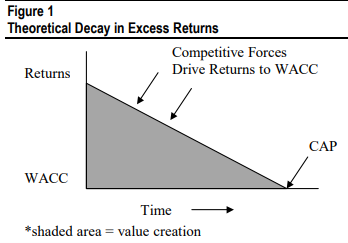

Theory versus reality

The economic theory for capitalism lays on the foundation that profits attract competitors. When a company enjoys returns on capital that are above its cost of capital, generates benefits, other people will see this and enter the industry.

As time goes by and as long as companies enjoy above-average returns on capital, competitors will keep coming. These companies with generic products have to compete on prices, which, eventually, drives companies’ returns to their cost of capital. Theoretically, it would look something like this:

However, that is not what happens in reality, as per usual. Data suggests that returns on capital do not diminish linearly as competition arrives. I believe this is due to Clayton’s theory about disruption. Established players are the most-likely ones to perform sustaining innovations. New players cannot displace them by offering the same as them, only a little better. Nevertheless, firms that create disruptive products can displace established firms as they improve the disruptive product.

This occurs in different market segments, innovators generally coming from the bottom-end of the market. Eventually, and paradoxically suddenly, the disruptive product gets better than the established one in all dimensions. The big firm gets displaced and its high returns are cut off.

Practical implications

Acknowledging that there is a theoretical end to a company’s superior performance drastically modifies the way we value it and, in parallel, the way we perceive the market to value it. Therefore, it looks as if by utilizing the CAP, we could get somewhere closer to an intrinsic value. Otherwise, DCF models generally include terminal values that account for 60-75% (!!) of a business’ intrinsic value.

“We find that the discounted cash flow analysis done by most analysts and strategic planners has a forecast period, or CAP, that is too short and a terminal value that incorporates too much of the overall value. As a result, the calculation of value becomes highly sensitive to the implicit growth assumptions beyond the forecast horizon that are embedded in the terminal value”

The method with which this can be employed is greatly articulated in the article (Competitive Advantage Period “CAP”, The Neglected Value Driver”). I’ll avoid getting into the math here as there is one more short insight I’d like to share.

Potential utility

This new equation defines a period X after which the company theoretically gets to having lower returns than its cost of capital. This of course is one’s assumption and it could well be the case that it’s wrong. Nevertheless, the business’ future “fair returns” will be in accordance to the stipulated CAP. If the company’s competitive advantage period remains constant over time, or even extends, an investor should be able to get these excess returns because of this unpriced CAP extension.

Personal commentary

I went over 10 of his research articles already, fascinating but tough read. The conclusion is that, during the 80s, the S&P’s CAP increased. Hope you enjoyed the article, I should be coming with many of these things in the next couple of Sundays!

Feel free to contact me regarding doubts/questions/a conversation.

Email: giulianomana@0to1stockmarket.com

If you haven’t yet, check out the podcast. I think it’s finally taking a good route:

Great article! I think a DCF serves it purpose because it makes your reasoning in valuation explicit. However, the final result, the calculated value is less usable. In the end, the goal is to find something that is heavily undervalued without knowing exactly by how much. To be directionally right.

Just a warning, soon after you will despise everything that involves investment banking, sell-side equity research, consulting etc.