By no means I consider myself an expert in the company like Leandro, Niklas or other very bright people on Fintwit. It is though very important for me to review this earning results in the best of detail and to bring the most facts to this article. In case you are not very familiar with the company, here’s a short overview of it:

Texas Instruments presented its 4th quarter results on the 24th of January, after the market closed.

Revenue came in at 4.67bn, down 3.4% YoY. I generally do not give much consideration to guidance, but since management is very keen on providing it, revenue was at almost the highest end of the range they provided on the third quarter:

"TI's fourth quarter outlook is for revenue in the range of $4.40 billion to $4.80 billion and earnings per share between $1.83 and $2.11.”

As a whole, Texas Instruments did 3.08bn in gross profit, down from 3.35bn in the comparable quarter. Gross profit margin was at 64%, declining 500bps YoY. The company’s overall operating profit was 2.17bn, down YoY and with its margin being at 46.4%. Now diving a bit into the segments’ financials.

Analog revenue for the quarter was 3.55bn, down 5% YoY and making its last 5-year compounded annual growth rate 7%. This segment has grown its revenue share of the business from 67.8% to 76.4% over the same timeframe. The operating profit it contributed to the overall results was of 1.79bn, which’s margin decreased 570bps YoY to 50.3%; and, represented 82.7% of the total operating profit generated, up from 76.2% in 2017.

Embedded Processing revenue came in at 0.83bn, up 10% YoY and making its last 5-year CAGR -1.4%. The segment’s share of the business decreased in the selected timeframe, from 23.9% in 2017 to 17.8% as of today. Embedded did 0.29bn in operating profit with its margin standing at 34.9%, up slightly over the last 5yr, but falling 300bps QoQ.

The last segment in which Texas Instruments reports its revenue is ‘other’. In the last quarter, ‘Other’ did 275M in revenue, down 11% YoY and 85M in operating profit. This segment’s revenue decreased in the past 5yr, but its operating profit grew from 68M in 2017.

Getting to the bottom line of the income statement, TI had 1.96bn in net income, down 8% from 2.13bn last year. With its decline, the net margin dropped 200bps YoY to 42%.

Cash Generation

Cash flow from operations have trended upwards for the past 3 years until this last downtick, where it decreased around 13%.

The image above corresponds to the firm’s cash flow statement. We can notice the most relevant changes (in absolute and relative terms) were in deferred taxes and inventories. Regarding inventory, management stated the following on the third quarter and something really similar but more extensive in this one:

“The product life cycles of the parts is decades in many times. The products themselves last 10 years in inventory, most of them. So the risk of obsolescence for the inventory is very, very low. The potential upside of having that inventory ready is very high. So that's why we prefer to have more, than less, inventory”

First outtake, a decrease in cash flow from operating activities is not necessarily negative, which it looks to be the case here. If adjusted by the extra inventory purchased, CFO would have been flat YoY. In the same line, management stated they could grow an additional 1-2bn without hurting the firm.

The remaining factor regarding the money TI produces on an operating basis is Capital Expenditures. The business has been going through an investment cycle since 2021 and it is expected to continue for the next year or two. In consequence, CapEx has increased abruptly, making free cash flow much lower than before and hurting its margin.

Bringing some extracts from the article I wrote a few months ago:

“We have 300mm capacity coming online in 2022-23”

“We have a 300mm roadmap to support growth from 2025-35”

“Customers are excited that capacity investments in (…) will support their growth in the decades ahead”

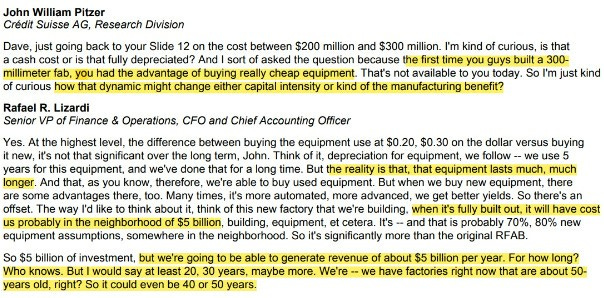

Lastly, as a reminder of how much sense do these investments make:

Cash Return

TI concludes their quarterly report by inputting a table which shows how much money did they return to shareholders in the form of dividends and stock repurchases. I thought it would be insightful to go back a few years, quarter by quarter.

Dividend payouts have been consistently raising and that trend has been upwards for a very long time. On the other hand, stock repurchases vary severely QoQ and period to period. Texas Instruments’ management team is often regarded as one of the best capital allocators out there and one of the most disciplined. The following chart showcases which are the periods when stock repurchases get higher.

When the stock market goes nuts to the downside, TI’s management is always ready to deploy capital. But it is more important to observe how they do not spend money on stock repurchase in clear upward trends, when it’s not needed, like in 2020/21.

One last thing on capital management, noticed by Leandro:

“Our balance sheet remains strong with $9.1 billion of cash and short-term investments at the end of the fourth quarter. In the quarter we issued $800 million in debt. Total debt outstanding was $8.8 billion with a weighted average coupon of 2.93%”

In this environment, having the coupon at such a low rate seems product of great decision making when issuing debt.

Management Commentary

Industrial + Automotive revenue made up 65% of total revenue, up 300bps YoY. Industrial and auto customers are increasingly turning to analog and embedded technologies, which is the main factor driving both customer segments to outgrow the others.

“Gross profit decreased primarily due to lower revenue, increased capital expenditures and the transition of LFAB-related charges to cost of revenue”

Guidance: “Turning to our outlook for the first quarter, we expect TI revenue in the range of $4.17 billion to $4.53 billion and earnings per share to be in the range of $1.64 to $1.90.”

End market demand was weaker in the 4th quarter and it is expected to continue in the 1st, with the exception of automotive, which remains resilient.

“But I do want to say, just as I said 90 days ago, that since we talked about this last year, our confidence surrounding our long-term growth prospects have only grown” (…) “that higher confidence comes from the higher semiconductor content growth that we're seeing, particularly in industrial and automotive, and the fact that those two markets now make up two-thirds of our revenue, so just as that structurally grows faster than the rest of the market, we're convinced more than ever that, that will continue to drive our top line and also the products that we have inside of those markets”

“We just continue to price aggressively in the marketplace, but that pricing isn't the reason why customers choose our products”

“When we think about the market opportunity for Embedded and Analog, we think that both of those markets have about the same growth opportunities”(…) “longer term, we believe that they can grow at the same rates.”

My Take

Intel presented results yesterday (I haven’t had the chance to review them in detail), but they looked horrible. ASML presented results on Wednesday’s morning and were strong with very good future prospects. Only two semiconductor companies reported results so an industry conclusion seems heavily skewed.

However, the semiconductor industry has been on a down cycle for the past few quarters and it got to show with almost all of them (not so much in ASML’s performance which is not surprising). In 2022, Texas Instruments’ revenue grew 9%, GPM increased 100bps to 68.7% and the net margin increased in the same proportion to 43.7%. Free cash flow has been affected by the investment cycle, making its margin drop 500bps to 29.6%.

In conclusion, Texas Instruments got to expand its margins and preserved a healthy 30% FCF margin while an ongoing CapEx investment is taking place. In perspective, it doesn’t seem extremely bad considering how much demand and profitability other companies have lost. Management guided for revenue declining by around 12% at the midpoint of the range, but they remain with a very positive outlook for the years to come. They also stated their investment focuses are working, as their results in automotive and industrials show. It is expected the demand for Analog and Embedded Processing coming from these sector outgrow the rest. This focus they are making in both of them should continue fueling Texas Instruments revenue and increase these segment’s clients dependency on them.

In my opinion, Texas Instruments is a business from which an investor should expect slow, but steady growth. It is its scarce of fundamental volatility what makes it a potential anchor in one’s portfolio and it looks like it’s accomplishing the objective.

Personal Commentary

I did not discuss in more detail how Analog and Embedded processing looks moving forward because of my ignorance. Getting to know every single technicality from every single company is a tough task. I feel as my base knowledge is continuously improving, but I will not express detailed opinions on matters I still do not know fully. There would be no value for you in me doing so. Anyway, hoped you enjoy the article and feel free to subscribe below!

Disclaimer: This is not financial advice

Awesome. Love this one!