Texas Instruments reported results last week, the same day as Google, Visa, and Microsoft, all of whom foreshadowed TI a bit. The company generated 4.53bn dollars in revenue, declining 13% year-over-year, but increasing 3% sequentially. First sequential increase in a while. The semiconductor industry has been in a down cycle for some quarters and TI does not get exempted from that. Curiously, yearly growth rate did not bottom out last quarter as growth rate declined once more.

During the second quarter of 2023, TI did 2.9bn in gross profit, down from 3.62bn last year. This means it operated at a 64% gross profit margin, which was down 540bps YoY and 120bps QoQ. Operating income was 1.97bn for the quarter, implying a margin of 43.5%. The latter declined 870bps YoY and slightly sequentially. Lastly, Texas Instruments reported a net income of 1.7bn with the net profit margin being at 38%, down 600bps YoY and 100bps QoQ.

Important detail on gross margins:

“On a year-on-year basis -- I know you asked sequentially, but just a reminder -- on a year-on-year basis, keep in mind that last year we had the Lehi acquisition fab cost in restructuring, and now it is in COR, in cost of revenue, as of December of last year is when it moved.”

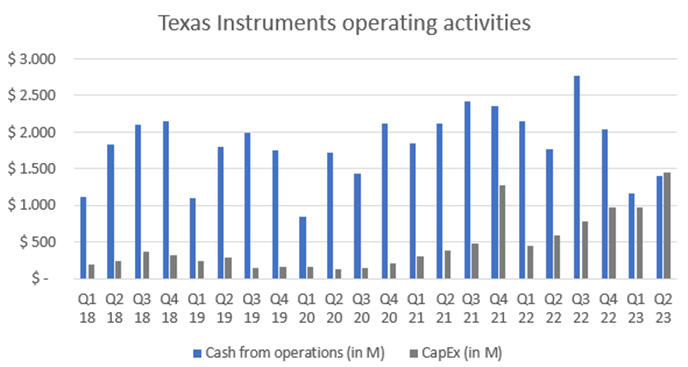

Moving into the cash flow statement, TI’s operations generated 1.39bn in cash, down 21% YoY. Moreover, the company had capital expenditures of 1.44bn dollars, the maximum amount they’ve invested in a particular quarter in a while. This leaves free cash flow at negative 47M for the quarter. The last time TI posted negative free cash flow was in the first quarter of 2004.

An important factor that caused this to happen is inventories. Management has been calling for an increase in inventories and have been doing so for the past couple of quarters. This past one, inventories signified a 441M outflow for TI, compared to a 139M in the comparable quarter.

Before diving into details, one last general thing Texas Instruments is widely known for, the value returned to shareholders. This past quarter, TI bought back the equivalent of 79M dollars in shares. Management always emphasizes their approach of only deploying capital when the stock is below intrinsic value. At the same time, they paid 1.125bn to shareholders in the form of dividends, a number that has been steadily increasing.

Texas Instruments operates under two major segments and a minor one. The first of them consists of manufacturing and selling analog chips. This business unit generated 3.27bn in revenue, down almost 18% year over year and flat sequentially. Moreover, operating income was 1.46bn for the segment, implying a 44.6% margin. The latter contracted 1120bps yearly and 330bps QoQ.

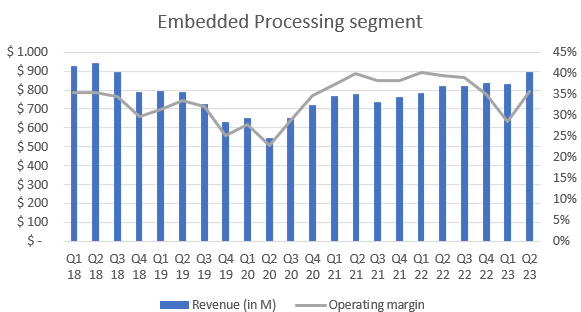

The second major segment is embedded processing, which, during the quarter, curiously grew its revenue by 9% YoY. It generated 894M dollars and 318M in operating income. The operating margin stood at 35.6%, but it’s quite volatile. It was down severely YoY and up dramatically QoQ as well.

Management commentary and outlook

Management mentioned a weakness continuation in all end markets, except automotive, which has been showing resilience this down cycle. Their guidance reflects some more of that in the future. Customers are continuing to work down inventories to get more in line with their demand and, until that ends, even less demand will there be for TI’s products. Something very similar was said by ASML’s team.

The concern most analysts shared was about Texas Instruments’ strategy, and almost the entirety of the conference call was around it. Since there hasn’t been much results from the company’s investments, analysts asked if it wouldn’t be time to reconsider the efforts. At the same time, capital expenditures continue to be high (in line with what they had guided), margins continue to contract, and management keeps increasing inventories, which again affects the cash from operations.

“at what point will TI say that something needs to change in the strategy to help close the gap on the growth side and to help free cash flow margins get back to the trend line?” Analyst

One of the things TI’s team is well-known for is their long-term thinking in nature. On the strategy, they pointed out, firstly, that it’s something they have guided for a long time. More importantly, the team recurrently reminds investors that their investments are destined to building new fabs. Ultimately, these investments are what will allow the business to grow revenues for the coming decades and produce items at lower costs. That’s where their focus is on. Revenue and margins fluctuations are something that, even though relevant, cloud the big picture.

“We're excited to making those investments regardless of the short-term fluctuations of revenue.”

Finally, management’s strategy with respect to inventories has been a matter of discussion for the past couple of quarters as well. “Inventory dollars were up $441 million from the prior quarter to $3.7 billion, and days were 207, up 12 days sequentially”. As usual, the team reminded investors that inventory is something they utilize to protect themselves from expected demand. If demand suddenly skyrockets and inventories are not built accordingly, TI’s reputation suffers. Customers, management mentions, are seeing all of these decisions with a good eye. Furthermore, they reminded investors the really low risk of obsolescence inventory really has.

” the inventory itself lasts years, in fact, up to 10 years on the shelf, but the product life cycles are very long with our customers, and we have, in many cases, tens or dozens of customers that buy the product. So the risk of obsolescence is very low in the dollar”

Some final takeways from the call:

“In the big scheme of things, our goal here is to support revenue growth..those investments will allow us to produce products at significantly lower cost when -- to service demand. So customers can see the investments that we're making. Not only with that, the other systems that we've got to make it easier to do business with us, combined with the inventory we're putting in place to support their growth, and customer reaction is extremely positive to that.”

For the third quarter, TI expects revenue to be between 4.36bn and 4.74bn. Earnings per share are expected in the range of 1.68-1.92.

My take

Investors seem to be getting nervous and analysts are starting to really manifest doubts towards Texas Instruments team. Management stood strong, answered and repeated without losing patience, and continued to give their honest view. The quarter was of course a disaster from a financial and isolated standpoint. But there are too many grays in business and investing. The fact that Texas Instruments is operating in a down cycle and making heavy investments for the long-term has depressed margins and cash from operations.

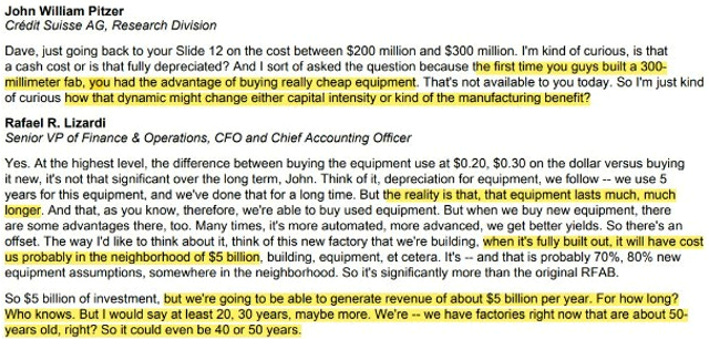

Interestingly to me, people very often label themselves as long-term investors, but, when management truly operates for the long term, they get angry. It is something I’ve also been witnessing with Tesla. Both management teams are doing what it’s best for the business in the long run, where the true yield is. What differentiates TI’s team from Tesla’s, in this regard, is that they’ve been calling for these decisions for a very long time. That’s why they mention in all conference call these things were not unexpected. The following image is from their Capital Management Day held in February and illustrates this point:

The semiconductor industry has immense secular tailwinds backing up its future growth. However, the cyclicality it has can make one forget about its long-term and healthy trend. The important thing is for a company’s management to not focus on these fluctuations, but to keep their eye on the long run. If they don’t, not only will they suffer during the down cycle, but, after it ends, competition will eat away their market share. Here’s the trend Texas Instruments is optimizing for:

That is why they are building up inventories and expanding capacity while geographically diversifying it at the same time. All these investments should help TI stay in market and grab more share, which management is confident they will. The fabs they are building will support revenue growth for a long time and have absurd return on investments because of their long-lasting nature.

Investments seems very much appropriate when put into perspective how much profit will they provide and for how long.

Personal commentary

The only reviews that are pending are Mercado Libre’s, who reported results this past Wednesday and Zoetis, that reports on Tuesday. I’ll be covering both next week. Finally, Zoetis second part of the research has been written for a while. I’ll be publishing it once earnings reviews stop to try not overwhelm. Hope you enjoyed the article!

Disclosure: This is not financial advice.

They are on my watchlist for a while now and I'm trying to wrap my head around all the Capex and margin contractions. This review help me with that thanks! I Will go and listen to the call myself to get a better understanding. Cheers!