Texas Instruments reported results on April 23rd after the market closed. The company has been severely struggling for the past couple of years as the semiconductor industry was immersed in a down cycle. In this article, I’ll go over TI’s quarterly performance from a financial standpoint, cover management’s commentary and outlook. At the end, I’ll share my take on the quarter and what I’m doing portfolio-wise.

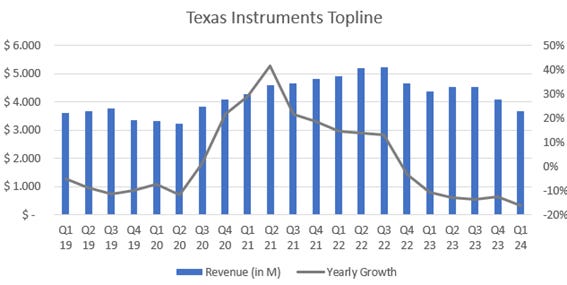

Texas Instruments had revenues of 3.66 billion dollars during the first quarter of 2024, down 16% on a yearly basis and over 10% sequentially. Revenue declined across all end markets and segments, wherein I’ll dive after the general overview. This is the sixth quarter in a row where revenue declines YoY.

Margins continued to decline. Gross profit in the quarter was 2.09bn dollars, down from last year’s 2.86bn. The gross profit margin contracted by 815bps YoY, being at 57% this Q. TI reported operating income of 1.28bn, with a margin of 35.1%, which fell 900bps. Lastly, the company generated 1.1bn in net income, implying a net profit margin of 30.1%.

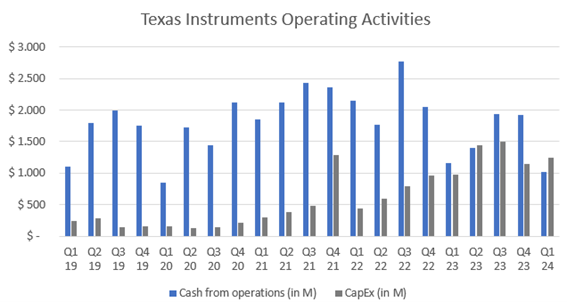

Free cash flow has experienced further trouble due to TI’s ongoing CapEx. During the quarter, the company reported 1.01bn in cash from operating activities, down from 1.16bn last year. Capital expenditures were 1.24bn, somewhat in line with management’s guidance of 5bn per year.