Before going into the article, keep in mind that, in the following weeks I’ll be covering Visa, Google, Microsoft, Texas Instruments, Mercado Libre and Zoetis. If you’d like to receive the earnings review, you can subscribe below.

Overall Financial Analysis

Tesla reported results last Wednesday after the market closed. The company generated 23.35bn in revenue, growing 8.8% on a yearly basis, drastically decelerating from the previous two quarters. Even though it looks concerning on some level, Tesla’s 4yr CAGR stands at 38% and, its 8yr CAGR, at 49%.

As a side note, Tesla is a business that’s near 100bn in annual revenue. Realistically, continued high growth rate should not be expected, or would not be what history would suggest. For some perspective, a comparable player in terms of size who’s also growing rapidly is AWS, which is already at 10-15% growth. Likewise with Microsoft’s Intelligent Cloud business, which is at an 80bn+ run rate growing at 16%.

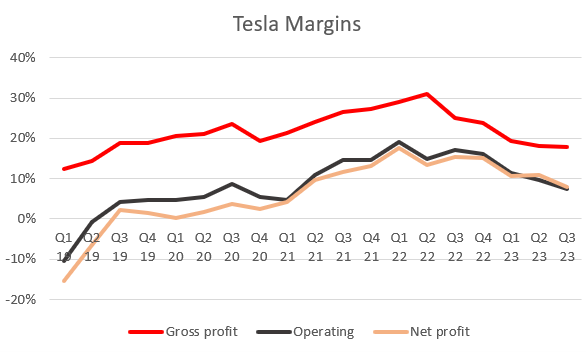

Moving down the income statement, Tesla generated 4.17bn in gross profit, down from 5.3bn in the comparable quarter. The respective margin declined by 720bps, from 25.1% to 17.9%. Operating income was 1.76bn for the quarter, implying a margin of 7.6%, continuing its downtrend and dropping 960bps YoY. Lastly, Tesla generated 1.85bn in net income, operating at a 7.9% net profit margin, which also declined over 700bps on a yearly basis.

Tesla brought in 3.3bn in cash from operating activities, down from 5.1bn last year, but up from 3bn last quarter. On the other hand, capital expenditures were a record 2.46bn, representing 10.5% of revenue. Over the last twelve months, cash from operations was 12.16bn while CapEx was 8.4bn. Tesla is still in an almost complete reinvestment mode.

Management employs a lot of cash to build gigafactories, improve old ones, improve products and develop new technologies. Most CapEx, though, is destined towards capacity expansion, both in terms of EVs and Tesla’s supercharging network. Free cash flow was 848M for the quarter. The business generates vast amounts of cash from operating activities but reinvests most of it.

Breakdown By Segment

Automotive

In the third quarter of 2023, Tesla produced a total of 430,488 vehicles, increasing 17.6% over the prior year. At the same time, it delivered 435,059 EVs, more than 24% over the comparable quarter. Both deliveries and production were below the last quarter, but continued to be in line with 2023 numbers. Production decline was called for on last Q:

“we expect that Q3 production will be a little bit down because we've got some shutdowns to for -- a lot of factory upgrades” Q2 2023

“During the quarter we brought down several production lines for upgrades at various factories, which led to a sequential decline in production volumes” Q3 2023

Relative demand for Teslas has been quite uncertain given the mismatch that had been taking place between production and deliveries, with price cuts playing a role in the narrative. Management called for the persistent mismatch for the past quarters and I suspect that this one, given the shutdowns for upgrades, does not necessarily imply such mismatch is over.

In absolute terms, demand is strong. If it wasn’t, deliveries couldn’t have grown at the 45% CAGR they have achieved over the past four years. Finally, days of supply in inventory was 16 days at the end of Q3, same as they had been in Q2.

All of this translated into 19.62bn in revenue for the automotive segment, implying a yearly increase of 5% and a 7.7% sequential decline. Moreover, it generated 3.66bn in gross profit, which was severely down from last year’s 5.2bn and from last quarter’s 4.08bn. The margin at which this business operates has suffered greatly during 2023 due, primarily, to price cuts. Lastly, the gross profit margin was 18.7%, declining 50bps QoQ and 920bps YoY.

As negative as price cuts had been qualified by investors, they allowed Tesla to continue growing at this pace at an almost 100bn run rate. As a consequence, the company has repeatedly captured market share in the main regions where it operates. All US/Canada-China-EU market share have ticked upwards in Q3, though EU is not shown in the chart.

“Model Y remained the best-selling vehicle of any kind in Europe year-to-date” Q3 2023

Having more Teslas being driven around is not only beneficial from a financial standpoint, but it also helps to continue feeding the FSD software. The pronounced increase in vehicle deliveries immediately translated into accumulated miles driven with FSD’s Beta. It has now surpassed the 500M mark and exponential accumulation should continue since delivered Teslas are still out there, but more will be joining.

“There's just no substitute for massive amount of data. And obviously, Tesla has more vehicles on the road. Then, collecting this data, then all of the companies combined. And really, just don't know how anyone could do what we're doing.”

“We have commissioned one of the world's largest supercomputers to accelerate the pace of our AI development, with compute capacity more than doubling compared to Q2.”

A key component of Tesla’s automotive segment, from a technological and competitive perspective, is their network of supercharger stations and connectors. Both continue to grow at 30%+ rates and have now more than quadrupled over the past 4 years. The company is putting real emphasis on this infrastructure, which should turn Tesla into an almost monopoly-holder, as replicating it is immensely costly and time consuming.

“Our team is focused on materially expanding Supercharging capacity and further improving capacity management in anticipation of other OEMs joining our network.” Q3 2023

This allows us to deviate and cover Tesla’s services & other segment, which includes non-warranty after-sales vehicle services and parts, sales of used vehicles, retail merchandise, paid supercharging and vehicle insurance revenue.

Services & Other has now become a significant business. During Q3, it generated 2.16bn in revenue, growing at 31% year-over-year and slightly sequentially. This puts its 4yr CAGR at 41%. The business unit operated at a 6% gross profit margin, which declined 170bps QoQ and expanded 200bps YoY. Margin volatility is somewhat expected, though it is remarkable it has gone from -40% to these levels in 4-5 years.

Energy Segment

Tesla’s energy generation and storage segment had tended towards nowhere for a couple of years, but it started to quickly gain traction after 2020. Since Q1 of 2020, revenue multiplied by a factor of 5, with it being a record 1.55bn this past Q. Moreover, like most of Tesla’s business units, it has been showing noticeable signs of operating leverage. Gross profit for the segment was 381M, implying a gross profit margin of 24.4%. The latter expanded 600bps QoQ and 1510bps YoY.

In this line, energy storage deployment in 2023 has experienced a dramatic rise, measured in gigawatt hours. Storage deployments were a record 3,980MWh during the third quarter, up over 90% over the comparable period.

“Continued growth in deployments was driven by the ongoing ramp of our Megafactory in Lathrop, CA toward full capacity of 40 GWh with the phase two expansion” Q3 2023

Management’s Commentary and Outlook

Some specifics before the details:

50% production CAGR is maintained

There is ample liquidity to fund product roadmap and capacity expansion plans

Effort is being put on reducing cost of manufacturing, but management expects AI, software, and fleet-based profits to accelerate

Cybertruck is on track to be delivered this year

Huge tone of worry from management. Elon had been mentioning how bad the macro is, with interest rates climbing higher and higher, during all 2023 if I’m not mistaken. Nonetheless, this was the quarter were the highest degree of emphasis was placed on this topic. He continuously reiterated how it is destroying people’s budgets, therefore reducing demand of cars. To equalize the effect, prices had to be cut further.

In this line, when asked about their plans, Elon mentioned a couple of things. Firstly, with regards to their new factory in Mexico, he confirmed they will be building it, but the construction will take place when uncertainty dissipates a bit, with his guess being beginning next year. Interestingly, the CFO mentioned Tesla will continue to invest meaningfully in R&D, primarily driven by Cybertruck’s prototyping and testing, Optimus and Dojo. Likewise, capital expenditures should continue trending higher due to factory upgrades and the supercharging network’s expansion. The team believes these investments are necessary for Tesla’s long-term success.

“We will continue to invest significantly in AI development as this is really the massive game changer. If you have fully autonomous cars at scale and fully autonomous humanoid robots that are truly useful, it's not clear what the limit is.”

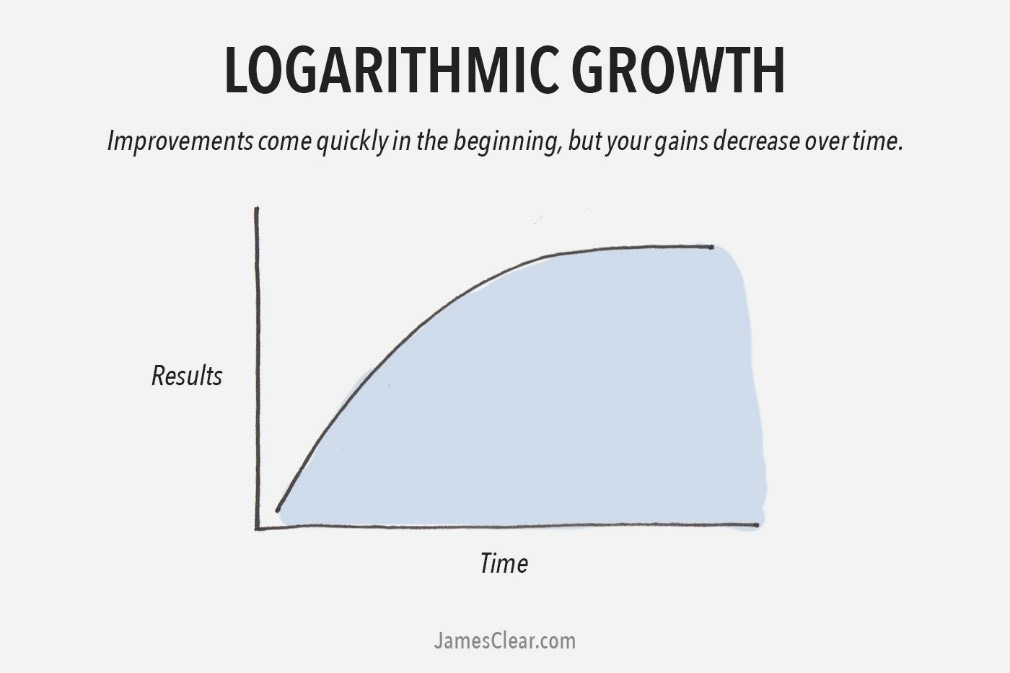

Regarding FSD, Elon mentioned that his prior optimism was due to the shape of the improvement’s curve. He says it very much resembles that of a log curve, with very rapid growth at the beginning, but with a somewhat natural tendency towards an asymptote. Therefore, extrapolating initial growth causes an inaccurate forecast. Elon referred to FSD’s technology as a series of stacked log curves.

“So, if you keep stacking them, keep stacking logs, eventually get to FSD”.

Another point of analyst’s concern was margins. Management mentioned their successful efforts in reducing the COGS of EVs, their updates in factories that should contribute to the bottom line, and how they are extremely focused on continuing attacking all cost buckets possible. However, prices are still affecting margins and the high-kept pace of investments are not helping in this regard either. The last headwind margins will continue to face is the ramp of Cybetrucks’ production.

Finally, on Cybertrucks, management simply said that “demand is off the charts. We have over 1 million people who have reserved the car”. However, the problem lies on how will supply be achieved on a profitable basis. Scaling production for something completely new is immensely complex due to the fact that there’s no one to copy, which makes building the machines that build the machines a necessary evil. Moreover, doing so profitably, is almost impossible.

“That is why there have not been new car start-ups that have been successful for 100 years apart from Tesla”

Elon did say, though, that his best guess is that it might take 18 months for the Cybertruck to be a significant cash flow contributor.

My Take

Financials for the quarter look awful, there is no way around that. However, what’s curious about Tesla’s case is that these are mostly self-inflicted wounds. I believe it is up to each investor’s interpretation to judge whether they are correct moves or not. On the one hand, one could simply argue that price cuts reflect nothing more than a material loss of pricing power. Furthermore, a case could also be made that, due to competition strongly setting foot in the industry, the reached levels of operating margins in 2022 are not repeatable. Similarly, it could be stated that Tesla’s investments in dream-like technology will yield no results.

My view is the complete opposite. It all begins with the customer. What I see is a management team so customer obsessed that, as soon as they successfully reduce costs, they don’t seek margins, but customers’ savings. In a similar line, something I try to keep in my conscious memory is Nicholas Sleep’s definition of ‘Scale Economics Shared’:

“Scale economics shared operations are quite different. As the firm grows in size, scale savings are given back to the customer in the form of lower prices. The customer then reciprocates by purchasing more goods, which provides greater scale for the retailer who passes on the new savings as well” Nick Sleep, 2008 Letter

“Our judgment is that relentlessly returning efficiency improvements and scale economies to customers in the form of lower prices creates a virtuous cycle that leads over the long-term to a much larger dollar amount of free cash flow” 2006 Letter

Yesterday, I covered in this article why I believe this is ultimately the best strategy the business can follow. It doesn’t leave room for disruption to occur and, moreover, customers end up recognizing these efforts and reciprocate in the form of brand loyalty. A fortunate and perhaps unintended (?) consequence of these measures is that it takes competition out of the game, and more so in an industry where almost nobody is able to profitable build and sell these cars.

On the investment’s note, there are a couple of points to touch. When FSD 100% materializes, the value per car will increase dramatically and it will open up multiple new revenue streams. However, more importantly, it should add Tesla a relevant real option it could exercise. Because of its transferrable nature, management claimed it would be what would power subsequent products Tesla would develop, such as Optimus.

The feasibility of such endeavors must be carefully considered. What I do know for certain about Tesla is that its biggest competitive advantage is in manufacturing. Ever since the early 1900s, there had been no new successful car company until Tesla. In the 2000s, an innumerable amount of green energy companies emerged, yet almost none came out of the down cycle. The reason why Tesla was able to perdure was the team’s superb manufacturing capabilities, which can be leveraged for new products. Even if none of these become a reality, the addressable market of EVs already give room for an immense company.

My final thoughts on this quarter go around something a friend pointed out about Elon. Even though he might be regarded as reckless, it is overlooked how calculated every single of his decisions is. What perfectly illustrates this feature is when he was asked about Tesla’s plan of constructing in Mexico. Part of the answer was as follows:

But I am still somewhat scarred by 2009 when General Motors and Chrysler went bankrupt. While that's now 14 years ago, it's -- that is seared into my mind with a branding iron because kind of Tesla was just hanging on by a thread during that entire time and with -- I mean, we closed a financing round 2008 at 6 p.m. December 24, Christmas Eve. And if we had not closed that financing round, we would have bounced payroll two days after Christmas.

So, we actually closed that around the last hour, the last day that it was possible, stressful to say the least, and then barely made it through 2009. So, I'm like -- I want to just -- I don't want to be going at top speed into uncertainty.

If interest rates start coming down, we will accelerate.

Personal Commentary

Long review, but hope you have enjoyed it. I’m getting the feeling that all the reads I’ve been doing these past time are yielding results and showing in things like my takes on earnings, which is wonderful to see.

Contact: giulianomana@0to1stockmarket.com

Disclosure: This is not financial advice.

Me ha gustado mucho el artículo, Giuliano. Y tienes razón, se nota tu evolución. Enhorabuena por tu trabajo y esfuerzo!