Before going into it, I’ll also be covering Visa, Google, Microsoft, Texas Instruments, Mercado Libre and some other companies. If you’d like to receive the earnings reviews at your email, you can subscribe below.

Overall financial analysis

Tesla has been going through a period with unusually high coverage in the media. A lot of things have happened since the beginning of this year, and, news agencies and people always take advantage of weak price actions. Fear and bad news are what get the most eyes. In this article, I’ll try to provide some context on how did Tesla perform in the first quarter of 2023.

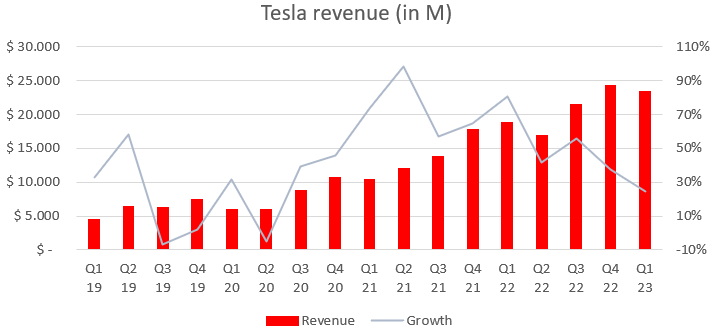

The company reported 24% YoY growth in their topline and a 4% sequential decline, generating 23.3bn in revenue. Tesla has been in hyper growth mode ever since inception practically and it had accelerated since 2020. Year over year growth peaked in the second quarter of 2021 and has been falling ever since. Nevertheless, given the company’s size, it is more than impressive that it can retain high levels of growth.

Tesla has been cutting prices for a while now and this has had a severe impact on the company’s financials. Tesla had 4.5bn in gross profit, down 17% YoY, meaning the GPM contracted by 977bps. In the same line, the company operated at an 11.4% operating margin, down 780bps from a year before. Lastly, Tesla generated 2.5bn in net income, implying the net profit margin also contracted by around 700bps.

At an operating level, Tesla brought in 2.51bn in operating cash flow while it invested 2.07bn in property plant and equipment. This leaves the company’s free cash flow at 440M for the first quarter of 2023.

Breakdown by segment

Automotive

In the first quarter of 2023, Tesla produced 440k cars or 44% more than it did in the previous year. On the other hand, it delivered 36% more Teslas, number which got to 422k. Record production and record deliveries.

Demand for Teslas is quite uncertain. While management claims demand highly exceeds capacity of production, the mismatch between the two continues to be there. At the same time, global vehicle inventory (days of supply) has been increasing quarterly, from 3 in the comparable quarter to 15 in this one. Nonetheless, deliveries are still growing at an extremely high rate, meaning demand is strong in absolute terms.

All of this translated into 19.9bn automotive revenue for Tesla. Topline for the business unit grew 18% year over year and declined 6% sequentially. Gross profit for the automotive segment suffered severely from the price cuts the company has been undertaking. The gross profit margin declined 1200bps YoY and 500bps QoQ.

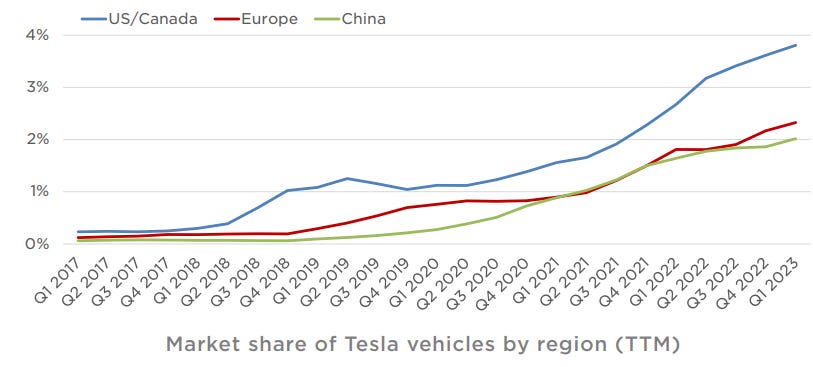

The pronounced growth in vehicle deliveries has allowed the company to continue grabbing regional share in the three main ones in which they have footprint.

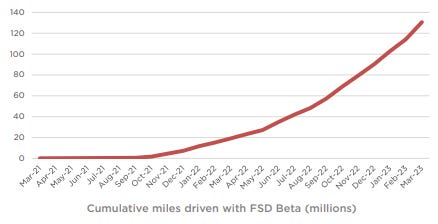

The fact of more cars being driven is not only positive for the company from a financial perspective, but it also helps Tesla continue feeding its full self-driving software. To date, the FSD Beta has over 150M miles driven accumulated. Management gave two particular quotes on how this helps strengthen Tesla’s competitive advantage.

“This level of data collection is unprecedented in the industry. Mass collection of diverse datasets is essential for AI-based approach”

“this is a data advantage that really no one else has”

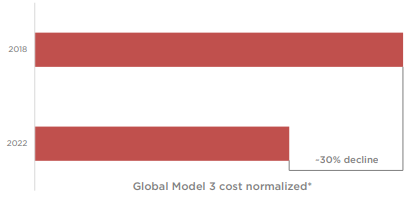

Lastly, in the quarterly deck, an included chart showcases the decline in costs the Model 3 has had over the past 4 years. Tesla’s team has managed to cut them down by 30% over the last 4 years.

The last point I want to touch in this section is the supercharger stations and connectors the company constructs and produces. Tesla has built 1223 stations in the past year, meaning their presence has increased by 33% YoY. Superchercharger connectors have grown at a 34% YoY rate and at a 37% CAGR over the past 4 years

Energy segment

Tesla’s energy generation and storage products have been tending towards nowhere for a couple of years, but, since 2020, they have started getting a lot of traction. As of the last quarter, revenue for the business unit was 1.52bn, an increase of 148% YoY and over 16% sequentially. Moreover, gross profit for the segment had been in negative territory for a couple of quarters or slightly breakeven. However, since the second quarter of 2022, energy G&S products gross margin has oscillated around 11%, showing some signs of operating leverage kicking in.

Revenue clearly reveals in a transparent manner how the segment does. Backing it up, Tesla got to deploy almost 4 GWh in energy storage in the first quarter, increasing dramatically from previous quarters.

“The ramp of our 40 GWh Megapack factory in Lathrop, California has been successful with still more room to reach full capacity. This Megapack factory will be the first of many. We recently announced our second 40 GWh Megafactory, this time in Shanghai, with construction starting later this year.”

Outlook and management commentary

In all quarterly decks, the company includes some key points regarding their outlook. On this occasion, it was as follows:

“We are planning to grow production as quickly as possible in alignment with the 50% CAGR target we began guiding to in early 2021.”

“We have sufficient liquidity to fund our product roadmap, long-term capacity expansion plans and other expenses.”

“We continue to believe that our operating margin will remain among the highest in the industry”

In the conference call, management went over many important topics. Firstly, they explained their intentions behind the price cuts. Tesla is aiming to be massively available and for this reason they have to make cars as affordable as possible. This means they are pushing for as low prices as they can, maintaining healthy margins, to maximize the volume of cars sold, not profit per car. Management also said they can’t get into the details on what makes them change prices, but they do confirm is a very actively thought point by the leadership team.

To further expand on their margins situation, they mentioned two particular things. From a philosophical perspective and as a form of general guidance, management said they generally look to mid-20% gross margins for any programs they launch. Additionally, they “are aggressively going across every cost bucket they can”.

In addition to this, two major costs are mentioned within the universe of variables they do not control. On the one side, logistics has been damaging the company’s margins for a while, but management mentioned it is now moving in their favor. The second one is the commodities world, in which we still are “kind of at the maximum of pain for commodities in our cost structure”

Secondly, they addressed the demand concern by simply saying the following two statements:

“Model Y became the best-selling vehicle of any kind in Europe and the best-selling non-pickup vehicle in the United States.”

“I think the overall thing we can say is that orders are in excess of production.”

In parallel, the energy generation and storage business has been gaining a lot of momentum and many questions were made about the segment. Management said that in a few quarters, they’ll perhaps include production and delivery of this segment in their press releases and particularly discuss guidance.

And, in other news, they anticipate having a Cybertruck delivery event in Q3.

My take

Financials obviously did not look good this quarter. There has always been a lot of volatility in the company’s quarterly free cash flow and periods in which it was much lower on a QoQ so I’ll abstain from drawing a profound conclusion here. I think we’ll see throughout the year, as quarters go by, but a single one of them can tell very little about long-term trends.

Tesla still has a net cash position of over 17bn and it’s profitable on every single basis, meaning the company has complete flexibility to try play for their long-term strategy. They mentioned several times how thoughtful they are in maintaining a financially healthy state, it’s not growth at all costs.

To my eyes, Tesla’s team is doing what they have to do (cutting prices). Moreover, it is exactly what has been in their plans for a very long time so it should come as no surprise that they are acting on it. The following statement is from Elon Musk in 2006:

“The strategy of Tesla is to enter at the high end of the market, where customers are prepared to pay a premium, and then drive down market as fast as possible to higher unit volume and lower prices with each successive model”

Tesla clearly had a lot of ground to reduce prices given the high margins they were operating at, and, given the 30% price reduction in the last 5 years, it is dazzling the company’s operating margins are still high in relative terms:

Finally, the thesis for increasing the volume of units sold goes around the different software and related offerings they have and will be created around cars. Tesla is building an ecosystem and, once that’s in, vertical offerings like FSD should offer cash flow avenues upon the customer base. It’s a very similar strategy as the one Apple followed. This is what Elon said regarding this point.

“But actually, we do have this unique strategic advantage that we have -- we're making a car that if autonomy pans out and we think it will, where that asset is actually will be worth a hell a lot more in the future than it is now. So, it is taking to be possible to sell it at zero profit, but still have the net present value of future cash flows associated with that asset very significant.”

Personal commentary

I hope you enjoyed the article. I’ll be covering Visa, Microsoft, TI, Mercado Libre and Google at least. If you’d like to receive the reviews at your email, you can subscribe below!

Disclousre: This is NOT financial advice.

¡Muy bueno compañero! Te felicito.

¡Trabajazo!