I decided to follow a somewhat similar path to the one I followed with Buffett, which basically consisted on two instances. Firstly, I tried to infer each investor’s philosophy (already did that). The second step was to attempt to define which letters are the most relevant and must-reads, with the intention of saving you some time.

Trying to do this with Warren’s was a complete struggle. However, I didn’t find most of Terry’s letters as authentic fountains of wisdom as it happened with Buffett’s. This allowed me to narrow down the universe of masterpieces to only one, great news for you.

I think Warren Buffet letters reach an absurd level of financial philosophy. I think Terry does not get to the level of deep thinking Warren does, but he is for sure as good a teacher as Buffett. Throughout this decade and something of writing, Smith shares an uncountable number of insights, and his 2021 letter, in this sense, is absolutely brilliant.

On valuations and good businesses

In investing, rules of thumb are intrinsically worth nothing. Even though they may act as guidance, if we isolated and evaluated their core, we would find futility.

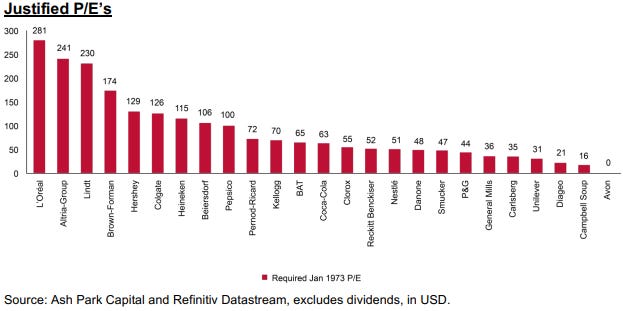

The first point that caught my eye in this letter is when Terry tears apart the idea that paying high PEs for companies invariably leads to underperformance.

Multiples intend to offer some sort of parameters in terms of how expensive is a business trading in respect to its own fundamentals, like earnings or sales. Nonetheless, the number itself is useless and this cannot be taken by granted. Terry computes and interesting chart with this idea in mind.

This illustrates what PE ratio you could have paid for each of these companies in 1973 and still achieve a 7% CAGR over the next 46 years, outperforming the 6.2% obtained by MSCI’s World Index. The study is of course biased, as all, and companies are cherry picked, but the point is still valid.

One important reminder:

“I am not suggesting we will pay those multiples but it puts the sloppy shorthand of high P/Es equating to expensive stocks into perspective.” January 2022

“Past returns of companies are a good guide to future returns”

This is a fascinating one. The first time I came across the following concept (in a well-defined manner) was while reading Buffett’s 1985 shareholder letter. In it, he states:

“A textile company that allocates capital brilliantly within its industry is a remarkable textile company—but not a remarkable business”

The quote encompasses the idea that good returns on capital are inherent to industries and businesses. Moreover, there’s some sort of restrictions or ceiling imposed to the maximum returns a company could earn, based on these intrinsic fundamentals. Terry brings the same idea to the table, but it accompanies it with this:

The chart is composed by the thousand largest companies in the US, which were sorted into quartiles based on their ROE. The green line represents companies in the lowest quartile, while the red one, the opposite group.

It is extremely insightful to observe how there’s some sort of mean to which these companies’ returns tend to. Variation is all across the board from period to period, but it is clear how good companies always tend to return to the 18-20% ROE while the bad ones return to 10-12%. Besides, it is key that the study covers 50 years. A long period is the main ingredient when examining sustainability of returns on capital.

Terry further addresses the matter with an even clearer illustration:

The chart above shows the achieved annual return on invested capital over two different periods and across industries.

“These return characteristics persist because good businesses find ways to fend off the competition — what Warren Buffett calls ‘The Moat’”

“Poor returns also persist because companies which have many competitors, no control over pricing and/or input costs, and an ability for consumers to prolong the life of the product in a downturn (like cars) cannot suddenly throw off these poor characteristics just because they are lowly rated and/or benefit from an economic recovery”

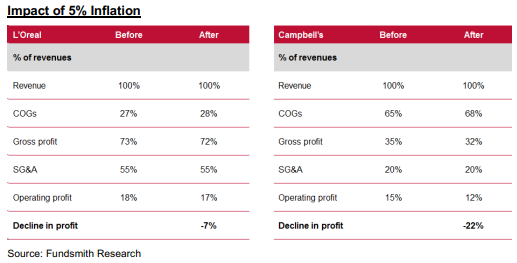

On inflation’s impact

Inflation has always been in investors mind, but its recent appearance and persistent nature started raising some concerns. In this letter, Terry addresses the issue by sharing a phenomenal yet simple table regarding inflation’s impact on businesses performance:

The table shows that companies with higher gross margins have their profitability far more protected than those with lower gross margins.

Terry also takes the time to expand on another matter that inflation affects, valuations. The longer the maturity of a bond, or the further in time the asset’s cash flows, the more sensitive is its valuation to changes in interest rates. The same happens with companies and that’s one of the reasons why unprofitable tech have performed so poorly recently. Since all of their value is derived from cash flows that will be produced long time from now, they are more susceptible to changes in interest rates, because the latter discounts those future cash flows into “today’s dollars”.

Personal Commentary

I found this letter outstandingly straightforward, simple to understand and very insightful. I think there’s a lot of value in these scattered pieces of information and thought some value could be created by putting them together and providing some context. Hope you enjoyed today’s article and, if you have, feel free to subscribe below.

On the research front, I began working on the next write up. Zoetis is the company I’ll be covering.

Looking forward for your next write up about Zoetis. It is one of my core position and I see a lot of upside potential for this one. Cheers!

I see Terry in the same way you see him. This year letter was quite interesting, thanks for sharing Giuliano. Great job as always!