SuperCom - growing 40% at potentially ~2x 2026 EBITDA

Accounting exercise on current investment opportunity

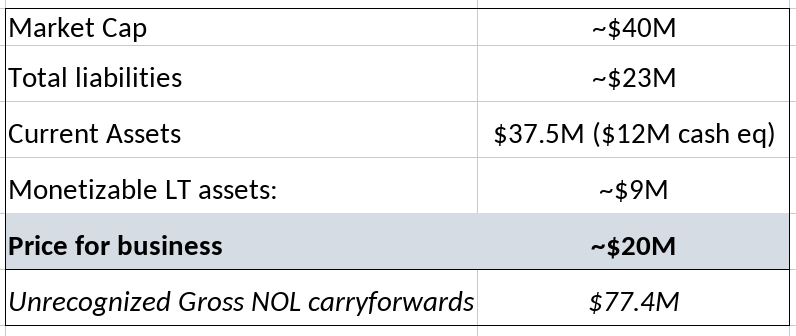

The company reported their 20-F last Tuesday and it’s unclear to me what to think of it. From a mathematical point of view, it seems at an attractive level:

SuperCom withstood two long decades of disastrous managerial administration. Ordan Trabelsi, son of the former CEO, was leading the US division; he took it from $0 to $6-10M in sales in less than a decade. The division seems to have operated profitably, winning several electronic monitoring deals and had done a very lucrative acquisition in 2016. All this while the parent company was struggling.

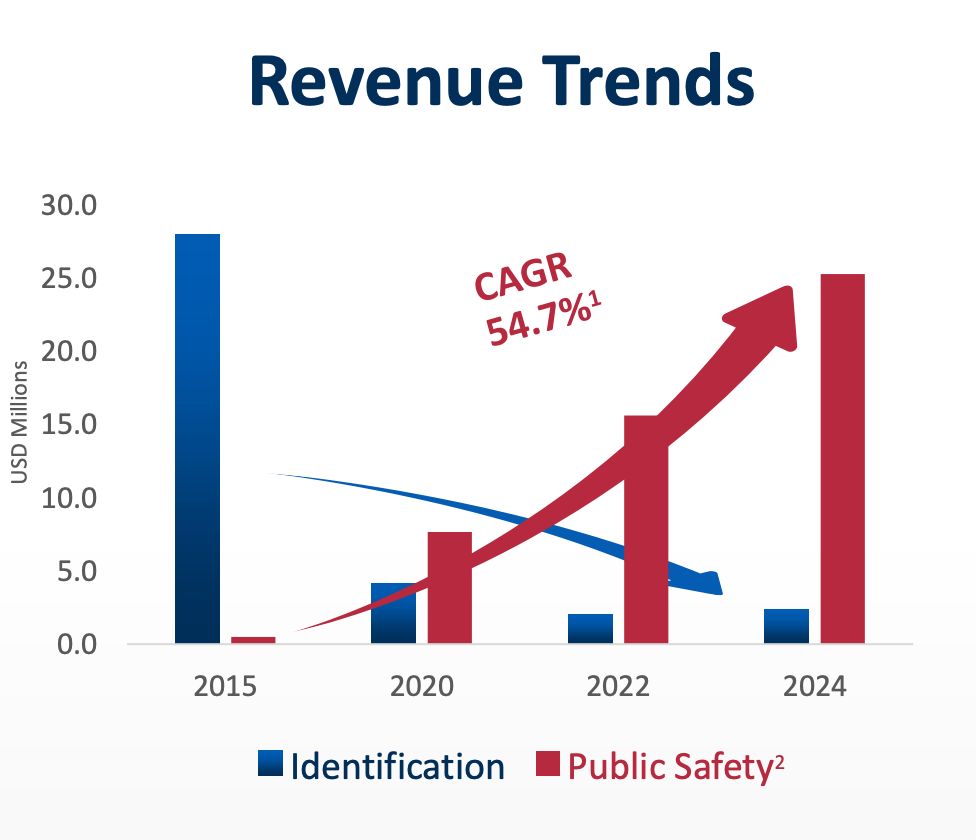

Ordan takes over as CEO in 2021 and turns the business around. He discontinues legacy activities and focuses the business on the public safety industry - electronic monitoring for public offenders and related products. In 5 years, he secured deals with 10 governments in the EU (Sweden, Germany, Romania), achieving a 65% win rate in national gov tenders; secures gov with Israel, 35+ county-wise deals in the US, and a state-wide deal with Arizona.

Much of the business SuperCom is getting is repeat business from these customers. The company has managed to scale up from $100k deals in Lithuania to $10-$35M deals among the mentioned national governments.

The business’ economic profile changed materially. 60-80% of their revenue is ‘recurring,’ for these are 1-10-year contracts, and I’d estimate equilibrium gross margins to be in the 55-70% range.

The underlying business has grown at a 10yr CAGR of 50% and excluding a huge deal impact, it grew ~40% in 2025. RPOs increased from $16M in Dec 2024 to $55M in Dec 2025 and 39% of the $55M are getting recognized over 2026, meaning baseline revenue is $21.7M. It’s likely that they grow at 25-50%.

A $17M deal with Sweden (4th with them) was announced in March. Management mentioned in the call there’s room to materially increase size. Another one was announced with an undisclosed national government (according to my dd, maybe England - worth $10-$100M). And Arizona happened in late 2025.

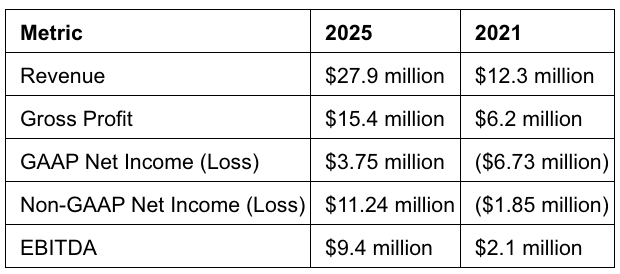

The business is doing extremely well from an operational, p&l standpoint. Balance-sheet-wise, debt got reduced by ~$10M in 2025 and book value increased from $11M to $43M, though shares outstanding increased from 2.2M to 5.4M (more on this later).

The issue lied/s in the mismatch between the narrative, the accounting, and management’s actions.

What’s happening at an accounting level - Why I struggled with it

The margin of safety embedded in the business price largely originates from the $25M in receivables. At first, I thought A/Rs were bound to decline because a large portion belonged to the legacy business linked to African governments. As those got off the books, AR’s quality should rise and so should collectability. But receivables continue to mount up. I didn’t understand what was going on.

Management mentions the US as a pure ARR business, likewise for Israel. And I thought about the classic SaaS model, where you provide the service and get paid on a per-month basis. Otherwise, it could be a HaaS model, where you own the hardware, hold it in your balance sheet, and get paid per month as well. But none seem to explain their accounting.

Management doesn’t speak about Europe’s model in a SaaS way.

Further, in 2025, SuperCom reported US sales of $6.8M and $6.9M in Israel.

So, if 70% of revenue is recurring, and you earn that much in the US and Israel, how is it that products sales were $21.4M in 2025 and services sales were $6.4M?

In addition, my understanding is that management sells the thesis of buying the equipment and leasing it out on a daily rate. To that effect, they hold $3M in PPE that’s located in Israel. However, no PPE is to be found in the US or EU.

Some things I still ignore, but I think it all comes together as follows:

In EU, the government buys the hardware (ankle bracelets) and SuperCom stays as software provider for the length of the contract. But govs typically pay for the whole thing over the length of contract.

This is the opposite to the typical SaaS deferred revenue. SuperCom finances governments’ purchase, creating a disastrous cash economics model. SuperCom spends millions upfront to build a hardware they get paid for over time. For reference, FCF has been systematically negative, being ~$-8M in 2025.

In the US they partner with local distributors, who go around bidding on county-level contracts. Same deal - SuperCom builds and ships hardware, and stays as SaaS provider. Payment terms here are better, quicker - ARs don’t build up so much.

In Israel, they own the hardware and lease it at a per-day rate. Thus, here they charge for the equipment lease + SaaS platform.

Management reported that each offender signifies an average $2,900 ARR. And I suspect this is a fully blended average, among the 3 models.

In the last 20F, SPCB split receivables into 2 components. I first thought the long-term part (~$9M) was the residual of African bad debt, but at a second glance, part of it might be the hardware shipped for the large EU contracts that will get paid over time. The ~$15M which remained current might be truly current now.

The question of management

I struggled like hell to understand their lease-based accounting and different economic models. Management doesn’t speak much about how it all comes together and they refer to a somewhat unified version of the story. Even though they might say EU is more front-loaded, specifics aren’t given on the how or why. It’s likely that this is a byproduct of me needing more training in accounting and not their fault.

Some other accounting-related things caught my eye:

$5.2M in patents held for sale since at least 2021. This constitutes a large part of the $37M in current assets.

They recorded provision for credit losses related to the legacy business of $1.8M, $1.2M, 1.4M in 2025, 2024, 2023 respectively. Total allowance for bad debt sits at $17M and I haven’t seen their estimate or opinion of how much of currently held receivables are from the legacy business.

Company reported $3.75M in net income for FY 2025, but $2M in tax benefits in Q4 and debt forgiveness gain of $4M in Q1.

Company is doing well on the p&l but management doesn’t speak much about the cash flow statements.

Of insider Ownership

In Dec 2024, management owned 196,000 shares (9% of outstanding).

And, as of Dec 2024, 40k options were outstanding with a weighted average exercise price of ~$50-$70 per share.As of Dec 2025, 31k options were outstanding; exercise price of ~$3 ?

As of April 2026, management owned 54k shares (<1% of total).

In April, a form 3 was filed for Ordan. He now owns 268k options with an exercise price of $0.0033?

Same for Barak Trabelsi. Now owns 201k options, same exercise price.

I don’t know what happened. Two possibilities: (i) management sold their equity at a loss and granted themselves “free” options; (ii) they exchanged their equity for options after finalizing reverse splits and exchanges of debt to equity. I can’t find the pertinent filing explaining all this; (ii) is more likely.

In any event, Ordan currently holds some ~4.8% of shares outstanding, similar to what he owned 2 years ago.

The dilution risk

SuperCom was essentially destined for bankruptcy. Ordan inherited a large legacy business which had customers who didn’t pay and was based on large one-off deals. He’s about to fully finalize the turnaround, but it was a ride.

Multiple debt-for-equity exchanges occurred over the past few years, mostly at premiums over share price. Notably, the January 2025 conversion was for $4.374M in debt for 100,000 shares ($43.74 per share). This also pushed the maturity of the debt to 2028 and accrues interest to be paid full at maturity. In August, $2.59M in debt was converted into 225,000 shares ($11.5 per share).

Same story with subordinated notes. SuperCom converted ~$17M of subordinated debt into common shares. Warrant issuance accompanied some of the conversions.

A portion of the former was done to clean up the balance sheet and avoid bankruptcy. However, I suspect another part was destined to fund the company’s growth, given the terrible cash economics of the business. If they manage to land another $20-$50M contract, it’s not obvious they can fund it with cash on hand without leaving SuperCom in a fragile position. Thus, equity issuance remains a possibility.

In addition to this, SuperCom had to do two reverse splits to remain listed on the Nasdaq exchange. A one-for-ten in November 2022, and a one-for-twenty in August 2024. The latter wasn’t mentioned in company PRs nor earnings call, but a 6-k got filed and confirms it.

Final Remarks

Conclusively, it’s a mess. I’m inclined to think Ordan is doing whatever he could to keep the business alive. It’ll be interesting to observe how he plays his hand hereafter. The business remains burning cash. Everything will be determined by the quality of their receivables.

And it’ll be interesting if people get surprised by the company’s 2026 p&l.

Disclosure: This is not a recommendation to buy or sell any security. I may own a position in some of the securitie(s) discussed. In addition, so much going on that I might’ve missed something; this is just the result of my dd and opinion.