This one will be quite a read, feel free to subscribe after skimming through it!

Mission

“Our mission is to connect the world through the most innovative, convenient, reliable and secure payments network, enabling individuals, businesses and economies to thrive.”

History

In the 1950s, the financial credit system was not very developed. Different merchants used to have their own credit system, upon which then they transacted with clients. Therefore, people had revolving credit accounts with all the different merchants, each of the latter having their particular card. This forced the general public to pay separate bills through separate mediums, which sounds absurdly inconvenient.

Visa was founded in 1958 by Bank of America as a credit card program, originally called BankAmericard, to deal with this issue. The conceptual solution, which had been tried before, was issuing a super card, an instrument that would unify the complete spectrum of the payments system. To test the product, BofA went to Fresno, where they had around 45% market share. The initial attempt went smoothly and, by 1959, Bank of America distributed this new credit card to over 2 million people in the state of California.

In 1966, Master Charge (now Mastercard), appeared on the scene as the consequence of an alliance between several banks, to combat BankAmericard. Legal restrictions made expanding to other states a real issue. To do so, and not get displaced by this new competitor, BankAmericard started signing agreements with other banks, from different states. In 1970, Bank of America gave up control of the project to this ‘banks council’. They created a corporation called National BankAmericard Inc.

As of 1972, NBI had licenses to operate in over 15 countries. A year later, NBI launched the first electronic authorization system, followed by an electronic clearing and settlement system. The completeness of the initiative turned out to be the precursor to VisaNet, which is basically the Visa Network, the one that powers all transactions.

In 1974, it got quite difficult to administrate BankAmericard after its international expansion. To efficiently manage it, the International Bankcard Company (IBANCO) was founded. Later in the 70s, by 1976, the different banks and program names united themselves as one, under the name of Visa.

The Visa Network was created with the purpose of addressing the problem people had when making transactions. Each of them was previously processed via different methods. Consequently, VisaNet’s intention was to relief this pain point, offering a single connection point for facilitating payment transactions to multiple endpoints.

Anticipating Demand Surges

Since the 70s, Visa has spent hundreds/billions of dollars for the network to continue being improved and remain ahead of competition. At the beginning of the 2000s, management detected a trend that was pushing transaction demand higher and higher, and it seemed to have only started, electronic payments. Until that moment, Visa’s Network processed all transactions through its first generation datacenters, but in 2005, they completed a multiyear initiative to expand the reach and capacity of the Network. This datacenter had a completely renovated design, up to the most modern technologies. It was capable of handling more than $1 trillion in annual transaction volume and was designed to meet the growing volume of credit, debit and prepaid transactions for the foreseeable future. For some perspective, the network had around 1/2 trillion in transaction volume at that point in time.

The first transactions were processed at OCC (Operation Center Central) in March 2005, and the migration of transactions volume to OCC continued through 2006. For the first time since launching the electronic authorization in the 70s, Visa now had the ability to house multiple authorization systems under one single roof, with better security and back-up technology as well. The transition made the network be always available and with abundant processing power ready to meet new demand.

The second datacenter of this kind was built on 2009. The importance of renewing the technological infrastructure is clear once you get to know the outputs. This is an extract from an article of 2009, stating in words the impact of the improved security:

“Still, despite the rising tide of breaches, the credit card company insists the amount of money that people are actually losing through fraud is decreasing. In the early 1990s, before the rise of e-commerce, Visa lost 18 cents out of every $100. Fraud was much more primitive then, usually resulting from lost or stolen cards.”

Today (in 2008), with global criminal enterprises actively trying to steal customers' financial information, fraud is a much more sophisticated business. Yet despite that, Visa says its loss has declined to 5 cents for every $100.”

In 2018, once again expecting a continued abrupt growth in transaction volume, Visa built two new datacenters that would process transactions in a completely renewed manner, again up to the most modern technology. On this occasion, the company saw the mobile market and the internet of things as potential major fuelers of digital transactions. At the same time, expanding datacenters footprint allowed Visa to cover more ground, helping it to offer a better service to customers worldwide by reducing both the cost and time needed for each transaction.

As of today, these four datacenters make up for the VisaNet, which supports:

3+ billion cards distributed among the global population

16.6k financial institutions

Over 46M merchants

200bn transactions per year

Business Overview

Visa is one of the leading companies in the digital payments industry. The company facilitates global commerce and money transfers across almost the whole planet through their global network, VisaNet. Thereafter, Visa has created a suite of products around their built infrastructure.

To get a bit deeper into the business offerings, we first must define where VisaNet is actually located in this ecosystem.

How do electronic payments work?

In every transaction, there are multiple parties involved and there are different steps needed to complete a transaction.

Consumers are issued debit or credit cards, which allows them to access their money or credit lines and make purchases to merchants that accept such form of payment.

Issuers are the banks that issue these cards to consumers. They are the ones who authorize transactions and guarantee payment on behalf of the consumer.

Merchants are sellers who decide to participate in the network by accepting these payment methods.

An acquirer is the merchants’ bank, who provide merchants access to the network by authorizing their transactions and ensuring they receive their payment.

VisaNet is the network that connects all parties involved, enabling the flow of transactions, through which money payments/transfers are done.

Every electronic payments transactions can be divided into three steps:

Authorization: it is performed when a card is swiped or entered in a PoS terminal. Once the card is read by the PoS, the transaction, the merchant and the consumer’s information are sent to the acquirer. The latter then formats the details and sends it to VisaNet. The network then performs a series of risk and fraud prevention controls to ensure the transaction is valid and secure. If the transaction meets VisaNet’s standards of quality, the request is sent to the issuer, who checks if the consumer’s funds available can cover the payment. If that’s the case, it puts a ‘hold’ on such funds and sends the approval back to VisaNet, which delivers the message to the acquirer. The acquirer reviews all the details once again and sends the issuer’s approval decision to the merchant. Now the merchant can let the consumer leave the store since the payment has been approved.

Clearing: After the transaction is complete, the acquirer transmits the final details of the transaction to VisaNet, which then sorts all transactions worldwide and sends a consolidated batch file to each issuer that has participated in the network. Upon the receipt of this file, the issuer removes the ‘hold’ of the consumer’s funds and debits the amount from the account balance.

Settlement: In this step, VisaNet consolidates all electronic payments worldwide and sends consolidated net settlements to the participating issuers and acquirers. Funds are then transferred between each institution with the count activity to settle all transactions that have occurred within a specific processing timeframe.

In conclusion, Visa owns the Network through which processes flow, connecting all participants during money transfers. Identifying the role it plays enables us to shred light onto some incorrect premises, like when people allegate Visa has a default risk.

“Visa is not a financial institution. We do not issue cards, extend credit or set rates and fees for account holders of Visa products nor do we earn revenues from, or bear credit risk with respect to, any of these activities”

Specifically, Visa offers:

Transaction processing services (authorization, clearing and settlement) to acquirers, issuers, merchants and consumers.

Visa branded payment products that clients (mainly banks) use to develop and offer credit/debit cards, prepaid cards and cash access programs for individuals, businesses and governments.

APIs which can be used by traditional and new players to leverage the network’s infrastructure and be able to process digital payments.

VisaNet has the peculiarity that it can be used as a ‘Network of Networks’. Through this approach, it doesn’t matter the network utilized to start or finish the payment, VisaNet can be used as the network processing such transaction, connecting with the initial and end point.

Visa offers clients issuing solutions, advisory services, open banking, risk detection and identity solutions.

To fuel for growth, the company runs a quite heavy client incentive program. Through it, it pays financial institutions, merchants and strategic partners to grow payments volume, increase Visa’s acceptance and win clients. In 2022, slightly more than a fourth of the total net revenues were employed on client incentives.

Strategy

In its 10-K, Visa goes thoroughly through the strategy they follow to fuel revenue growth as well as to build a sustainable business.

Visa has identified the three main beacons of revenue and works towards improving/excelling at them. These three pillars are:

Consumer Payments.

In this sector, the core products are credit, debit and prepaid cards. To easily enable consumer payments, which would boost card usage, technology had to evolve to a point in which friction, at the time of making a digital payment, gets reduced to a minimum. Pursuing that objective has made Visa focus on these new suites of technologies, called Enablers.

Both ‘Tap to Pay’ and ‘Click to Pay’ have been created with the sole intention of making digital payments smoother to the everyday users. Helping merchants and institutions improve the technologies employed ultimately increases volume by accelerating and enhancing usage.

“We surpassed one billion contactless transactions on global transit systems in fiscal year 2022, an increase of 70% year over year.”

On the other hand, Visa Token Service works basically as a replacement of the 16 digits accounts have with a shorter and cryptographic token.

New Flows

This subsegment makes Visa focus on enhancing new ways in which money could flow by interchanging parties involved in the different transactions.

With this intention in mind, Visa has developed:

Visa Direct, which is a global, real-time payment network that helps facilitate the fast delivery of funds to eligible cards and bank accounts

“In fiscal year 2022, we had 5.9 billion Visa Direct transactions, an increase of 36 percent year over year(...) Visa Direct connected 16 card-based networks, 66 automated clearing house (ACH) schemes, 11 real-time payment (RTP) networks and five gateways.”

Visa Business Solutions are designed to bring efficiency, controls and automation to small businesses, commercial and government payment processes.

Visa Treasury as a Service is a payment service that allows clients to leverage Visa's expertise in FX, liquidity, and ledger-based solutions to facilitate cross border commerce.

Value Added Services

This segment is intended to create new avenues for revenue, independent of the network and building vertically upon each layer.

Visa Data Processing Services, upon cards issuance, provides fraud mitigation, disputes management, data analytics, campaign management. Additionally, Visa provides issuers with account control, digital issuance and BNPL capabilities.

Acceptance Solutions come in hand of Cybersource, a modular platform Visa acquired in 2010. Cybersource enables merchants to improve consumer engagement, mitigate fraud and lower operational costs. Besides it, Visa provides reliable services that reduce the friction of digital payments and drive acceptance (visa contactless payments for example).

Risk & Identity Solutions consist on added layers (to the base one VisaNet has) to prevent fraud and detect risk. Solutions like Visa Advanced Authorization, Visa Secure, Visa Advanced Identity Score, are design with this purpose.

In 2022, Visa acquired Tink, an open banking platform to accelerate the development and transition of open banking. Capabilities range from data access use cases to payment initiation.

The company has an advisory business unit called Visa Consulting and Analytics.

In parallel, management works towards constructing a solid foundation that could provide an angular keystone over which a sustainable and long-lasting business could be built on. The identified areas Visa works to excel at are the following:

Visa aims, as mentioned, to be the Network of Networks, connecting all forms of payments and all endpoints.

Building a state-of-the-art infrastructure is one of the company’s objectives.

Visa has built several layers of security within its network and additional ones as added value offerings.

Building brand awareness is key for the company to keep winning heavy-weight clients.

Visa believes it is key to attract the best talent possible, given the agenda the company has planned. To this end, Visa supports its professionals in all verticals of necessity.

To conclude this section, Visa’s revenue comes from the segments and geographies as follows:

Services Revenue consist on services provided to support client’s usage of Visa’s payment network (does not include processing them). The main driver of services revenue is the payment volume the network handles.

Data Processing’s revenue derives from the number of processed transactions. In this segment, revenue comes from processing clearings, settlements and authorizations, and, the mentioned value-added services.

The International Transactions subsegment derives revenue from cross-border transactions and currency conversion. Demand for international transactions tends to grow as Visa gets to expand the reach and efficiency at which VisaNet operates.

Other Revenue mainly consists of license fees, other value-added services, account holder services and certifications.

VisaNet Usage

Visa finalizes its fiscal year on September, which is when they upload their Annual Filing. The thing is that they report Total Volume, Total Transactions and Cards in the form of the previous calendar years.

So, there will be a slight chronological discrepancy for the following data (a quarter of deviation), but it should not suppose a huge problem. Also, keep in mind the 2022 metrics will be considered for their FY, finalized on September, it is not the end of the calendar year 2022.

First and foremost, the probably most important metric is Total Volume. It measures how much money flowed through Visa’s Network. One thing to keep in mind is that this is different from Payments Volume. Payments volume is the aggregate amount of purchases made with cards and other form factors carrying the Visa, Visa Electron, V PAY and Interlink. Total volume is the sum of payments volume and cash volume.

At the beginning of this period, total volume the company had was 3.8tn and, at 2022, it got to 14.1tn. Over this 15yr timeframe, the exhibited CAGR was 9.1%, resulting in total volume 4xing.

Secondly, transactions processed through the network is a fundamental pillar to Visa’s business. Total Transactions represent payments and cash transactions as reported by Visa clients on their operating certificates. Visa Processed Transactions represent transactions involving cards and other form factors carrying the Visa, Visa Electron, Interlink, V PAY and PLUS brands processed on Visa’s network.

Total transactions grew from 50bn in 2007 to 258bn in 2022, implying a compounded annual growth rate of 11.6%. Out of the 258 billion transactions that were done leveraging VisaNet, card transactions accounted for 74.4%, up from 66% in 2008, but it has oscillated between 66-70% for the past decade and a half.

In the Business Overview section, we went through how electronic payments are done. As seen, for every transaction to occur, multiple parties have to play their role. The following two charts are supposed to showcase the underlying agents powering the processed transactions shown in the chart above.

Visa’s cards in circulation (debit + credit + prepaid) went from 1.5bn in 2007 to 4.1bn in 2022, which equates to more than half the global population. This metric by itself would be kind of empty since cards are the mean people have to pay for things, but the growing demand for transactions are proving growth in cards is not in vain.

Lastly, the platform’s health could be measured upon the number of participants within it, besides their cards. Visa reports the amount of merchants and financial institutions that utilize and/or have partnered with the company. However, going back more than 6 years, data seems unfindable (I truly tried haha).

In 2016, Visa had 16.800 financial institutions as partners and 44M merchants utilizing their network. As of last year, financial institutions accounted for 15.000 and merchants reached 80M. Consistently losing financial institutions could seem like a potential redflag. Nonetheless, it could be that there simply are less financial institutions out there, with some of them continuing taking market share from others. In scenarios like this, it is about the quality and size of the partner, not the number of partners one has.

Industry

Visa belongs to a clear industry, digital payments. Payments are realized for every property transaction, meaning money is the blood of the system we live in. The technological innovation of the past decades, including e-commerce and digital payments, made transactions multiply phenomenally. Digital payments ended up being a tool we utilize with the purpose of buying or selling, but now with global reach and in all existent fields. In consequence, electronic payments got so intricated with the global economy that it’s only logical to assume economic growth only fuels the demand for this technology.

The conclusion at which I arrived above is not a coincidence. Since the beginning of human civilization, there’s a particular tendency that has caught my eye:

The minimization of friction on all sort of transactions, usage, methods, and everything.

People want things to be as easy and non-tedious as they possibly can. Even more so when discussing daily and recurring activities. Therefore, it is only logical to think that if the demand for payments overall grow, the method which will capture most of its growth will be the one that minimizes the friction at the time of paying/selling. Visa’s core relies on innovation and acceptance of new technologies with this objective.

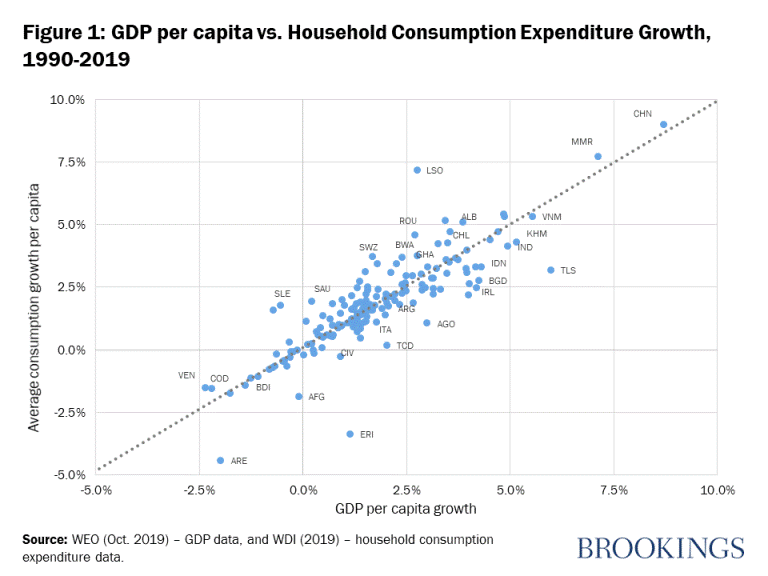

Economic growth means, in essence, GDP growth, which means the total value of all goods and services produced in a particular country increases. The following image illustrates the relationship between GDP per capita and consumption growth.

If we are under a scenario were economies grow, aggregated income should tend upwards as well and so should the avenues in which people can spend money: Consumption, Investment, etc. If that’s the case, that would imply an increase in the demand of payments and, if this happens, people should tend to select the one that minimizes friction, which are powered by Visa.

In the same line, here are some extracts from a published paper by Moody’s Analytics in 2015:

“Electronic payments added $296 billion in real (U.S.) dollars to GDP in the 70 countries/regions studied between 2011 and 2015”

“Countries/regions with the largest increases in card usage experienced the biggest contributions to growth.”

Moody’s got to establish a clear relationship between economic growth and the penetration/usage of digital payments. The reason for this is that electronic payments are vastly more inclusive of the population and it lowers the cost of usage while facilitating payments. These extra people that now participate more actively, and the efficiency at which all participants operate, fuel the economies.

Mckinsey analysts got to the same conclusion, showing what they expect could be the impact of digital payments.

As potential forecasts for some sectors, Statista estimates that Total Transaction Value will grow at compounded annual growth rate of 11.8% until 2027, getting roughly to 15tn.

SkyQuest expects similar growth for the total addressable market of global digital payments. The market was valued at 90bn in 2021 and it’s expected to be worth around 228bn by 2028, exhibiting a CAGR of 14.3%.

Lastly, it is important to keep in mind is digital payments resiliency as a sector. There’s almost no conceivable scenario in which payments or digital payments suffer a severe downturn. As long as economies and businesses are running, demand for transactions will be there.

Thesis

In the previous section, we kind of went through Visa’s thesis, but for further clarification, we’ll synthesize it here. VisaNet is the most important player in digital payments and it got immensely adopted, making a potential displacement very unlikely. The predominant position the network has, should allow VisaNet to be one of the main factors causing this economic growth Moody’s Analytics and McKinsey wrote about. But it doesn’t end there.

Economic growth brings with it higher aggregated income, which, down the road, increases the demand for transactions and cards. In parallel, digital finance brings with it the inclusion of millions and billions of people to the system. Each of these ‘new’ members will demand cards and transactions, as every human being that has to pay for stuff. Here’s what Visa’s CEO had to say in this respect:

“There are still hundreds and hundreds of millions of people to bring into the financial mainstream. There are still trillions of dollars spent on cash and check.” Q1 2023

In parallel, a strong workforce playing in payments’ favor is the Money Supply. One of the main tasks central banks have in the modern world is to continue fueling each country’s GDP by printing money, roughly speaking. When nations grow, if the money supply stayed flat, there would be a continuously smaller money supply for the goods and services produced, making forward growth slow down due to money’s scarcity. Therefore, to avoid such natural slowdown, central banks issue money to fill in this gap. Economics are much more complex, but I wanted to transmit the essence here.

Visa got itself to be in a place of acting in favor of the economy and people’s inclusion, which in turn fuels Visa’s business. I’d expect Visa to continue benefiting in the foreseeable future from such flywheel and, its leading position should allow the company to capture a major part of the markets it creates and from overall economic growth as well.

At the same time, the sole factor of countries issuing money to not let economies slow down their growth, benefit the payments industry as a whole. Being electronic payments the ‘easiest’ method in which people can make payments, they should continue to attract most of the extra demand generated by future ‘extra’ money.

Management

Alfred Kelly is the man leading Visa. He worked as the President and Head of Global Consumer Group at American Express for 23 years, from 1987 to 2010. After leaving the company, he performed as the CEO of NY Super Bowl Host Committee for a few years and as the CEO of Intersection Co in 2016. In parallel to these activities, Kelly joined Visa’s board in 2014 as an independent director. In late 2016, Alfred was named Visa’s CEO and continues in that role.

Glassdoor offers some insights as to how is Alfred’s image indoors. There are over 6 thousand reviews and, as usual, the larger the number, the more ‘truthful’ the rating becomes. His approval is quite high given how large the company is, though not spectacular.

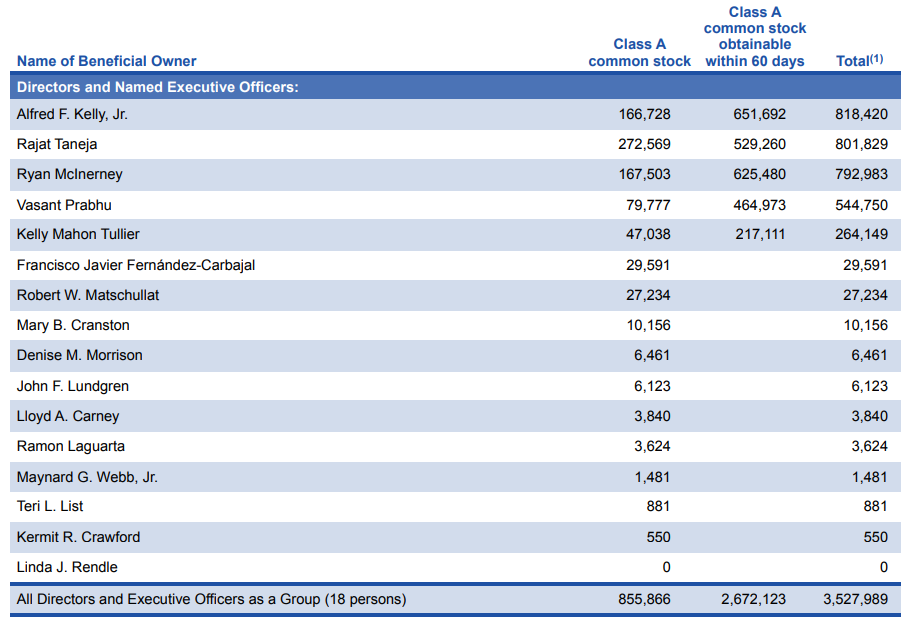

The image above illustrates the amount of stock each of the top managers have. The sum of all owned stocks plus the obtainable within 60 days accounts for 3.5M, equating for 830M dollars at Visa’s price of $230 per share. Less than 1%. Not much skin in the game in relative terms, but in absolute terms, that’s a big number.

MOAT

As stated, Visa is the facilitator of VisaNet and all services provided are built around that. In consequence, to analyze the main long-durable competitive advantage Visa has, we have to look at VisaNet.

The most developed and mature MOAT the company has is its Network Effects. They began acquiring clients and platform users since the 70s, turning VisaNet into the most demanded infrastructure for processing digital payments. In consequence, merchants and banks, almost without a choice, have to implement payment solutions leveraging the Visa Network because, if not, they would basically lose clients. As of today, VisaNet has got extremely intricated on 80% of the world’s economy. I reiterate, it is not an option to not utilize it if you are a merchant or a bank. This MOAT seems to be one of the widest out there.

Visa has been around for over 60 years now and it has made a complete name of itself. Perhaps not at the level of Microsoft Office or Google, but Visa must be at the top 10 most known technological tools at a worldwide basis. I’m talking the name here, not the offerings. Many people see their debit/credit cards with the name ‘Visa’ on them, but not all of them now it’s not Visa who issues the card. Nevertheless, the brand awareness it has created cannot be ignored, and I’d assume they have a quite heavy Brand Value mark.

Additionally, this can be seen through consumers’ lenses or through other participants. There may be not a single merchant or bank who actually distrust the service Visa provides, further strengthening the company’s Brand Value.

I’ve read people claiming Visa benefits from high switching costs and a low-cost producer advantage given the infrastructure it has developed. However, this is my view on both regards:

Given the number of players and technologies that have arisen and that get rapid and wide adoption, I wouldn’t say Visa benefits from high switching costs.

I agree at some point because the developed network allows Visa to process payments faster and more efficiently than competition, as well as covering more territory. However, there is not an immense gap in costs, and technologies like Bitcoin’s Lightning Network are presenting competition in all fronts.

Lastly, the long-durable competitive advantage Visa has been able to build over the past half a century is further strengthened by a very tall barrier:

“If you wanted to build your own payments network to compete with Visa, you’d need to win over the issuing banks. Of course, you won’t get the issuers if you don’t have merchants to accept your card and you won’t get the merchants unless you have the issuers’ card customers, who want to know that the card is accepted nearly everywhere...and, critically, you won’t get anyone unless you can ensure security, which itself depends on the insights garnered from the 100bn+ of transactions these two networks process every year. Every time you swipe your card, Visa evaluates over 500 different data points to determine fraud risk, calculates a risk score, and sends that score to the issuer to approve the transaction.all in a fraction of a second. Clearly, this is a tough chicken/egg nut to crack.” Expanding the Rails, Part 2

Competitive Positioning

The competitive landscape in the digital payments space is quite inclined to the two biggest players, up to the point this market could be categorized as a Duopoly (nothing new). The reason for this is because the sum of both companies controls over 80% (roughly speaking, hard to find Asia numbers) of the total volume processed, but that doesn’t mean there are no other significant players. American Express did over 1.5 trillion dollars in 2022, which is an immense number, in absolute terms, though a 10% of Visa’s volume.

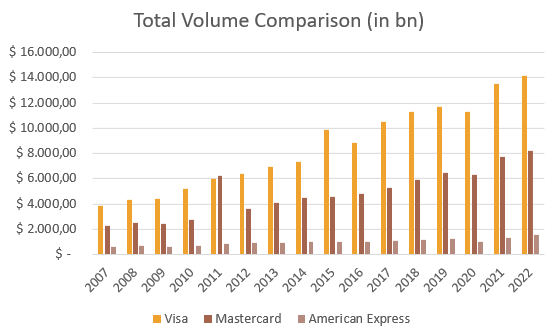

The following chart displays total volume growth for each of the 3 main players the sector has; Visa, Mastercard and American Express. Over this period, Visa outgrew its competition by a wide margin:

It achieved a 9.1% CAGR vs the 8.9% by Mastercard and the 6% by American Express.

Visa captured 10.3 extra trillion dollars in total volume, while Mastercard increased theirs by 5.9tn and American Express 904bn.

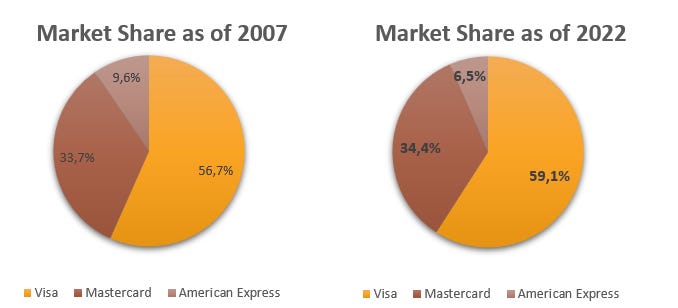

The three aforementioned competitors make up for over 80% of the digital payments industry. The following chart is based upon the controlled market by these 3, but keep in mind there’s a total 10-20% that’s not theirs.

Since 2007, market share did not change that much. The main difference is American Express lost market share to Visa and Mastercard, being Visa the one able to benefit more from this. For the past 15 years, the space has been almost completely dominated by Visa.

The second variable from which we could analyze competition is the total transactions performed by each network. The following image displays such variable for the previously selected timeframe (starting in 2007, when Visa went public).

Even though the chart looks very similar to the one presented in total volume, there’s a difference. On this occasion, Mastercard slightly outgrew Visa, exhibiting a 12.2% CAGR while Visa achieved 11.6%. It is worth mentioning Visa began the period from double the base of MA, but still. In nominal terms, Visa was able to process an additional 208bn transactions than it had in 2007, while Mastercard an extra 124bn.

The last front we’ll be looking at is the total cards each company has in circulation and how has it grown over the last decade and a half.

Similarly to the last comparison, Mastercard also outgrew Visa when it comes to total cards. MA grew its total cards in circulation from 916M in 2007 to 2,731M in 2022, at a 7.6% CAGR. On the other hand, Visa’s total cards went from 1,592M to 4,100, growing at a 6.5% CAGR. Again, Visa was able to make financial institutions issue more of their cards in nominal terms than Mastercard, but the bigger base at which it began made it quite difficult to compete in the percentage growth realm.

The Difference

There are two things we must cover here. Firstly, a distinction with Apple Pay and Google Pay, which are commonly mistaken as competitors. Same though not that clear with Paypal.

Paypal. While Paypal is an online service that secures virtual payments using end-to-end encryption, Visa is a card network that facilitates transactions by connecting consumers, banks and merchants.

Apple Pay. Apple Pay is a mobile payment and digital wallet service that allows users to make purchases with their Apple devices. In other words, Visa is the network that facilitates transactions, while Apple Pay is a specific service that utilizes Visa’s or other network to enable mobile payments.

Google Pay. Same as Apple Pay. It’s a technology made to purchase things. It outsources payments processing to networks such as VisaNet.

These are easier to distinguish than the differences with companies like Mastercard or American Express, both of which belong to the more closer circle in terms of offerings.

Mastercard. Visa and Mastercard basically serve the same purpose, but there are some differences in acceptance, geographical revenue sources and the processing fees structure.

American Express. Similarly as with Mastercard, the differences are, beyond the overall size, at a more narrow level, such as the processing fee structure.

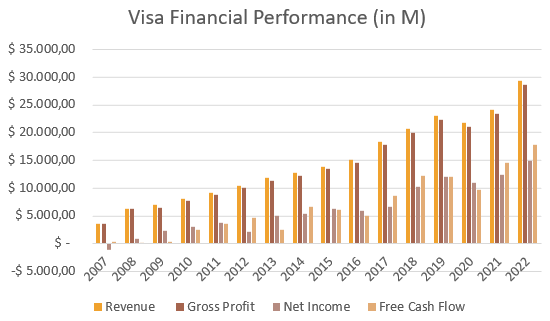

Financial Soundness

Since going public, Visa has been consistently increasing its revenue at quite a fast pace, accompanied with a higher margin efficiency. During the 15yr period:

Revenue grew at a 15% CAGR from 3,590M to 29,310M in 2022 (keep in mind Visa reports its Net Revenues, which means its their revenues after client incentives)

Gross profit increased from 3,590M to 28,567M, growing at a 14.8% CAGR

Net income at the beginning of the period was -1,076M and at the end, 14,957M. Since 2008, it has grown at a 28% CAGR

FCF has gone from 345M in 2007 to 17,879M in 2022, exhibiting a 30.1% CAGR. FCF/Share currently stands at 8.65 and it has grown at a 21.8% CAGR since 2007 or at 46.8% since 2008

Given the higher performance net income, free cash flow and operating income have had, it’s easy to conclude that margins have expanded by at least a fair amount. The following chart computes Visa’s margins at the different income statement levels.

It seems like a bug, but Visa’s gross profit margin is literally almost 100% and has consistently stayed close to that number for the past decades. Going down through the income statements, margins have only improved for Visa since going public. More specifically

Operating margin has increased 2.430bps since 2008, going from 43.1% to 67.4%.

Net margin has gone from 12.8% in 2008 to 51% in 2022, expanding 3.820bps.

FCF margin has increased a total of 5.910bps since 2008, now standing at 61%.

The logical requirement for bottom line margins to improve is for revenue to increase at a faster pace than costs, which is what happened across this timespan. Visa actually reports its operating costs in a very well fragmented way. However, it is broken so much down to the point that if I include all variables, the chart turns unintelligible. With the purpose of clarity, I selected what I considered to be the most relevant expenses. For reference, here’s what Visa reports:

From the operating expenses, I chose to go with Personnel, Marketing and Network. Upon different fronts, I also decided to include the cost gross revenues have, Client Incentives (CI in the chart); and, lastly, Capital Expenditure. Keep in mind the operating expenses and CapEx are in terms of Net Revenues, while Client Incentives are in terms of total revenue.

The trend for operating expenses is extremely clear, also explaining the rise in operating margin:

Expenses in Personnel have declined 400bps as a % of net revenues

Marketing expenses as a % of net revenues have declined 11.7pp over the last 15 years

Network and Processing expenses have declined 290bps since 2008

In the same line as operating, CapEx has gone from 6.6% of net revenues in 2008 to 3.3% in 2022. The only expense, which is taken out of the equation by Visa very up on the income statement, that has trended upwards is Client Incentives. During the last 14 years, CI has increased from being 15.6% of total revenue to 26% in 2022, perhaps raising some concerns on competition.

One fabulous thing Visa has is it does not spend a single dollar in R&D, which is absolutely impressive given their continued leading position in this market.

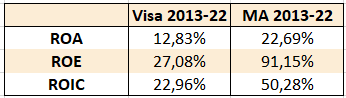

Capital Allocation Skills

A case could be made where some of the charts illustrated above speak of the discipline in which management allocates capital at an operating level. For further breakdown of their actual skill, we’ll recur to the usual standards for measurement.

The three financial metrics upon capital allocations skills can be examined have been trending upwards, with no signal of peaking yet. In the period 2008-2022:

Return on Assets has gone from 8.58% to 14.67%, with an average of 11.5%.

Return on Equity has climbed from 7.78% in 2008 to 40.88% in 2022, averaging 21.6% per year.

Return on Invested Capital has increased from 11.03% to 29.1%, showing an average of 20.5%.

In absolute terms, all three returns on capital are very high. However, they are not as high as they could be given the industry Visa’s in. Here’s a comparison for the last decade between Visa and Mastercard (average). Worth keeping it in mind.

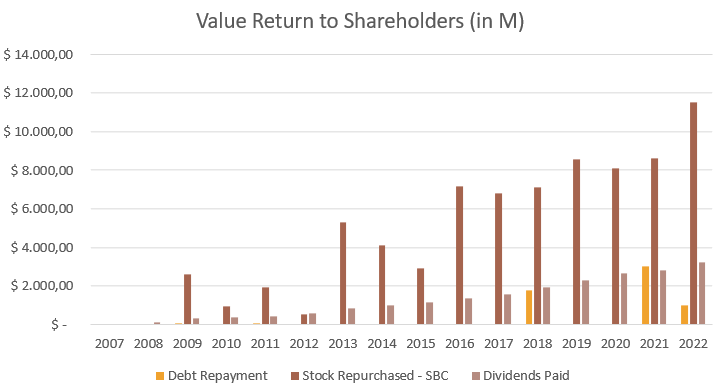

Value Return to Shareholders

Almost since going public, Visa has continuously returned value to its shareholders, mainly in the form of stock repurchases. The following chart computes the 3 principal activities in which companies can do this task.

Until 2016, the company had almost no issued debt. After issuing, Visa repaid a total of 5.75bn of debt

Stock repurchases have been consistent during this decade and a half while SBC kept low, making Visa’s total shares outstanding decline by more than 30%

Dividends paid have been yearly increasing as well with now the company paying over 3bn in dividends to shareholders.

Finally, as of the last reported results, 1Q FY’23, Visa held a total of 20.4bn in debt while having 16.1bn in cash and equivalents, making the overall business have a net debt position of 4.3bn. Definitely not a splendid balance sheet though the incredibly high profitability levels Visa has makes it extremely anti fragile. A single quarter’s FCF can almost cover the whole gap between debt and cash.

Risks

Competition. The digital payments industry is highly disruptible, as we’ve seen with blockchain and tech-enabled companies. At the same time, Mastercard continues to be a heavy weight in the space.

Regulations that could affect the payments industry as a whole

Cyber attacks have been rising very rapidly over the past years and Visa is surely in the spot of attracting them.

Personal Commentary

Selecting between Visa and Mastercard is not a crystal clear decision. I might write an article solely dedicated to diving deeper into the differences. Besides that, I really enjoyed putting this article together. If you enjoyed reading it, feel free to subscribe below, I’ll try to bring 1 research article per month at least.

Disclaimer: This is not financial advice.

Amazing work!

Impressive work, you can see the hours you've put into it