“Our passion is to create a better world by making electronics more affordable through semiconductors.”

Business Overview

Texas Instruments was founded by Cecil.H Green in 1930 as Geophysical Service Incorporated. In 1941, the company was bought by three people and, during World War II, it supplied electronic equipment for the US Navy and Army signal Corps. It continued producing electronic equipment when in 1951, it changed its name to Texas Instruments

Texas Instruments designs and makes semiconductors that then sells to electronics designers and manufacturers all over the world. Semiconductors are electronic components that serve as the building blocks inside modern electronic systems and equipment. TXN counts with a portfolio of about 80.000 products that are integral to almost every type of electronic equipment. The utility of such products is very diverse, they are used to:

Converting and amplifying signals

Interfacing with other devices

Managing and distributing power

Processing data

Canceling noise

Improving signal resolution

Texas Instruments agglomerates this broad portfolio of products into three segments, upon which then reports results. Each of these segments include products that are similar in design, development and requirements.

Analog Semiconductors change real-world signals like sound/temperature by conditioning them, amplifying them and converting them into digital data so it can be then processed by other semiconductors. They are also used to manage power in all electronic equipment by converting, distributing, storing and measuring electrical energy.

Embedded Processing products are the digital brain of many types of electronic equipment. They are designed to handle specific tasks and can be optimized for various combinations of performance, power and cost. The diversity of TI’s products goes from simple and low-cost like electric toothbrushes to highly complex devices like motor controls.

Other includes the remaining activities of the business that do not meet the requirements to be reportable individually nor can be aggregated with the other segments.

Source: TXN Investor Overview

The vast majority of revenue comes from Analog Semiconductors, representing a high 77% while 17% comes from Embedded Processes and the remaining from Other. These products are sold to over 100.000 customers with little concentration, having more than 40% of revenue coming from non-top 100 customers.

Chips are used in all sort of technological devices and the vast portfolio of products TXN has, makes the company sell to a wide variety of clients from a broad variety of sectors.

Source: TXN Investor Overview

Each of those industries are composed by many sectors. Industrial represents 13 different sectors, from Factory Automation & Control to Medical, Grid Infrastructure, Building Automation and more. Automotive represents 5 different sectors, Personal electronics 10 sectors, Communication Equipment 4 sectors and Enterprise Systems 3 sectors.

Industry

Technology has been responsible for most of the human progress of the past centuries. Technology needs semiconductors in order to function and they will continue to do so. With evolution, new technologies arises and these new technologies need a higher input of power to work. Among this there’s AI, Automation, Robotics, 5G, Edge Computing, Cloud Computing, EVs, VR.

All of them need chips and higher throughput, hence why the Semiconductor Industry is estimated to grow from 573bn today, to 1.3tn in 2029, exhibiting a compound annual growth rate of 12.2%.

However, the semiconductor industry has been historically characterized for its cyclicality. It has periods of very tight supply caused by an increase in demand or insufficient manufacturing capacity, followed by periods of surplus inventory caused by weakening demand or excess manufacturing capacity. These cycles are aggravated by the significant time and money required to build and maintain semiconductor manufacturing facilities. Therefore, even though the estimated CAGR for the industry may be of 12% until 2029, it will not be a linear growth.

Regarding the industry, Texas Instruments mentions two additional factors. Firstly, the significance of global competition from dozens of large and small companies making the industry a very difficult to continue to thrive in. Secondly, it mentions their revenue is subject to seasonal variation since, historically, its sequential growth rates tend to be weaker in the first and fourth quarters compared to the other two.

Thesis

Semiconductors will be a major part of technological progress in all fields aforementioned. Texas Instruments seem to be in a very well-suited position to capture part of that growth. Given its broad portfolio of products, it shouldn’t matter which technological trend drives the most growth, TXN should cover the sector and benefit from it.

Although to analyze a company’s thesis I generally focus on inherent fundamentals to the business and sector, I’ll make an exception with Texas Instruments. Knowing how to use capital effectively can play a major role on a company’s future and save it in decisive moments. Management at TXN excels at it, hence why it will provide another pillar to the thesis.

Management

Texas Instruments is currently led by Richard Templeton. He joined the company after graduating from a BSc in electrical engineering in 1980. In 1996 he began leading the semiconductor business, then served as COO from 2000-2004. In May of 2004, he was named CEO and, in April 2008, Richard joined Texas Instruments Board.

According to Glassdoor’s 4.600 reviews, Richard holds a very high approval rate, at 94%. Employees at Texas Instruments seem to be satisfied with the values the company professes as well as working there, TXN getting a high 4.2 stars.

Source: Glassdoor

Texas Instruments is ranked as one of the Best Places to Work according to Glassdoor’s database.

Source: Glassdoor

As illustrated in the image below, the board of directors own less than 1% of TXN’s shares. Texas Instruments is obviously not founder led and its management does not own a huge stake of the company. These characteristics are not ideal, but the company’s excellent culture and Richard’s trajectory at Texas Instruments are highly positive points.

Source: DEF 14A SEC filing

Another important and peculiar thing to mention regarding management is their Capital Allocation Skills, their discipline to do so and their mindset. Some quotes

“We will act like owners who will own the company for decades”

“Our objective and the best metric to measure progress and generate long-term value for owners is the growth of free cash flow per share”

These two quotes are a big deal. The first one clearly states they’ll operate with a long-term vision while the second one states their absolute focus in growing “Free Cash Flow per Share.” This implies maximizing the efficiency at which the company runs on a daily basis while being extremely disciplined on R&D and every sort of operating cost, which shows in margins. Spending is always done thinking how will it return more cash to owners.

Source: TXN Investor Overview

TI has spent 79bn dollars over the past decade among R&D, CapEx, Inventory, Share Buyback and dividends. R&D meant the highest spending which was utilized to drive organic growth for the company, which went from 12.8bn revenue in 2012 to 18.34bn in 2021.

Moat

Texas Instruments competitive position is strengthened by various pillars.

Source: TXN

The first one is its manufacturing capacity and distribution channel. Given its size and that it owns its factories, the company has more control over the supply chain to support customers and can manufacture its product more cost-effectively than its peers. Having the majority of the manufacturing process in-house also allows them to produce even in turbulent periods, since they depend mostly on themselves. At the same time, this mature distribution network allows TI to provide a more reliable service to its customers and at lower costs than its peers.

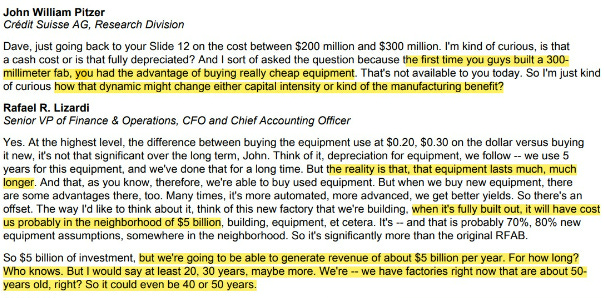

Adding to its low-cost manufacturing process, TI built the first 300mm wafer fab for analog manufacturing in 2010. Over the decade, Texas Instruments focused on expanding their 300mm output and this sets them on a very different level of profitability against most competitors.

Source: TXN

With a lower force, TXN also benefits from high switching costs, mainly in the embedded processes. It is very common that customers invest their own R&D to write software that operates on TXN’s products and, once this is done, the most viable choice for a company is to continue operating with Texas Instruments products rather than investing and writing new software.

Lastly but also contributing to Texas Instruments competitive position, its Patents Portfolio. As of 2016, TXN had a portfolio of about 45 thousand patents. I was not able to find an actual number for 2022 but estimates vary between 50k and 80k. This intangible moat makes entering each separated sector more difficult for competitors.

Financial Soundness

I know it’s visually kind of choppy but if I intend to agglomerate the whole decade in a single picture, quality turns 0 and numbers unintelligible.

Source: Koyfin

Source: Koyfin

Summarizing:

Self-made

Texas Instruments most notable evolution over this period has been its abnormally high margin expansion, which could be attributed to different reasons.

Firstly, the aforementioned benefit of being a large manufacturer and having a well built distribution network allows the company to continually decrease the costs per product sold and to keep competitors away.

The second main reason may be based on a decision Texas Instruments made back in 2012, where it said it would shift its wireless investment focus from products like smartphones to a broader market including industrial clients like carmakers where it was hoping for a more profitable and stable business. Here’s how things changed since:

Source: 3Q 2012 and 2Q 2022 TXN Results

Going back to a previously mentioned point about management’s disciplined and great capital allocation skills, the different financial metrics measuring this seem to favor management. Return on Equity has been at a high average of 38%, Return on Assets at 17% and Return on Invested Capital at 32%. These 3 financial metrics express how well or how efficiently is capital being employed.

Texas Instruments has been at a mature state for decades now and, aggregating this to management’s focus of returning capital to shareholders, has made the company return cash for many years. In the following period, Dividends grew at a 22.43% compound annual growth rate and shares outstanding have been reduced by 47%. At the moment, Texas Instruments has an ongoing and unused repurchase program of 23bn, about 15% of TXN’s current market cap.

Source: Koyfin

One thing to keep in mind is Texas Instruments is making CapEx investments to strengthen their manufacture and technological competitive advantage. This will further lower the manufacturing costs as well as it will increase TXN’s control over their supply chain. Some quotes by management on the subject:

“We have 300mm capacity coming online in 2022-23.”

“We have a 300mm roadmap to support growth from 2025-35.”

“Customers are excited that capacity investments in (…) will support their growth in the decades ahead.”

The last one on how these investments make so much sense over the long term and the lifetime value they’ll be able to capture from each factory.

Lastly, TI has 7.2bn in total debt while it has 8.4bn in total cash and short-term investments, making debt easily cancellable. The company is extremely profitable as well, having produced about 6bn in free cash flow over the last twelve months, making it in a non-fragile financial position.

Risks

Geopolitical. Occident has been pushing measure trying to limit the amount of chip equipment sold to China. China-based customers represent 25% of TXN revenue.

Innovation. Almost every field now is subject to technological innovation and so is the semiconductor industry.

Cybersecurity Breaches.

Thanks for reading From 0 to 1 in the Stock Market! Subscribe for free to receive new posts.