Mission

“Tesla’s mission is to accelerate the world’s transition to sustainable energy”

Business Overview

Tesla was founded in 2003 as Tesla Motors by Martin Eberhard and Marc Tarpenning. In early 2004, they were looking for funding and connected with Elon Musk, who contributed over $6.5M to the Series A. Since then, Elon became chairman of the board of directors, taking a step towards administration. In late 2009, a lawsuit settlement agreed to by Martin and Tesla, allowed the five most representative men to call themselves Co-Founders.

The company first started as an Electric Vehicles manufacturer but quickly spined out of it to create a suit of different products. They report them as two different segments, automotive and energy generation & storage. However, the vast majority of Tesla’s revenue comes from the EV sector. Among the products the company has, we can find:

The automotive segment includes the design, development, manufacturing, sales and leasing of electric vehicles as well as sales of automotive regulatory credits. Tesla’s vehicle offerings include:

- Model 3 is a four-door mid-size sedan

- Model Y is a compact sport utility vehicle (“SUV”) built on the Model 3 platform with seating for up to seven adults.

- Model S is a four-door full-size sedan

- Model X s a mid-size SUV with seating for up to seven adults

The company is working on future EV offerings, such as:

- Tesla Semi

- Cybertruck

- Tesla Roadster

The energy generation and storage segment includes the design, manufacture, installation, sales and leasing of solar energy generation and energy storage products and related services and sales of solar energy systems incentives.

- Powerwall and Megapack are their lithium battery energy storage products. Powerwall is for small demand energy storage (houses), whereas Megapack is for industrial/commercial purposes.

- Among their Solar energy generation offerings they have retrofit solar energy systems and their Solar Roof.

A particular and remarkable aspect of Tesla’s business model is that it is vertically integrated. The company has designed and manufacture almost every component the car needs to properly function, as well as the energy and the software offerings. This is a very peculiar characteristic in the automotive market and makes Tesla more resilient to supply chain issues.

Almost the completeness of Tesla’s business model is currently about their electric vehicles. Hence, a key metric to evaluate performance is the cars delivered. Since 2012, deliveries grew from 2.600 to 908k in the first three quarters of 2022.

The next two charts are a breakdown of Tesla’s revenue. As aforementioned, most of it comes from the automotive sector.

Absolutely in parallel, Tesla counts with multiple initiatives to incentive/accelerate Electric Vehicle’s usage and adoption. They are developing what they call customer-facing infrastructure through a global network of:

Supercharger Stations: Industrial grade, high-speed vehicle chargers. A particular thing about them is they commonly employ their own renewable energy systems, both of generation and storage.

Vehicle Service Centers.

Mobile Service Technicians who perform work remotely at customers’ homes or other locations.

Destination Chargers: Tesla Wall Connectors for concurred spaces and single-family homeowners.

The last part composing Tesla’s business models is its Car-related in app upgrades and/or additional services (FSD, warranties, insurance, vehicle service, leasing/loans), as well as the multiple vertical initiatives it has, like apparel, lifestyle. To avoid misunderstandings, this last part generates a very small fraction of the company’s revenue, remaining secondary.

The most relevant among all is Full Self-Driving. FSD will be a software offering that will allow for autonomous driving. These enhancement has been on beta since October 2020, but is expected to be generally and fully released on Q4 of 2022. FSD users grew from a few thousands when it was launched to about 100k on September 2022.

Industry

Tesla belongs mainly to the electric vehicle industry, but it has several products over parallel sectors. Among them, the most remarkable are renewable energy solutions, storage and generation. At the same time, the company has been building their Full Self Driving capabilities for years now and there’s something Elon said on an interview that struck me (I’m paraphrasing):

“There was some point in the road where we could not advance and that’s when I figured out that to solve FSD we had to solve AI”

This implies that once the full self-driving software and the autonomous driving solutions are out there and sharpened, it will most likely mean that the team at Tesla got to solve AI. When this happens, Tesla could calmly start releasing AI products (like Optimus, the robot presented in last Tesla’s AI Day). This opens up another potential industry to which Tesla could have exposure to. For those that do not follow Tesla that close, Optimus is a humanoid robot (prototype) which should leverage AI to solve real problems, firstly oriented at household issues as far as I know. Tesla’s plan is to massively produce these products and deliver them at scale.

Forecasts should always be taken with a grain of salt, but the Total Addressable Market for EVs is expected to grow from 287bn in 2021 to 1.3tn in 2028, exhibiting a 24% CAGR.

It is worth mentioning that the automotive industry has been historically cyclical. This has not yet affected the EV space given the exaggerated tailwinds Electric Vehicles have, but this resilience to downturn periods could not last forever and is something to watch out for. As known, cyclicality makes growth be non-linear, even though high growth rates could be achieved in the long term.

On the other hand, the renewable energy industry is expected to grow at averagely high rates and so is the AI space, both markets expected to be worth in the hundreds of billions of dollars at least.

According to Precedence Research, the global renewable energy market size is expected to be worth around the 1.9tn dollars in 2030, exhibiting a CAGR of about 8.6%. Battery energy storage solutions are expected to grow from a 10bn market in 2022, to a 31bn one in 2030. This would imply for it to achieve a 16% compound annual growth rate. Tesla’s position in both market is not a leading one, yet could be benefited from the sector’s growth.

Thesis

Tesla’s thesis is quite a complex web.

The first and most important one is its position in the Electric Vehicles space. Tesla is currently leading the trend and continues to grab market share from its peers. Its scale should allow it to persist in this trajectory and be one of, if not the most, benefited company from this immense and rapidly growing market.

Secondly, autonomy is a pillar for next decade’s transportation thesis and could allow Tesla to incorporate a new unprecedented revenue stream, but which appears could be a fantastic addition to the company’s business model, fundamentally and financially speaking.

“Autonomy is an insanely fundamental breakthrough and nobody is anywhere close to Tesla for solving generalized self-driving vehicles, nobody is even close. With self-driving, the car becomes ‘roughly 5x more useful but it costs the same to build’”

I’m generally against including such thing as ‘innovation’ to a business thesis, yet in this occasion, innovation is so deeply rooted to Tesla and Elon’s existence it can’t be ignored. This is a company so sure of its future innovation that since 2019, grants away patents for free to competitors, under the premise that other companies will never catch up Tesla since it’s always working in the next improvement. In line with this:

“We have a massive amount of internal manufacturing technology that we built ourselves.... It's like, okay, what are the things we want to make, design a machine that will make that thing, then we make the machine."

Upon the previous two legs surges the next one, AI. Artificial Intelligence makes a major part of Tesla’s future thesis. Even though EV already makes a very strong one for a single company, AI cannot be omitted either. As mentioned in the previous section, if Tesla gets to solve AI and is a first mover in these kind of products, new revenue streams should open up and they should be ones with very large TAMs, estimated in the trillions. But not only this, if it does it so soon, peers could never really catch up given the inherent competitive advantage underlying in this technology.

The last source fueling Tesla’s thesis is Renewable Energy. This sector’s generation and storage solutions are expected to grab a ton of market share in the future. The whole world has acknowledged in the past decade they should adopt renewable energy and every piece of the puzzle is ensuring it becomes a major component of total production and storage. Tesla owns a decent portfolio of products, which is expected to expand as well, and could benefit from the massive tailwinds this sector has for the next couple of decades.

Management

Most likely known by everyone, Elon Musk currently leads Tesla. Even though he was not the literal founder of the company, he joined so early and being a technical co-founder makes a very valid case to call Tesla a founder led company. Foremost, he’s envisioned the company’s future for the past decades and is still doing so for the coming ones. This man is objectively one of the 21st century greatest visionaries and plans to continue running Tesla for his foreseeable future.

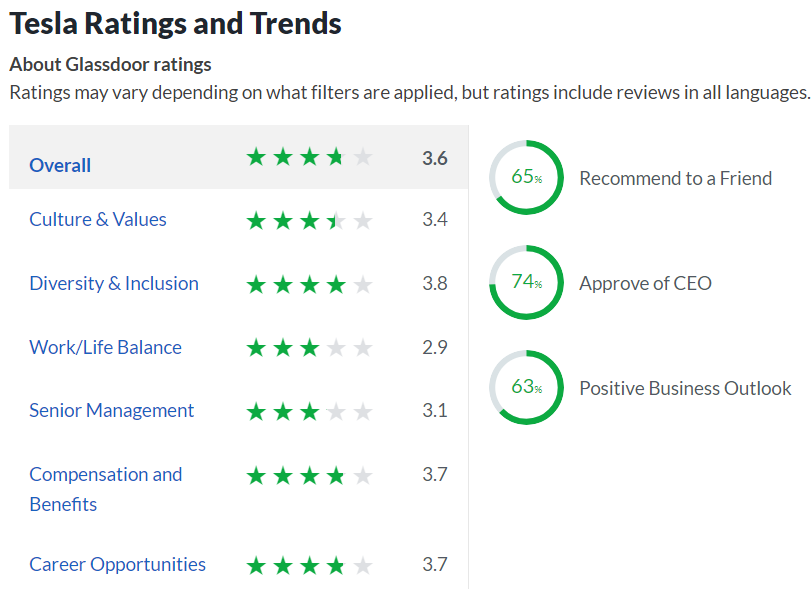

However, overall Tesla ratings at Glassdoor are not that great, or at least not what one would think when working for such a person. According to the written reviews, it may have a lot to do with work-life balance. Among the most quoted issues employees encountered when working for this company was “long hours” and “no work-life balance.” In general terms, culture and acceptance within Tesla is fine, but not fantastic as companies we’ve previously covered.

Watching it from another perspective, Tesla has always appealed the engineering community for the immensity and attractiveness of the problem it’s solving. According to 2021 Universum survey, Tesla ranks 3rd as top businesses to work for, 2nd as most desired place to work for engineers and 4th for computer science people. The conjecture one could take out of this is Tesla pushes people to the limit, but they choose to work there because they may feel they are doing something actually important for humankind.

The last aspect to evaluate on management is the skin in the game they have. At the moment, management owns about 9% of Tesla, with Elon owning 8.5%, which would be around 52bn dollars. I wasn’t able to find the answer but I believe Elon would be the person with the largest stake in a single company.

Moat

The first two competitive advantages Tesla has, derive directly from its current business model. The company is worldwide known for not spending a single dollar in marketing, yet it got to create such an awareness for its brand that everyone knows it. Consequently, according to Statista, the current brand value of Tesla is estimated to be worth 75bn dollars, up from 42bn dollars last year. Pairing both arguments, a common conclusion to arrive to is Tesla benefits from a strong Brand Value MOAT.

The second one Tesla has is low-cost production, associated with the scale achieved and the efficiency in which they build their Gigafactories. In 2017, making each Tesla costed around 84k dollars. In September 2022, Dan Mihalascu shared that the current cost per car is around the 36k dollars. Big proof of Tesla’s operating leverage, coming from its low-cost production competitive advantage. Nowadays, production capacity stands this way:

So about 2M in production capacity, which the company plans to continue expanding, reiterating several times their 50% annual growth in deliveries for the coming future.

The following is an estimate of the net income per car in the 3Q22’:

Lets use an example to showcase this moat in practice. Tesla’s cost per Gigafactory vary with the production capacity each has. For the illustration, we’ll utilize Texas Gigafactory, which costed around 1.1bn dollars to construct (according to multiple sources, non of them is Tesla itself). To calculate the return on this investment, we’ll dive into how much does Tesla makes per car delivery. For it, I used the disclosed number for automotive revenues and the disclosed number for the cost of those revenues. Thereafter, to calculate the floor for how much is Tesla making in net income per delivery, I assigned the complete operating costs, taxes and other expenses to this segment.

It’s current minimum income per car delivered is estimated to be around 7.500 and Texas Gigafactory capacity is estimated to be 250k cars per year. So, we get that for each factory of these characteristics Tesla builds, its return of investment is of 170% per year:

This competitive advantage is further protected by two barriers:

High entry cost. Entering the automotive manufacturing business has a huge first fixed cost, which keeps competitors away. At the same time, it’s a sector that has historically had very low margins (Tesla is changing that appraisal in the EV space), so it was not even worth entering it.

Complexity. It is not only about the cost of the facilities, but the difficulty on building them as well. This extract perfectly explains it:

"This makes it quite difficult to copy Tesla... because you can't do catalog engineering. You can't just [say] I’ll pick up the supplier catalog, I’ll get one of those." When it comes to what Tesla does, "there is no catalog. Look at it. So we made the machine, that made the machine that made the machine," says Musk.

In addition to the aforementioned competitive advantages Tesla has as a business, when full self-driving is completely achieved, it will unlock new moats. First and foremost, Switching Costs will be as high as it gets, since Tesla will be the only offeror of such solution. Therefore, it will possess an authentic monopoly on it, making customers be ‘forced’ to using it since they have no other option to opt for.

The second one arises from the underlying technology in the Full Self Driving software, Network Effect. Artificial intelligence technologies characterizes themselves for getting better and better when fed with more data. FSD has been fed for the past two years with competition not even close of having a decent product. Consequently, once fully launched, full self driving will be exposed to tons and tons of data, which will increase the accuracy and further sharpen the software. This cycle will make Tesla’s offering the best worldwide and if competition doesn’t soon create a competing product, FSD could be the greatest autonomous driving offering. Finally, as Google has shown with Google Search, it is very difficult to displace a MOAT of this kind.

Andrej Karpathy, former AI director at Tesla, was on Lex Fridman’s podcast in September and mentioned some interesting things in this regard:

On the timeline to solve autonomous driving: “The problem with timeline is that no one has created self driving… no one has built autonomy, it’s not obvious”

“At least the team at Tesla, which is what I saw internally, is definitely on track to that [solving autonomous driving]”

Competitive Positioning

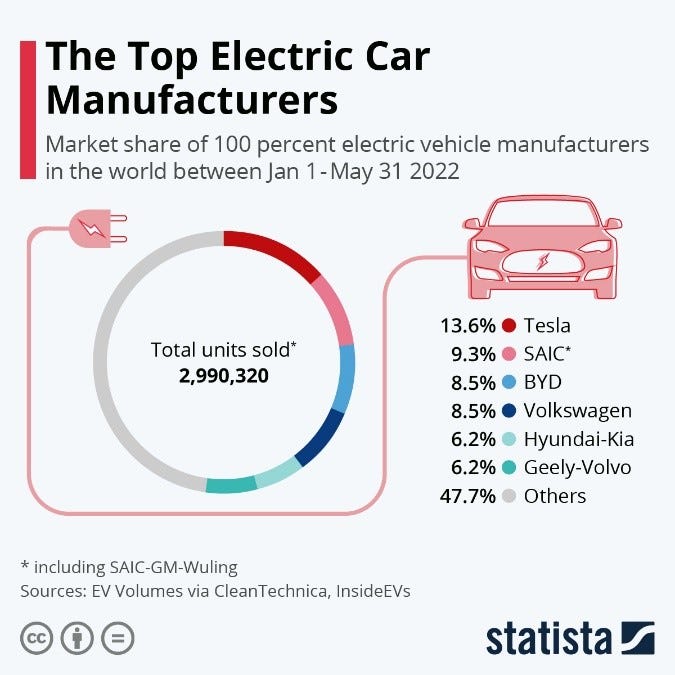

As of May 2022, Tesla was the company that sold the greatest number of cars among 100% EV manufacturers.

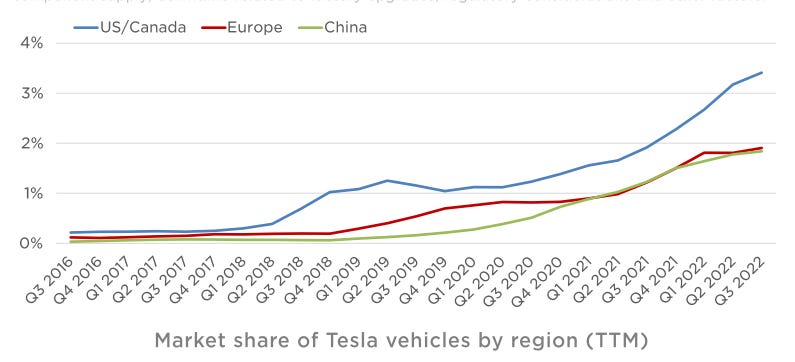

In terms of the automotive market, Tesla has been grabbing market share since 2016 and has never stopped doing so.

A financial comparison with big automotive companies:

Finally, Tesla differentiates from competitors because of its business model. The fact of the company being almost 100% vertically integrated makes it much more resilient to supply chain issues. This got to show during the past two years, where the world succumbed to material issues of this kind. During the first three quarters of 2022, Tesla delivered 908k vehicles, whereas on the four quarters of 2020 delivered 500k.

Financial Soundness

To analyze Tesla’s financial state, we’ll split it into three parts. The first one will be on historical growth as well as margins exhibited during the process. The second one will be on management’s discipline regarding capital allocation. Lastly, the third one will be on management’s capital allocation skill.

Charts won’t reveal 2010-13 period because they denaturalize them. That 3 year span had unbelievably negativemargins and revenue was so low that chart’s scales turn awkwardly unintelligible. From 2010-LTM (4Q’21+3Q’22) Tesla grew its revenue from 116M to 74.8bn dollars, exhibiting one of the highest ever achieved CAGRs, 73.6%.

The company has been immersed into hyper growth mode ever since inception until 2019, which gets to show when income is analyzed. Tesla lost money until then on a fcf and net income basis, but since 2019, margins drastically expanded. In 2019, gross profit margin standed at 16.5%; free cash flow margin at 3.9%; net income margin at -3.5%. However, in the last twelve months, the exhibited margins were 26.6%, 11.9% and 14.9% respectively. This gets to show more vividly Tesla’s operating leverage kicking in, as aforementioned.

To get a glance at management’s discipline when allocating capital, the most pragmatic approach is to analyze how have expenses been managed as the company grew larger. More so, in a growth company, it’s especially effective to compare expenses to the percentage of revenue they represent.

Since 2013, all three operating expenses have trended down when measured in this regard. General and Aministrative expenses began representing a 14% of total revenue and finalized at 6% over the last twelve months. Research and Development started being 12% of revenue in 2013 and ended at 4% in the LTM. Finally, Capital Expenditure has overall trended down, beginning at a 13% of revenue and ending at 9% of it.

One key thing to mention is that Tesla is an automotive company. This means that it needs manufacturing facilities to assemble the products made and it need to overspend (in CapEx) to expand its reach. That’s what makes Capital Expenditure vary so much over time and it should continue showing that volatility given the company’s future plans.

Capital allocation skills are usually measured by metrics such as Return on Equity, Return on Assets and Return on Invested Capital. Tesla has been historically not optimized to produce neither net income nor operating income, making these parameters unuseful. Since 2018, the company has somewhat stabilized financially, so the analysis will be made from that year forward. Caution is advised on conclusions given the short span of time evaluated.

Tesla getting more cost efficient in these past couple of years abruptly affected the perceived management’s capital allocation skills. The three metrics were negative in 2018 and, over the last twelve months, ROE was at 32%, ROA at 11.8% and ROIC 27%. Trend seems to still be upwards, even though the percentages reached are standardly high. Once operating leverage stops showing, they should all normalize and tend to their intrinsic values.

Risks

Key person risk. Elon has been leading the company since inception and has been the one who had and still has the vision for Tesla’s future.

Geopolitical. 25% of total revenue comes from China, which makes the company fairly exposed to this geopolitical risk.

Disruption. Tesla belongs to the frontier of innovation and companies of these characteristics are extremely fragile to innovation and disruption.

Competition. Even though Tesla has dominated the space, companies like BYD in China are really catching up and suppose a threat.

Personal commentary

Tesla is currently between hyper growth and stabilization, making it very particular to analyze in some regards. Most of the article is about 90% of Tesla’s current business, a future article could be a deeper dive into the remaining 10%. Lastly, beware of estimates. Anyway, hope you enjoyed it!

Disclaimer: This is NOT financial advice

Your article was a joy to read! I loved how you provided such a detailed analysis and made the topic so engaging. Thank you for taking the time to write it - it was truly appreciated!

Good read, I think another thing worth mentioning is Tesla’s sale of Carbon credits have been 5-10% of their quarterly profits this year. Tesla has warned that carbon credits will decline. That being said, their current level of growth is probably enough to offset this decline