This is the second (out of two) part of Microsoft’s research. In the previous part I covered, as thoroughly as I could, Microsoft’s offerings. Here’s it in case you want to check it out

Industry

Microsoft belongs to a set of different industries, all of which add to the addressable market the company has.

Firstly, one of the main pillars of the business is their Office 365 products. The underlying industries this suite of solutions represent are uniquely intentioned softwares. Its tools can be useful for administrative work, creative, collaborative, construction and design work. Statista offers a very comprehensive estimate breakdown of most industries to which Office 365 belongs. From 2022-2027, the sector is expected to achieve a CAGR of about 4-4.5%, showing signs of maturity.

At the same time, a case could also be made where some of these apps are meant to increase productivity and efficiency among employees. This characteristic can be highlighted on products like Teams, SharePoint, the different set of task & project management tools like the ones included in Dynamics 365. Particularly, through no-code developing solutions offered by Power Apps, productivity is meant to only increase. For example, Power BI allows for the automation of several previously manual efforts. This market is expected to grow at a CAGR of about 14.5% in the period 2020-28.

The second branch originated from Microsoft’s industry tree is, of course, Cloud Computing. This term is defined as anything that involves delivering hosted services over the internet. In it, and supported by the 40+ use cases Azure has, there’s computing power via Virtual Machines, Cloud Storage, Data Analytics powered by ML models, Automation, app development, and others. The Total Addressable Market for Cloud Computing is estimated to grow from 380bn in 2021 and around 500bn in 2022, to over 1.1-1.6 trillion dollars, depending on the forecast.

The following estimate is a more optimistic one, expecting the Cloud Computing market to exhibit a CAGR of 18%.

The Operating Systems market could be considered a mature market. It’s been around for more than 40 years and, as of this moment, there’s no apparent hard innovations that could be done to enhance the demand with added value, and therefore accelerate the OS market growth. According to Regional Research Reports, the global operating systems market is expected to grow from 43bn in 2021 to 57bn in 2030, exhibiting a CAGR of around 3.2%.

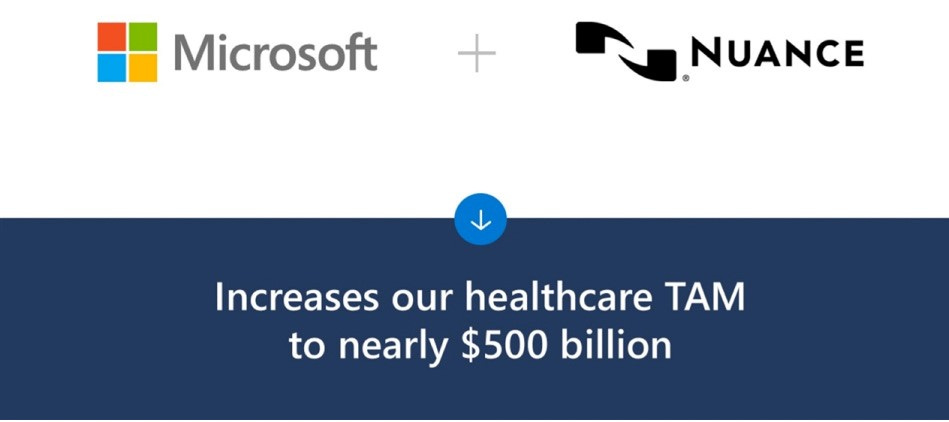

Microsoft has several AI components fueling its thesis, mostly within the Azure ecosystem, but it was further enhanced by their Nuance acquisition. Although it has some sort of full spectrum AI tailwinds, estimates to that market include all the verticals to which AI could be applied. In consequence, as a form of north star, lets utilize Microsoft’s estimate of how much does their Nuance acquisitions boosts their addressable market in the healthcare/AI space.

One of the more pronounced AI verticals Microsoft is exposed to is Conversational AI, through Nuance. This space is expected to grow at a 20% CAGR until 2030, from 6/7bn today, to 30/40bn.

LinkedIn is a very peculiar business unit because its revenues streams are very versatile. It sells business solutions, subscriptions to professionals and obtains almost 40% of its revenue from advertisements. This gives LinkedIn exposure to different industries, which makes its future addressable market a tricky to estimate. As of 2016, Microsoft estimated LinkedIn’s TAM to be around 115bn, which’s figure has not been updated. In its last Fiscal Year, LinkedIn made over 13bn in revenue, meaning it captured around 10% of its 2016 estimated TAM.

The last major industry to which Microsoft belongs is gaming. According to Grand View Research, this market was valued at 195bn in 2021 and it’s expected to grow at a 12.9% CAGR until 2030, making the global video game market size be 580bn. Cloud Gaming derives directly from the overall gaming sector and it’s expected to grow extremely fast.

Thesis

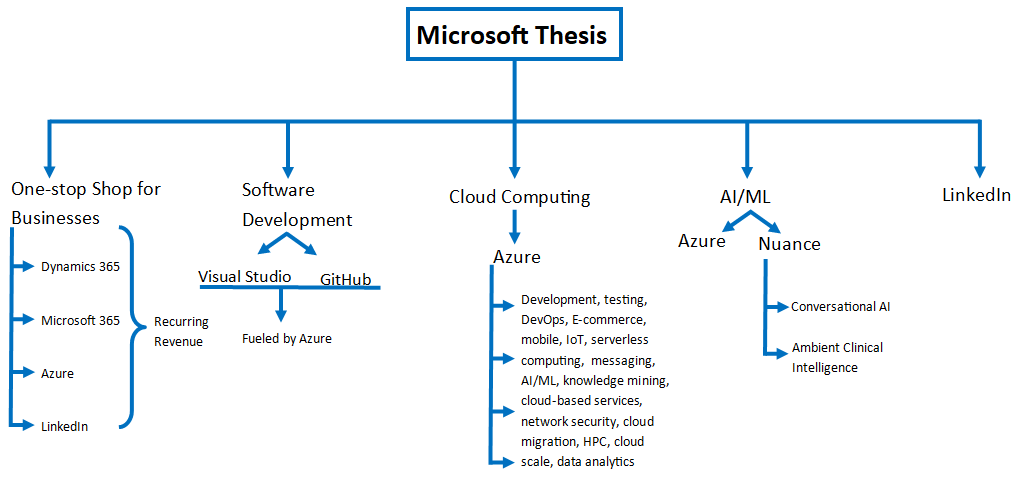

There are several elements in play when talking about Microsoft’s business. The purpose of this thesis is to somehow integrate all these spread pieces of companies and highlight how they synergize to create value. Although they are all part of what I consider could be the major drivers of Microsoft’s growth moving forward, they’ll be ordered in descending relevance. As a form of orientation, I made the following visual:

Since Satya became Microsoft’s CEO in 2014 (will be discussed later), the company has been very focused on building solutions for all verticals of necessity other companies have. Imagine a person in charge of a business, doesn’t matter the size, nor what management’s needs are, Microsoft will have a solution for it.

Microsoft 365 added to Dynamics 365 come together to cover productivity, efficiency, crm, sales, performance, working tools, collaboration, data analytics, project/program/store management, marketing, operating systems, human resources. I must emphasize Microsoft Teams plays a key role here, since it acts as the portal to all products.

If you combine Microsoft Viva with LinkedIn, you obtain an end-to-end employee solution. Combined, they can be used to attract, manage, analyze and boost employees professionally and personally. More explicitly, they provide hiring solutions, talent solutions, learning solutions and a platform meant to address concerns on employee-experience. On the other hand, if a business decides to promote its growth, LinkedIn is a vast platform that offers marketing campaign and the business unit has a sales solution.

Azure complements by facilitating the required hardware and software needed to perform any task, as well as powering cloud-based services offered by products like Dynamics 365, SharePoint, Azure Virtual Desktop.

This gets to show how powerful the combination really is. Moreover, most services and products provided within this ‘space’ are sold via subscriptions, which means Microsoft enhances its business resiliency through selling them.

The second, which could easily be the first, most determinant component of Microsoft’s Thesis is, in my opinion, Cloud Computing. It’s indescribable the impact this sector has had in the whole world. It constantly seems as if cloud economic activity has peaked, given its size, but as a percentage of IT spending, which seems a valid perspective, public cloud spend accounts for 10% of the total budget.

Cloud solutions use cases are innumerable and Microsoft Azure is a solid and very well positioned player in almost all verticals cloud has. This makes Azure one of the main beneficiaries of the large secular tailwind cloud possesses. Given its vast portfolio of offerings, as well as efficiency and experience, Azure should be able to capture a large portion of the inevitable transition IT budgets seem to be having.

The third leg Microsoft’s Thesis has is AI/ML, a space that is already seeing traction. It may not be worth to share more forecasts of the TAM since they reach absurd numbers. Being such a revolutionary technology makes impossible the task of correctly evaluating where it can end up, or how will it influence economic activity. As of today, one of the segments in which AIs have been proved successful is the conversational AI, where Microsoft has one of the key players, Nuance. Nuance is recognized globally, having won many Recognition Awards in the past years for its performance. This could be a vertical with heavy expansion in the near future.

On the other hand, Microsoft counts with Azure, a cloud that offers automation products and, alongside with GitHub & Visual Studio, a very comprehensive in all manners AI/ML development environment. The following image is from Sam Altman, former president of YCombinator and current CEO of OpenAI.

In conclusion, Microsoft will be completely exposed to AI/ML by end products and by providing the tools for development.

As a fourth pillar I personally see software development. Through Visual Studio GitHub and Azure, Microsoft covers the complete spectrum of what’s known to be development. The world has been slowly but consistently transitioning to the cloud, figure that can be spotted through this visual (most recent I could get was from 2018). It represents “Digital economy as a percentage of total economy GDP in the United States.”

The underlying trend is clear, the digital economy is gaining market share out of the grand economy. As overall demand for cloud continues to grow, so should the demand for development products. Open-source development could play a key role here since it acts as a way of rapidly compounding software development. It’s like if devs were creating legos, which can then be used by other devs as foundation for their code, speeding up the complete development process. Owning GitHub makes Microsoft the leader in such space, where customers seem to be happy with the platform and are greatly welcoming added-value services like GitHub Copilot. Having possession of the environment that will give tomorrow’s products shape can be powerful. Lastly, the reason for including Azure in this part is for its indirect development offerings, as well as being Azure capable of acting as the fuel via Virtual Machines for example.

Finally, the remaining component of Microsoft’s Thesis is LinkedIn as a whole. This business unit could be seen from two different perspectives.

Firstly, its growing and immense user base has allowed the platform to build some sort of monopoly over professionals. As time goes by, LinkedIn seems clearer and clearer as the first-choice professionals go to when they need to get a job, and the first option for enterprise to find professionals. Being the gatekeeper of such reciprocal bridge makes Microsoft exposed to a still growing market and one which will always exist.

Secondarily, LinkedIn has evolved to be multi-usage, from the aforementioned, to a sales solution, to advertisements and analytics. The embedded optionality is not only a plus, but the different segments have grown drastically and belong to markets, like digital ads, that are expected to continue in that path. Emphasis goes to the ads sector. Having built such an intricated platform of 850M users is showing above average advertisements results and this could continue to be the case given LinkedIn’s market positioning.

One other thing that could play a significant role in Microsoft’s future is gaming. Owning one of the two main players among console vendors, having such a vast portfolio of gaming studios and being one of the leaders in cloud gaming could fuel some of the company’s future growth. However, with the pending acquisition of Activision Blizzard, I’d rather not include gaming as a main pillar for this thesis. When that huge deal goes through, or not, I shall write a complete article dedicated to the gaming division.

Management

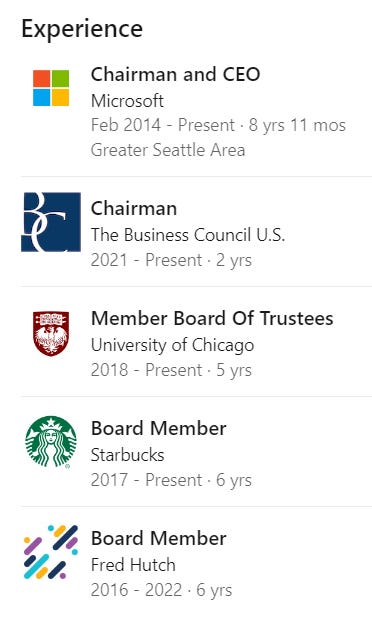

Satya Nadella joined Microsoft as a young engineer in 1992. By 2007, Nadella was the senior VP of Microsoft Online Services, which made him in charge of Bing, the early versions of Microsoft Office and Xbox Live. In 2011, he was appointed for President of the Server and Tools Division, which oversaw the Azure cloud platform and products for companies’ data centers like Windows Server and the SQL Server database

In February 2014, Bill Gates took the decision of making Satya Microsoft’s CEO, after Ballmer stepped down. This turned out to be an inflection point for the company. Since that date, Microsoft’s market cap multiplied by 5, revenues grew about 2.5x, net income margin and operating margin increased more than 1000bps, recurring revenue increased from 15% to 60%, Azure has become the second largest player in the cloud computing space, Microsoft has acquired LinkedIn, Nuance, Xandr, GitHub, Minecraft; the company launched Teams, Viva, Dynamics 365, and more.

Sometimes, things can be a coincidence, though the innovation Microsoft has been through really takes out the possibility of this being one. Satya has changed the complete business model, its focus and its financials as well. From these mentioned points, a common conclusion to arrive is that Satya has been working on making Microsoft a complete cloud player, full of services, rather than products, which boosts the company’s resilience.

Not only Satya has been leading Microsoft’s vision change, but Glassdoor reviews also reveal him as a best-in-class CEO. In terms of personal appreciation, the culture and values he professes, employees really seem to see a phenomenal leader.

Something to keep in mind of is that, currently, Satya’s Chairman of The Business Council U.S, Board Member of the University of Chicago, Board Member at Starbucks and, until this year, he was Board Member of Fred Hutch as well. This does not necessarily represent a risk. The number of activities a person can perform at peak efficiency varies from human to human, though, as said, it’s something to at least keep an eye on.

When evaluating management’s skin in the game, the same repetitive pattern among large companies arises. All top owners together have less than 1% of the company.

I extracted some phrases from hearing to interviews Satya had in the past couple of years.

“One of the things my father said to me once was, when I work in an institution, I wanna make sure the institution becomes stronger and it doesn’t fall apart after I leave.”

“LinkedIn, GitHub and Minecraft are all the large ones and they are all centered in building communities around something we had permission in.” (This is before Nuance)

“You are only a better owner if the mission for a LinkedIn, or a GitHub, or a Minecraft, could be realized better with Microsoft as a platform. In fact, in all three, one of the interesting things for me is we had other people bidding for these assets and all three founders chose to sell to Microsoft.. I was not surprised, but I feel like we got it right.”

It’s all about personal perception, of course, and for all we know, he could be lying. Leaving those assumptions aside, some of the possible conjectures are the following:

Satya’s a true long-term thinker, which has been proven to be the best approach (for stakeholders) when managing a business

There’s an ultimate vision for the company, which may not have been revealed yet

The founders saw Satya and Microsoft capable of making their creations thrive

This last part is very subjective, but so is everything. For the registered performance Satya Nadella has had in the company, he could be seen as one of the 21st century visionaries, time will tell.

MOAT

Microsoft owns a lot of different businesses, therefore, what seems to be the most logical approach is to evaluate competitive advantages singularly. We’ll be addressing the most relevant ones like Azure, Office 365, Dynamics 365, LinkedIn, Xbox and Nuance. It’s not in any order of relevance or weight.

Azure counts with three competitive advantages:

This is something I read on AWS High Switching Costs, but it perfectly applies for Azure as well.

“Moving from one cloud to another is not a simple process for a company like Netflix. Netflix uses AWS for nearly all its computing and storage needs, including databases, analytics, recommendation engines, video transcoding, and more—hundreds of functions that in total use more than 100,000 server instances on AWS. It also uses 1,000 Amazon Kinesis shards work in parallel to process the data stream. Now just take a minute and think about migrating this massive workload.”

Economies of Scale is seen when a business has made significant CapEx and fixed assets investments for that to generate an advantage over other and new players. Azure is the cloud provider with the most data centers distributed around the world, with over 200 (AWS is the second with around 130), making it the one that covers the most regions and time availability zones. Regions are like the places where you locate your resources. The closer they are to customers, the smoother their experience will be. Furthermore, the infrastructure Microsoft developed allows customers to operate at a significant lower cost per unit than competition.

Microsoft 365 (which includes both office and the operating system) benefits from the following:

Network Effect. Most users run Windows on their PCs, so most developers will target that platform, which will make more applications available for it, which will in turn attract more users, and so on. On the other hand, Office has it as well. The more the software spreads, the more it becomes essential for everyone to know how it works, making it spread even more.

High Switching Costs. In office, this one comes from compatibility, data format (this is becoming a smaller problem) and ease of use. If your company pays for Office 365, the most likely scenario is that all databases and programs are run so that they are compatible with Word/Excel/etc. At the same time, for individuals, both Office and Google’s Workspace offer similar resources, and once you are used to using one of them, it’s very unlikely you’ll arbitrarily decide to stop doing so. On the Windows side, there’s virtually no other operating system to turn to, unless you switch PC provider to Apple.

Brand Value. Brand value comes with awareness and association of a brand to a particular concept. Word/Excel/Power Point/Windows may probably be the most widely known pieces of tech, perhaps just under YouTube or Google.

Dynamics 365 benefits from High Switching Costs, like any kind of utility software. Once you start using Dynamics 365 CRM, planning tools, finance tools, automation tools or any of the enterprise resources available and get used to their particular platform, it’s unlikely one will change. In line with this, there’s such a synergy between Dynamics 365 and Microsoft 365 that makes the intention to switch even less likely.

Given the nature of Nuance solutions, the business unit benefits from several competitive advantages:

Network Effect is a very common MOAT among AI technologies. As you feed algorithms with data, they get better and better and clients go to the best algorithm out there. To truly develop this MOAT, the AI must have farmed tons of data, and Nuance products seem to have achieved such milestone.

Low-cost Advantage. Building an AI is all about R&D and paying for the technological infrastructure. Once this is realized, variable costs get lower and lower as the AI increases reach. At the same time, this R&D and upfront cost suppose a barrier for competitors.

Brand Value is not that strong in this case, almost no one outside the space knows about Nuance. However, the business unit has received an absurd amount of recognition and awards.

LinkedIn seems to be fueled by a powerful Network Effect. The larger the user base and companies’ presence, the more users and companies will it attract. For having some kind of monopoly over this professionals network, it could also benefited from some sort of High Switching Costs, though it’s not clear how.

Lastly, Xbox, understood as the complete game brand with its spectrum of offerings, benefits from two different competitive advantages:

Brand Value. Xbox has been around for over 20 years now and has widely known games like Minecraft and Halo. It would be quite rare for a person to not know Xbox exists. Being the top 2 player in the console market adds to this.

Secondarily, Microsoft is designing a whole world of games owned & developed by themselves. This ecosystem is rapidly growing and once Cloud Gaming is fully released, the Game Pass for which players pay a monthly subscription, could give Xbox quite heavy High Switching Costs.

Competitive Positioning

Once again, it makes no sense to compare Microsoft’s overall competitive positioning given its vast portfolio of products. Therefore, a product per product overview:

Azure

By going through different websites and sources, I was able to recreate an estimate of what could be a comparison between Azure, AWS and Google Cloud Platform, from a cost per month, reach and infrastructure perspective.

As exposed, Azure’s the player with the most datacenters deployed around the world, by a wide margin, and the one that covers the most regions and availability zones, by a comfortable margin. From a cost perspective, it’s slightly less costly Amazon’s AWS and over 10% more costly than GCP. Remember the cost per month is a vague and over simplistic estimate.

The cloud space is currently and has been historically dominated by AWS, having 34% of the total market share, while Azure’s the second largest player with 21% market share. However, as of 2018, AWS held 31.7% market share and Azure 16.8%, meaning Microsoft’s cloud is outgrowing Amazon’s.

One more outtake is the top 3 players hold over 66% of the total Cloud Computing Market, and this dominance has grown from 57% in 2018. The largest players are taking share from competition, which is great to see from an Azure’s perspective.

Down from here, further comparisons get extremely technical, almost unintelligible for an ‘outsider’. Hence, I may address a more technical comparison in the future, as I learn more about the sector.

Microsoft 365

The software productivity app markets has been historically dominated by Office 365, but, since 2017, Google Workspace has grown to a considerable size, turning the market into a duopoly, previously a monopoly.

As of Feb 2022, Office 365 held a 51% market share while Google Workspace 46.5%. Google has four different plans, according to the size and features included, while Microsoft has 8 (4 for SMBs and 4 for Enterprises), which makes a product comparison quite messy. The following table is a comparison of both products. “Pricing”, “Storage” and “E-mail Storage” are taken from the very initial plan offered by both companies. Keep in mind many comparisons are subjective.

I find Office 365’s MOAT kind of superior because the suite of apps have been more extensively used over the past two decades and that makes them dominate the file format. Nonetheless, being G-mail the most widely used mail worldwide, and being E-mail a key resource within the space, Google Workspace kind of mitigates Office argument.

The second component of Microsoft 365, Windows, has always had a monopoly as well. However, the same thing happened to this market, Windows has been slowly losing market share to competitors. In this case, Microsoft’s product still possesses over 75% of the market share. The trend does not look promising, but disrupting or gaining even a small fraction of this market is a very tough task.

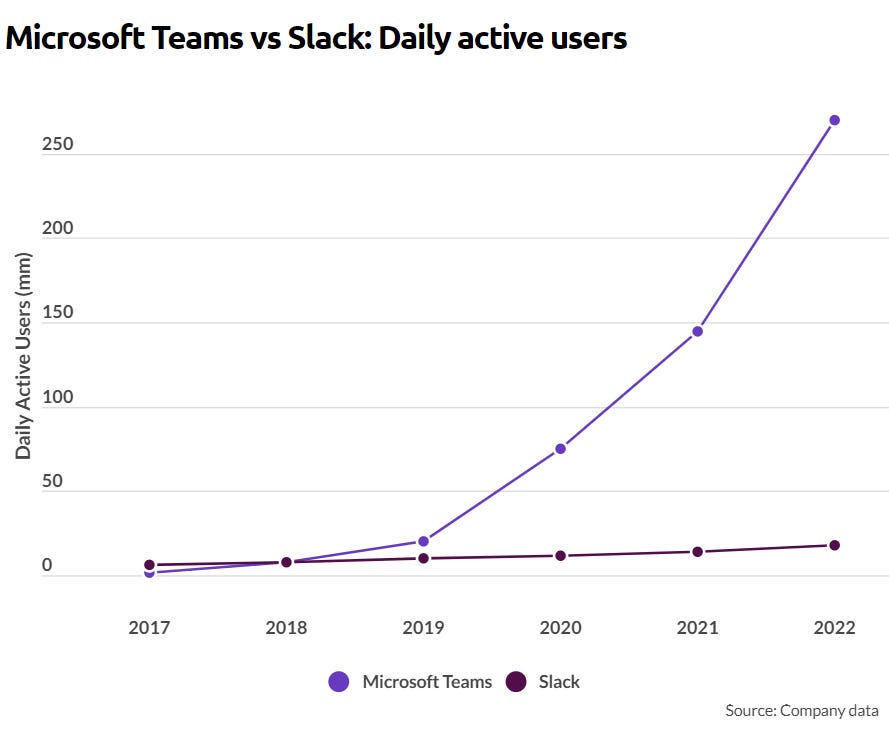

One last thing to mention regarding Microsoft 365 suite of solutions is Microsoft Teams. Given this product plays a center role in the package ecosystem, it seems appropriate to evaluate its competitive position. Execution on this field was astronomically good. Microsoft Teams was launched in 2017 and since then, took over the market, growing from none to over 270M users. Teams’ closest competitor is Salesforce’s Slack, which has under a tenth of the user base.

Dynamics 365

It competes in a quite diverse set of markets, with the most representative ones being Customer Relationship Management and Enterprise Resource Planning. As of 2021, Microsoft’s solution was the second largest player, barely behind Salesforce. It’s noticeable that since inception in 2016, it has grown from no market share to 29%.

On the ERP front, it leads the market and by a huge difference. Dynamics 365 has 31% of the total market with the second player being SAP, who accounts for almost 12% of the total share.

Nuance

Nuance participates of the Speech Recognition and the Ambient Clinical Intelligence market, in overall terms. There’s not much data on the industry nor a breakdown of participants’ market share. This is the only thing I was able to find:

“Their largest market share is in the Speech & Voice Recognition Software Developers industry, where they account for an estimated 16.2% of total industry revenue.”

Xbox

Xbox mainly derives revenue from gaming consoles, gaming subscriptions, in-app purchases, and ads, at the moment. For the reason of the segmentation being so particular, there’s no actual breakdown of such industries’ market share. On the Gaming Console front, as of January 2022, Xbox had a 40% market share, severely behind Sony’s Playstation.

Financial Soundness

Over the past 10 years, Microsoft has compounded revenue and gross profit at a 10% rate, same with gross profit. Net Income, interestingly, compounded at a 14% rate, implying margins have expanded. Free cash flow grew slightly faster than revenue, at an 11% CAGR. It is noticeable however that financials were fairly stagnant from 2013-2017. Since 2017, metrics multiplied by a factor of 2.5x on average.

Microsoft margins have been steadily improving over the last decade. Since Satya joined in 2014, it appears as if the company went through a 4/5 years operating investments, which made margins deteriorate. Since then, all of them have consistently ticked up until this past quarters, characterized by the inflationary pressures all companies have suffered.

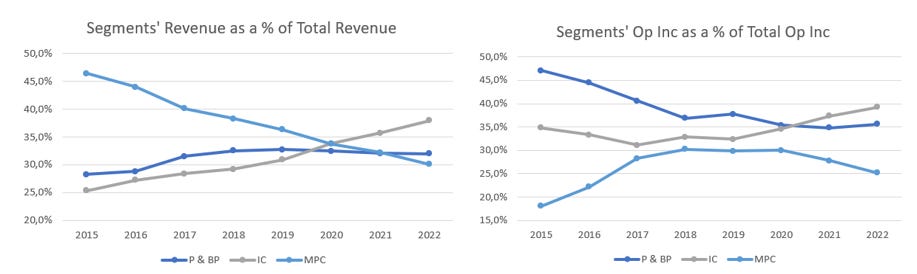

The following image illustrates how the company’s different segments have performed since 2015. It’s remarkable how composition of revenue and operating income has changed in the Satya era.

Trends look definitely promising. Microsoft is tending towards Productivity & Business Processes and Intelligent Cloud to conform a larger portion of total revenue. The composition of operating income is only a consequence of how single revenues have trended.

The reason for this being positive is the reliability and stickiness of the products composing IC and P&BP, shown in Microsoft’s ARR over time chart. At the same time, both segments are the ones better positioned for the coming decade and, iterating to add value upon their offerings seem simpler to do.

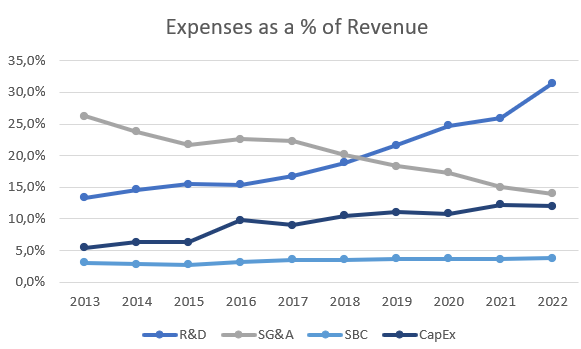

Now, to evaluate management’s discipline and skill when allocating capital, it’s useful to analyze how have expenses as a % of revenue performed over a long period. Microsoft has been a quite mature company for the past decades, but the recent cloud-based approach has unlocked high growth once again. For its previous stance on the curve of maturity, it would be ‘normal’ for expenses to remain kind of steady as a percentage of revenues. Nevertheless, the recent spin off has influenced heavily in how the company spends its money.

Stock-based Compensation has remained below the 5% threshold. In the period 2013-22, revenue increased 120%, while market cap increased 500%, meaning SBC dilution has been trending down.

Sales, general and administrative expenses have been pronouncedly trending down for the past decade. This means that the ‘indirect’ expenses needed to run the business, among which there’s salaries, rent, electricity bills, have been increasing at a slower rate than revenue.

Microsoft built its first datacenter in 1989. As of June 2015, it had around 100 datacenters, and had spent around 15bn on their infrastructure. In the subsequent 7 years, the company more than doubled the number of data centers and thr overall cloud infrastructure’s capacity. This resulted in heavy CapEx investments, which can be seen either positively or negatively. The bright side is that the developed network overtook competitors’ respective networks and this can translate into a competitive advantage. On the negative side, free cash flow will not be as high as it can be during the investment period. Some quotes from an early 2021 Microsoft post:

“Microsoft is slated to add datacenters in at least 10 more countries this year, and the company is on pace to build between 50 and 100 new datacenters each year for the foreseeable future.”

“the pace of change over the next five years is likely to eclipse the pace of change over the past 20 years”

The mentioned ‘pace of change’ will include improvements all across the board. The company committed to powering their datacenters 100% by renewable sources of energy by 2025. Likewise, Datacenters use water to cool and control the temperature, in which front Microsoft is aiming to move towards waterless cooling technologies. Other expenses will be for automation, mechanical and electrical infrastructure, better encryption and security.

Lastly, Research and Development has been highly increasing since Satya became CEO. A potential approach to measuring the impact of such spending is to evaluate what did it result in. In this case:

Launched Dynamics 365, now a top 3 player

Launched Microsoft Teams, now dominates the market

Azure went from 10% market share to 21%

Recurring revenue went from sub 15% of total revenue to over 60%

Launched Microsoft Viva

Multiplied GitHub’s revenue and users by more than 3x

Datacenters were improved

LinkedIn’s revenue increased over 200%

Offerings expanded across the whole Microsoft spectrum

Returns on capital improved considerably (check below)

Bottom line margins improved

Very difficult to accurately tell if it’s desirable to have a 30+% of R&D because results are not always certain. Past R&D seem to have been wisely employed, implying an efficient team, though this does not guarantee anything.

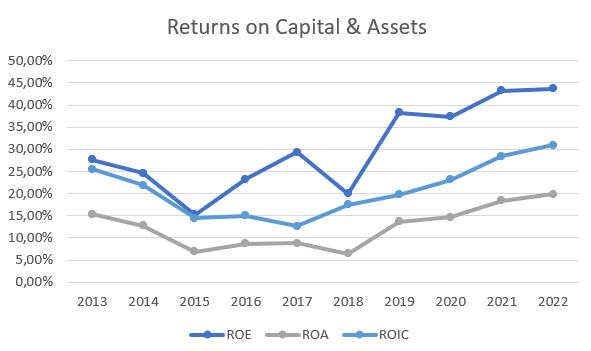

Two things remaining to evaluate Microsoft’s financial soundness, which are capital allocation skills and balance sheet’s fragility.

Investments made when Satya took over, damaged returns on capital over the short term. But, as margins did, return on equity, on assets and on invested capital, only ticked up since 2018. Over the exposed timeframe, Microsoft had an average ROE of 30%, an average ROA of 12.5%, and an average ROIC of 20.9%, implying highly efficiency on invested capital and resources utilization. It’s noticeable that at the end of the decade, ROE standed at 43%, ROA at 20% and ROIC at 31%, all of which are stellar.

In the period 2013-22, Microsoft has been steadily increasing stocks repurchased, dividends paid and debt repayment, meaning the company’s increasingly returning more capital to shareholders. The amount of capital destined to repay debt increased at a 23% CAGR, the amount destined to stock repurchases at a 22% CAGR, and, finally, total money spent on dividends achieved a 10% CAGR.

As of the last reported quarter, 1Q FY’23, Microsoft had 130bn in cash and short term investments, while having a total debt of 67bn. The company has an AAA rating by Standard & Poor’s and an Aaa rating by Moody’s.

Risks

Key-man risk, perhaps

Heavy competition in the cloud space, with a lot of room for disruption

Many offerings are asset light by nature, meaning competition can look for potential entries with little to no cost

Integration risk. The company made several large acquisitions recently (Nuance for over 19bn, ZeniMax Media Inc for over 8bn) and has a pending immense deal with Activision, for 69bn

Continued high efficiency on R&D is required

Legal procedures

Personal Commentary

I decided to skip analyzing many business units’ particular financials for the article had already gotten quite long, once again. In the future, I’m planning on releasing particular articles regarding:

Microsoft’s Complete Gaming Sector

Satya’s Vision

Microsoft’s Acquisition Strategy

Azure as a whole, with further breakdown

Nuance as a whole

And many more. Feel free to DM me at @Giuliano_Mana (Twitter) if you think there are other potential article topics!

Disclaimer: This is not financial advice.

A lot of the stock buy-back is actually to offset dilution due to share buy-backs. In 2022 SBC was $7.5bn, previous years being $6.1bn, $5.3bn, $4.6bn and in 2018 $3.9bn. Suggesting that this is "returning value to shareholders" is plain wrong. It is enriching insiders at the expense of shareholders by distributing shareholder capital.

Take a look at this: https://rockandturner.substack.com/p/a-free-lunch-no-such-thing . It will shock, amaze and and disgust you in equal measure.

Investors need to be aware of what is going on here. Microsoft is in the middle of one of the biggest financial scandals of modern times.