Mission

“Our main focus is to serve people in Latin America by enabling wider access to retail, digital payments and e-commerce services, and by providing compelling technology-based solutions that democratize commerce and money”

Business Overview

Mercado Libre is an Argentine company headquartered in Montevideo since a few years ago. It was founded in 1999 by Marcos Galperín and Hernán Kazah, alongside a group of entrepreneurs. Mercado Libre firstly was an auction marketplace, as eBay, to then migrate it’s functionality to an authentic marketplace.

Curiously, the company noticed in 2003 that the friction digital payments caused was very aggressive and attempted against the marketplace’s volume. As a solution, Mercado Libre created its fintech arm, Mercado Pago. Two decades later, Mercado Libre has founded it’s own solution to a wide variety of concerns and pain points over E-commerce and Digital Payments.

Business Model

Mercado Libre is historically the main product of the company, which is an online marketplace where people can buy or sell stuff. Since its beginning, the marketplace has been gaining a lot of traction, constantly adding users and increasing Gross Merchandise Value.

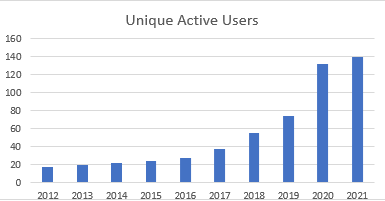

Platform’s usage has grown absurdly, with its user base running from 17M in 2012 to almost 140M in 2021. Enlarging the user base is of extreme importance for Mercado Libre’s ecosystem since it acts as a catalyst for people to get exposure to MELI’s products. In line with this, Gross Merchandise Value and Total Items Sold grew very fast as well. And, adding to this, Mercado Libre’s Take Rate on each item sold has been steadily increasing over time, giving signs of pricing power.

Mercado Pago is the fintech unit of business of Mercado Libre. It started being just a tool to make digital payments but it evolved, becoming a very complete financial app.

As we see, it’s not only about making digital payments through the platform, but it also has multiple solutions in the financial space. In parallel to the marketplace’s growth, Mercado Pago has seen really high growth as well. Total Payment Volume has grown more than 10x with take rate staying in the 3%-3.5% range.

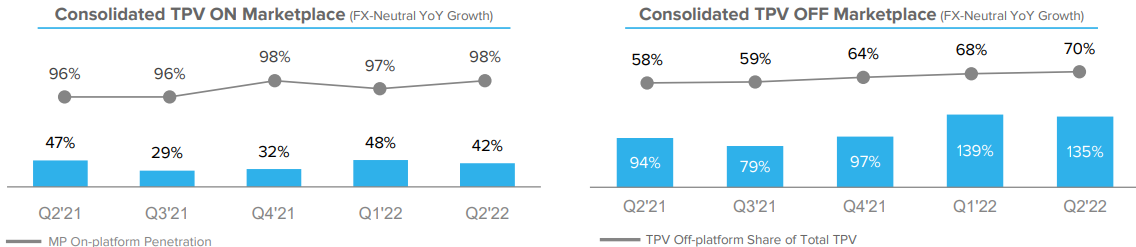

The peculiar thing regarding Mercado Pago is that, over time, it got of so common usage that not only is it used for transactions on the marketplace, but its’ actually getting more use off of it. This is an extremely important developing trend for Mercado Libre since it exposes the company to the actual market of digital payments, outside of its ecosystem, where the addressable market is much larger. As of the Second Quarter of 2022, TPV Off Marketplace accounted for 70% of total TPV, while growing at 135%.

Mercado Envíos is Mercado Libre’s logistics arm. It was born in 2013 as a solution to one of the most obvious problems that arise from E-commerce, product distribution. This is an area that involved a heavy degree of investments from Mercado Libre. The purpose of it was to build infrastructure so that Mercado Envíos has rapid access all around the countries where it operates. As of 2Q 2022, Mercado Envíos shipped 91% of total products and almost 80% of all volumes were delivered within 48hs.

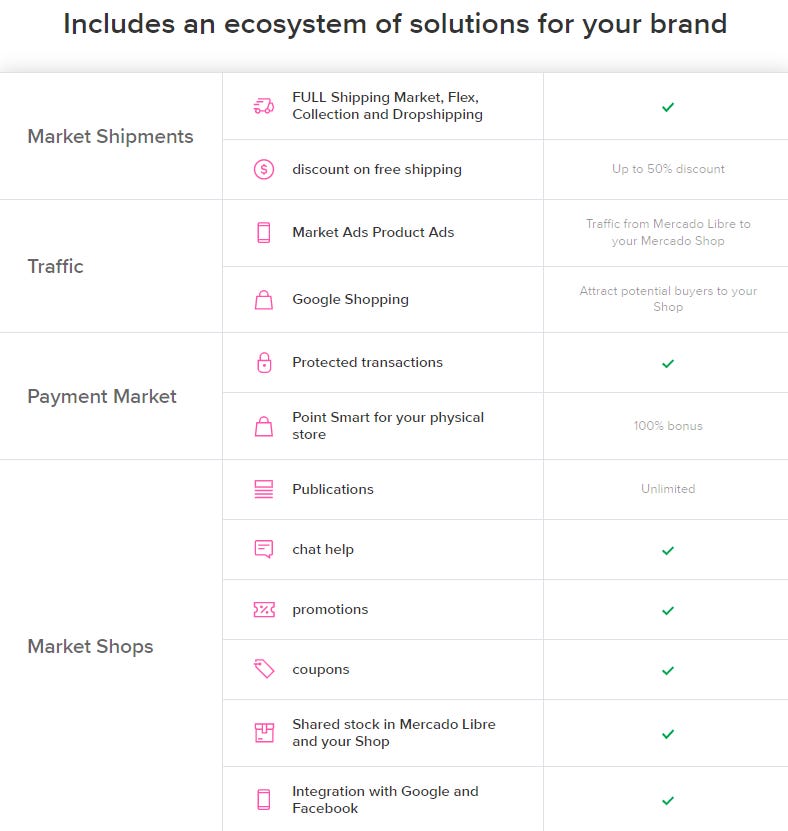

Mercado Shops is a service the company offers to its users that allows them to create their virtual store with some added features:

Mercado Crédito is Mercado Libre’s credit solution. It offers credit lines to both online merchants as well as MPOS device users. Because their online merchants’ business flows through Mercado Pago, they are able to collect principal and interest payments from their existing sales on Mercado Libre’s Marketplace, meaningfully reducing the risk of uncollectability on the loans originated to merchants.

Mercado Ads serves as a tool merchants can use to publicize their products.

Yes, that’s a ton of businesses. Although some of them may shine on their own, like Mercado Pago, is this ethereal synergy the thing that characterizes Mercado Libre’s whole ecosystem. The company got to reduce friction on E-commerce drastically, serving across the whole value chain.

The business’ revenue therefore is distributed among different products, industries and regions. It is not disclosed the exact amount coming from each source. Mercado Libre differentiates revenue for coming from the marketplace and everything except the marketplace.

Industry

The industry to which Mercado Libre is exposed that represents (currently) the majority of revenue is E-commerce. This trend has been around for over twenty years now, but it is still growing rapidly and there’s a lot of room left for growth.

Online sales have grown by 5x over the past 8 years and the sector is expected to continue attracting buyers and sellers in the coming decade. At the same time, online sales just represent a 14% of total sales done in the US. It can be observed how online sales have been gaining market share of total sales in the past decade but it still represents a somewhat small fraction of the whole.

The second industry to which Mercado Libre is exposed to in a big way is Digital Payments and Fintech Features. With Mercado Pago, the company has one of the region leaders when speaking of Digital Payments and probably the best positioned player to capture growth ahead. As we’ve experienced in the past decades, this trend continues to play out and, in Latin America, growth is expected to outpace world’s in the next couple of years.

“Latin America Mobile Payment Market is expected to register a CAGR of 24.5% from 2022-27.” Mordor Intelligence

“Total transaction value is expected to show an annual growth rate (CAGR 2022-2027) of 15.74%.” Statista

A key point to be made regarding both industries is the stickiness they have, implying underlying resilience to more turbulent periods. Multiple Small and Medium Businesses tend to sell and depend on E-commerce Platforms like Mercado Libre, meaning they’d continue utilizing the service and selling online. On the other hand, people don’t usually change either payment method nor their provider. As a consequence, we get two resilient industries.

Thesis

Mercado Libre is riding multiple secular trends, mainly the two aforementioned. The fact it is doing so, as a leader and in a non-developed region like Latin America, is only signal of the immense potential for growth ahead. Being a leader would allow MELI to capture a vast majority of it. At the same time, we are talking about two industries known for their excellent fundamentals, which would imply that Mercado Libre should have no problem in turning topline growth into bottom line as well. The company has already shown a 25% fcf margin and an 80% gross margin when it was focused on profitability in 2012.

The other thing worth mentioning is the potential shift (already happening) in Mercado Pago, turning to be the leader in digital payments and fintech solutions in Latin America. The reason for the importance of this relies in the fact of the impressive fundamentals this business has (shown by companies like Visa) and, as previously mentioned, the stickiness of it. A much more resilient and profitable business model would be achieved if Mercado Pago grew to a larger percentage of the company’s total sales.

Management

Mercado Libre, as opposed to the previously covered companies is founder led. Marcos Galperín is the company’s CEO and has been since he founded the company in 1999. He envisioned an E-commerce business in the late 90s, when internet was in its beginnings. He later proceed to envision Mercado Pago, digital payments, way before it got to be a thing. I believe Marcos would enter the category of visionaries.

Mercado Libre has a phenomenal culture, with great ratings in all categories. With 3.200 ratings, Marcos gets a 94% Approval Rate and the company’s values are highly steamed by employees. I live in Argentina and have some friends working at Mercado Libre. They have only said good things regarding these topics.

According to the SEC filings the company reports, board ownership is less than 1%. However, Marcos Galperin’s family, via the legal vehicle “Galperin Trust” owns about 8% of Mercado Libre.

It is worth noting that not only Marcos has been involved for a long time in the company, but so have most of the high tier management. As shown in the image below, the CFO has been around for over 23 years, having performed a variety of tasks within the same company. The President at the Fintech area has been around for 22 years. Same thing with the COO and the CAO. The commitment of management towards Mercado Libre is very unique and the wide variety of tasks they’ve performed withing the company makes them knowledgeable of the most detailed things.

MOAT

Mercado Libre benefits from a wide variety of moats in my opinion. I generally try to narrow down the competitive advantages a company has, to the strongest or the two strongest. But in this case, I think it is important to highlight the actual four-pillar moat.

Firstly, the strongest one appears to be the Network Effect Mercado Libre and Mercado Pago have. On the E-commerce side, acquiring more sellers amplify the range of products sold through the platform, which in turn attracts a wider variety of buyers, and the flywheel starts over. On the Fintech side, people generally tend to use the digital payment methods that most people use, for it to be the smoothest possible process. Although this competitive advantage comes naturally to both businesses and could cloud the opinion on whether the company has built the actual moat, Mercado Libre has gotten large enough that it has.

Secondly, Mercado Libre and Mercado Pago both benefit from having High Switching Costs. Since the beginning, retail stores have sold through online media like MELI’s marketplace, but it generally was just something they did in parallel to their physical selling. Last couple of years have been quite interesting, many SMB have built their online store and now their sales depend completely on it. This makes it quite hard to move business to another marketplace.

Mercado Pago’s high switching costs comes from another perspective. Even though nowadays, changing payment method is not as hard as changing banks, people are lazy to do so. They tend to stick with what they already use and know, the UX they are familiar with. At the same time, Mercado Pago is actually the leader in features provision which includes things like Mercado Fondo or an easy PoS payment, hence providing more reasons for people not to change their digital payments method.

Thirdly, the marketplace, helped by Mercado Envíos, benefits from economies of scale. When people have to choose which E-commerce platform to use, we generally prioritize price while trying to minimize the delivery time. Mercado Libre has been investing into Mercado Envíos for the past decade. It has now built a large enough infrastructure along Latin America for shipment delivery to be the shortest among competitors. The fact of Mercado Envíos having a 90+% shipping penetration with an 80% rate of delivering in less than 48hs provide customers with a great experience.

Lastly, the fourth durable-competitive advantage the company has is its Brand Value. Mercado Libre and Mercado Pago have been around for several decades now and have built their brand awareness among Argentine/Brazilian and Mexican population. Not only everyone knows both brands but also they are regarded as high quality services. Again, I live in Argentina and I constantly see this in my day to day; in supermarkets, cafés, restaurants.

Competitive Positioning

As of the E-commerce sector, Mercado Libre dominates by far in terms of Gross Merchandise Value. In the second quarter of 2021, the company had more than triple the GMV the second player had.

In terms of website visits, there’s a similar picture. Out of the top 10 most visited E-commerce platforms in Latin America (2021), Mercado Libre occupies the three first spots and the last one. Adding the websites visits, we obtain that Mercado Libre got around 600M visits, whereas the second contendent, OLX in Brazil, barely got 130M, less than a fourth.

Mercado Pago is the leader as well when it comes to digital payments in Argentina and Brazil. The following image is from August 2019 (latest I could find) and it’s already shown how it had captured most of the market share and it also already had the most usage intensity.

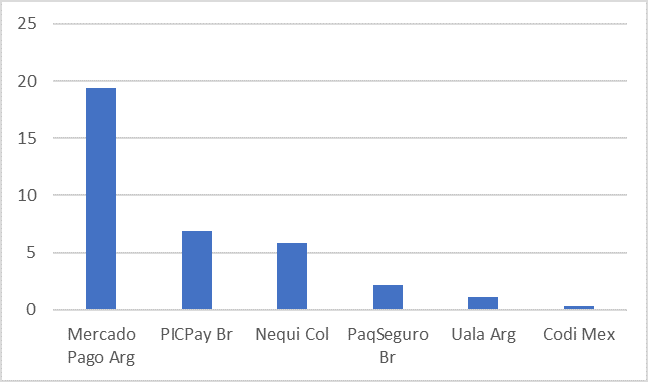

The following image is from January 2022 and signals the amount of visits per digital payments app in Latin America. As observed, Argentina’s Mercado Pago leads the pack by a wide margin.

Financial Soundness

As per usual, I know posting two continued images is not the best visually but if not, it turns unintelligible.

Anyway, a summary:

Mercado Libre’s financial history is a very particular one. In 2010, it was mostly optimized for profitability but after 2014 and the heavy investments done in Mercado Envíos and other ventures to fund growth, profitability was not the main focus. This made margins collapse over the 11 year period. However, Mercado Libre kept being free cash flow positive all along the way, which speaks of the natural fundamentals inherently relying. In the same line, net income turned negative three years in a row, in 2018-2020, but margin stayed below the -10% threshold. Not all growth companies can say the same.

The investments made and the focus in growth were not completely in vain. Mercado Libre grew revenue by almost 35x over 11 years, achieving a 37.3% compound annual growth rate, which is extremely high for such a long timeframe. This of course would be irrelevant if the business could not ever turn this revenue into profit, but this is not the case.

Invested capital returns varied quite a lot over the selected timeframe, but on average were well above growth companies’ standards. Return on Equity averaged a healthy 18%, while Return on Assets a 10.8% and Return on Invested Capital a high 23%.

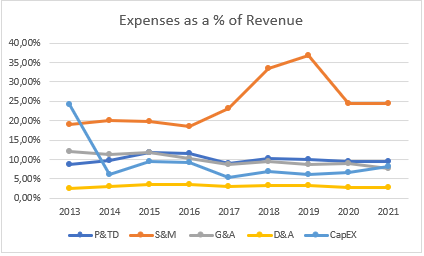

Other useful metrics to evaluate management’s capital allocation discipline in growth companies is expenses as a percentage of growth. As a company matures, investors would rather want this expenses go down. The following image reveals Product and Technology Development, Sales and Marketing and General & Administrative Expenses as a percentage of total revenue. It also illustrates Depreciation & Amortization and Capital Expenditure as a percentage of sales. In all cases, except S&M, they stayed either flat or trended down.

Mercado Libre currently holds 2.2bn dollars in cash and short term investments while it has 5bn in total debt. This could sound somewhat concerning, though the company generated 1bn dollars in free cash flow over the last twelve months, and operating leverage continues to kick in. Anyway, Mercado Libre seems in a much more fragile position than the companies previously analyzed, but it does not appear in that much of a trouble.

Risks

Although obvious to every market, competition is remarkably high in E-commerce.

Government regulations, mainly in Argentina. As seen, more than 20% of Mercado Libre’s revenue comes from here.

Mercado Crédito. The credit business is by no joke an easy one. Determining a customer’s credit risk is not an easy task and doing so incorrectly could severely affect Mercado Libre’s cash flow.

Rise in interest rates (very common in Argentina) affect Mercado Fondo (Mercado Pago)’s demand.

Latin America’ macroeconomics. We navigate uncertain waters and sudden changes in politics and macroeconomics are always a possibility here.

Personal Commentary

I could have included further details on the expansion plans the company has, through extracts of conference calls, but I think the article was kind of long. I’d appreciate if you tell me whether you found it indigestible for its longitude or not.

Disclaimer: This is NOT investment advice, do your own DD.

Excellent writeup Giuliano! I have looked at this company in the past, but my knowledge of S. America has always pulled me away from putting money there. A few questions:

1. Thoughts on margin compression? Is this more a product of continued expansion (like Alibaba) that is causing them to spend elsewhere to continue growing?

2. What is your TAM for their business? Or should I say, can they continue growing at current rate for the next 5-10 years?