I believe this is an interesting read, but I know it could take 2 or 3 revisits due to its longitude. So I invite you to skim through it and subscribe if the content seems valuable!

Thesis

When companies grow horizontally, their thesis, which in many cases is in line with the potential growth sources, tends to follow.

If we tried to keep it simple and minimize items, Google’s thesis would be a product of their past. The company owns the two most visited websites on a monthly basis, Google Search and YouTube.

In parallel, Alphabet is the owner of tens of apps that have an immense number of users, many of them exceeding the billion monthly active users:

Google Search, 96bn monthly visits and 3.3 trillion yearly searches.

Google Chrome, 2.8bn MAUs

Android, 3.3bn users

Google Maps, more than 1bn MAUs

YouTube, over 2.5bn MAUs

And the list goes on and on, covering a wide array of products. This history of owning, throughout decades, a large number of very successful applications, platforms and websites, has allowed Google to capture an infinite amount of information from users, in many different formats, and it’s theirs.

Advertising is not only about exposing products to an audience, but it’s also about who is the ad actually shown to. Being able of correctly identifying perfect customers for advertisers is fundamental for ad businesses, since the quality of their offering goes up because conversion goes up. The extensive list of information-capturing mechanisms Google owns made the company become the one with the largest first party data pool, which allows it to be the best at targeting ads.

Furthermore, Alphabet has been in the digital ads market for a very long time and has become the main vehicle for companies’ advertising. Consequently, Google has constructed the biggest portfolio of advertisers and publishers, their Ad Network. Having possession of this asset is extremely powerful because of its strong network effects. Publishers will look for advertisers where they’ll be paid the most and have the highest fill rate, while advertisers will go to the place where the best publishers are.

The two mentioned forces that act in the company’s favor plus owning many 1bn+ distribution channels should allow the company to keep greatly benefiting from the secular tailwinds the digital ad market has.

The second pillar that conforms Google’s thesis is Google Cloud Platform. The world has been going digital for the past decades, with this trend accelerating over recent years. It continuously seems as if cloud spending has peaked, but it still represents a minor percentage of the global IT budget.

Cloud computing offerings covers, as explained in the last article, an immense number of verticals and use cases. Google Cloud Platform, even if it’s not leading the trend, has been outgrowing its peers and possesses competitive products in each of these verticals. Alphabet should be able to greatly benefit from this sector, which has one of the most pronounced secular tailwinds of the decade.

The third pillar that I believe can fuel enormous growth for the company is their cloud-based platform, YouTube. YouTube basically has a monopoly over the video vertical. This is an extremely powerful asset Google has because everything video or alike-based product will end up on YouTube. Having this monopoly in a market with so much embedded optionality has allowed the platform to place itself in multiple fronts. For instance, its entrance to the television market was a byproduct of the platform being THE place for transmissions.

Nowadays, having a YouTube channel is like operating a broadcasting station with no upfront costs and built-in distribution. This as well is invaluable, since the little friction creators face, helps them create content for the platform, and the more creators out there, the broader the supply will be. YouTube is a place where people are learning from technical topics to things like how to play a game, having fun, being entertained, watching and keeping up with interesting people. It’s quite difficult to state the actual amount of optionality that can derive from providing supply to the audiovisual market. Possibilities are infinite and YouTube is at the center, having the supply and demand in the digital world. I believe this optionality should allow the business to continue recreating itself and capture many more niches.

The fourth major component that could fuel Google’s future growth is the fact of them being the gatekeeper to technology. There are two main technologies consumers spend their time on, smartphones and the internet.

Alphabet is the owner of Android, the operating system that powers more than 70% of utilized smartphones. 3.3 billion users are dependent on Android to access the 21th century most important tool. This puts Google in a position of extreme power and it gets to show why the Play Store is such a profitable business. As time goes by, the economic output generated by smartphones should tend to increase, strengthening Android’s role and enhancing its growth.

In parallel to this, Alphabet owns Google Search and YouTube, the two most visited websites on a monthly basis. GSearch is the literal gateway to all internet offerings. Likewise, YouTube is the platform to look for audiovisual content. The first one’s leading position is highly protected by another core piece of technology that’s very early on in the value chain, Google Chrome. The latter basically ‘forces’ 2.8bn people to utilize the company’s search engine.

Moving forward, I believe the next two sources are secondary and a bit speculative, since they haven’t really proved themselves as highly monetizable. Nonetheless, they are worth mentioning.

Google Maps is the most used and possesses the most nurtured digital world map. Thinking of how crucial is such a product for getting physical orientation makes me believe that there’s also an immense amount of embedded optionality in the product. It seems to me as if GMaps is in a similar place as WhatsApp was during 2015-2019, a widely utilized product, but with little to no effort for direct monetization. I believe the company will invariably tend to launch initiatives and prove how monetizable can be to own this core piece of technology.

Lastly, Artificial Intelligence will probably be the highest contributor to global GDP over the next couple of decades. OpenAI and Microsoft’s deal made everyone assume Google now belongs to a secondary spot in what AI respects. However, DeepMind has one of the vastest and more comprehensive AI research archives. Besides, AIs are fed with data and policies like Apple’s IDFA show why it’s fundamental for a company in this segment to have its own sources of data to feed their algorithms.

Industry

Even though Alphabet has a vast portfolio of products, it belongs to a little number of industries. Before going a bit into them, some overall perspective on the nature of Google’s products demand.

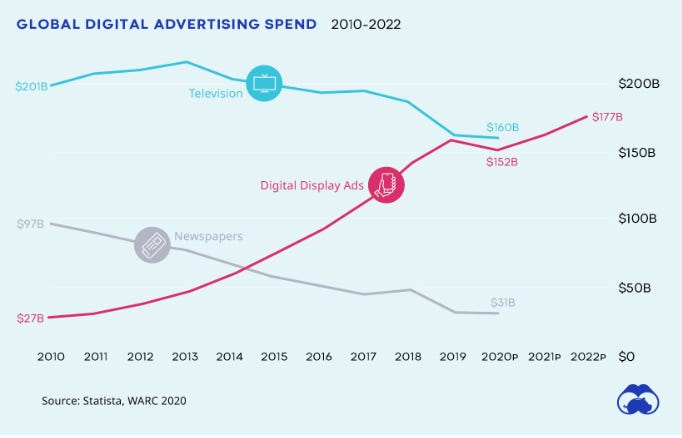

Historically, business owners have always wanted to earn more, ambition is only human. One of the ways to do so is to hike prices until demand collapses. The second way is to sell more items to more people, achievable by expanding the company’s reach to appeal to a larger audience. This was initially done by putting simple and hand-made signs around the store and near routes. Later on, the 19th and 20th century unlocked new distribution methods of information, which were consumed by a large number of people. Newspapers and television are meant to deliver information and entertainment, but since they capture people’s attention, they are monetizable, giving business owners the eyes and reach they seek for. Advertising has always been around. The following chart estimates, in today’s dollars, how have the different ad mediums trended since their creation.

With the arrive of the internet, this new massively consumed digital space allowed for innovative ways to capture eyes. Digital advertising soon began taking share from physical advertising, which makes sense given internet’s high and intense usage.

Even if a bit out of date, the chart above illustrates how have the different medium’s ad revenue been for the past decade. Once again, it is displayed how rapidly did digital ads grow. Furthermore, according to Statista, digital ad revenue as a percentage of total ad revenue has grown to over 60% in 2022. It is impossible to determine at which point will this trend stop. Some traditional and physical advertising solutions have more impact than digital in particular niches or regions, which makes me think they will not disappear.

The last datapoint I usually look at when examining particular industries is the percentage of GDP they represent, which indirectly determines what the expected growth of the sector could be, given a certain GDP growth.

To finalize, and put actual numbers to the issue, Statista estimates the digital ads market worldwide will grow at a 9.42% CAGR between 2023 and 2027, reaching a market volume of 1.005 trillion

Before moving forward, it is key to acknowledge the digital advertising market, and advertising overall, is cyclical. Companies tend to dedicate larger percents of their budgets to advertising when things are going well and they tend to reduce it when they are getting complicated. At the end of the day, promoting your business is crucial, but surviving is more so.

The global video streaming market size was valued at USD 59.14 billion in 2021 and is expected to expand at a compound annual growth rate of 21.3% from 2022 to 2030. Being YouTube the industry leader makes it very much likely for it to highly benefit from this trend.

The last industry I’ll refer to is cloud computing, in which Alphabet owns the third largest player, Google Cloud Platform. Within cloud computing there is anything that involves delivering hosted services or products over the internet. Google offers more than a hundred products in dozens of industries and with tens of use cases. The total addressable market for cloud computing is estimated to grow from around 500bn in 2022 to over 1.1-1.6tn dollars, depending on the forecast.

Management

Until recently, Alphabet has been basically co-founders led. Sergey and Larry have been in charge of the company ever since they came up with the idea of Page Rank, back in 1996, when they were both PhD students at Stanford. However, Eric Shmidt was Google’s CEO since he reached an agreement with Sergey and Larry in 2001.

Their track record is close to perfection. United, both have a history of disrupting and becoming a monopoly in one of the most profitable industries that have existed and they had enough vision to refuse selling their business to Yahoo in 2002, when the latter offered the duo 3 billion dollars. Furthermore, they:

Bought Android in 2005 for 50M, which now has 70% of the mobile OS market share

Bought YouTube in 2006 for 1.65bn, the second most actively used social media and the second most visited website on a monthly basis

Ideated Google Workspace very early on, a previously unconceivable ‘cloud-based productivity software tools’

Pitched Google Chrome to Eric Shmidt, CEO in 2008, a now 2.8bn users browser

Turned separate acquisitions into the most used and precise digital map worldwide

In 2011, Page took over as CEO again and Shmidt shifted to executive chairman. Visions had collided and Larry stated:

“One of the primary goals I have is to get Google to be a big company that has the nimbleness and soul and passion and speed of a start-up,”

A year later, the management team, composed mainly by Larry and Sergey, took a decision that would alter Google’s political structure forever. To ensure their future control of the company, they issued the ‘super-voting class B stock, which have 10 votes per share’. Combined, they hold over 50% of voting rights and did this saying it would allow them to:

“concentrate on the long term.”

As of today, they hold a combined 51.1% of voting power. It’s confusing what’s their actual ownership percentage given Alphabet’s corporate structure and that it did a split in July 2022. Nonetheless, on the one side, Sergey owns 6% of Alphabet’s shares and controls 24.9% of the company’s voting rights, totaling a market value of around 69bn. Larry, on the other hand, holds a 6.3% ownership with 26.2% voting power, accounting for a total of 73bn. Lastly, Eric Shmidt, former CEO, owns 1.4% of the company, or 16bn.

The last member of Google’s leading team is the current CEO, Sundar Pichai. Sundar joined the company in 2004 and has made several fundamental contributions throughout the years.

One of the most notable of them was his persistence and insistence of developing Google’s own web browser in the mid 2000s. Eric, CEO at that time, thought it wasn’t a good idea to get into the web browsers fight that was taking place. However, Sundar talked Larry through the idea and Larry carried it forward to Eric. Pichai oversaw development of Chrome since 2006 and got the product to the state of market dominance. Another of Sundar’s remarkable actions was its leadership in the Android Operating System, which ended providing an immense value to Alphabet.

In 2015, Sundar was appointed as Google’s CEO, upon the corporate restructure of the company (Alphabet thereafter). He was now leading all Google’s products and platforms, including Search, Maps, Play Store, Android, Chrome, Gmail and the Workspace. Few years later, in 2019, Pichai was named Alphabet’s CEO, a position that he currently holds. Larry and Sergey communicated their decision to shareholders in 2019, through a letter, in which they wrote the following about Sundar:

“Sundar brings humility and a deep passion for technology to our users, partners and our employees every day. He’s worked closely with us for 15 years, through the formation of Alphabet, as CEO of Google, and a member of the Alphabet Board of Directors. He shares our confidence in the value of the Alphabet structure, and the ability it provides us to tackle big challenges through technology. There is no one that we have relied on more since Alphabet was founded, and no better person to lead Google and Alphabet into the future.”

With over 41 thousand reviews, Pichai scores 4.4 stars out of five. It seems as if Google has a very strong inside culture and supports employees in a manner they regard as satisfactory. Likewise, Sundar’s approval is at 87%, which given the number of reviews, stands in high territory.

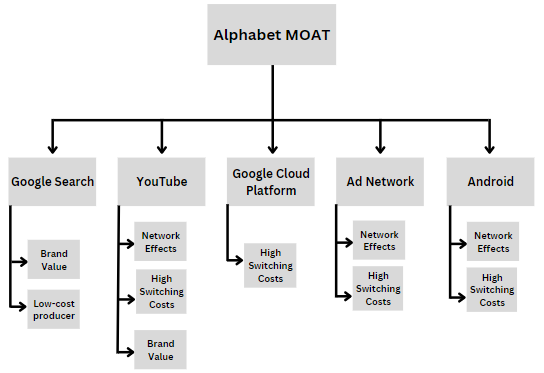

MOAT

Alphabet is a company with multiple business units and, because of it, competitive advantages have to be analyzed singularly.

Google Search

GSearch benefits strongly from two different competitive advantages. Firstly, the search engine is one of the most known pieces of technology ever created, which even made Oxford add the word to their dictionary back in 2000s. Furthermore, it has been ranked as the third most valuable brand in 2022, accounting for a total 263bn in value. It is therefore fair to assume Google has a very strong brand value. Secondly, the large first party data pool Google has fed into its algorithm allows it to be the most precise search engine, both for searching and for targeting ads.

The aforementioned competitive advantages are further enhanced by two things that protect active usage. On the one hand, Alphabet owns Google Chrome, a 2.8bn user web browser, which has Google as the default search engine. To displace Google Search, companies would also have to displace GChrome and people do not like changing these kinds of things. On the other hand, there’s a monetary barrier, which of course would fall if there was a higher bidder. But the fact that Google’s willing to spend multiple billion dollars to be the default search engine in as many devices as possible keeps competition away.

At the same time, being Google the company that owns the vastest amount of data makes them the ones with the possibility of empowering AI products at the highest level. This is one of the reasons why Bing will have a harder time in displacing Google than people believe. Additionally, Google has worked in search engine AI features for the past decade. It should be expectable for the company to have, in-house, a much better and more powerful AI search engine tool than the one released by Microsoft.

YouTube

YouTube is also featured in the image above, ranking as the 75th most valuable brand in the world for a total of 23.9bn. This platform is actively used by more than 1/3 of the global population, everybody knows it and what’s it for, making possible the conclusion that YouTube does possess a high brand value. Secondly, YouTube greatly benefits from network effects, at a truly strong level. The more creators/supply-side agents on the platform, the broader and more diversity the content will have, appealing to a wider range of public and once again attracting more creators. Moreover, the more it’s used, the more fed the algorithm becomes, letting it be the best video recommendation engine, keeping users engaged. Lastly, users do not have high switching costs in terms of actual switching, but the uniqueness and diversity of the platform’s content make people only find that content there. Furthermore, creators are almost completely locked into the platform. Once a subscriber base is built on a YouTube channel, the switching costs for creators are extremely high, for they’d have to build the audience again if they left.

Google Cloud Platform

GCP as all cloud computing vendors, strongly benefits from high switching costs, explained by the following extract:

“Moving from one cloud to another is not a simple process for a company like Netflix. Netflix uses AWS for nearly all its computing and storage needs, including databases, analytics, recommendation engines, video transcoding, and more—hundreds of functions that in total use more than 100,000 server instances on AWS. It also uses 1,000 Amazon Kinesis shards work in parallel to process the data stream. Now just take a minute and think about migrating this massive workload.”

One could also argue GCP benefits from the scale it has achieved as well. Although this is true when compared to small and new players, it does not hold when compared with the two leaders of the sector, whose scale is actually larger, particularly Azure’s. Nonetheless, even with much less datacenters than its competitors, Google Cloud Platform is close to Azure in the amount of availability zones in which it’s offered and actually covers more regions than AWS.

Ad Network

The Ad Network is not a product, but it is an intangible asset, one could say, Google possesses, and fuels its advertising solutions. An ad network is a technology platform that serves as a broker between a group of publishers and advertisers. The more advertisers utilize this network, the more of their counterpart will they attract and the more valuable will the network itself become, perfectly emulating what network effect mean. Google’s ad net has been in place for over two decades now and has become the largest, making me believe it has reached the moat point.

Likewise, being the largest ad network out there means this will be the one that will allow publishers to maximize revenue per impression. This is because the more advertisement demand there is, the more bidders there are and the higher the filler rate. In consequence, publishers who leave the network would probably face revenue headwinds.

Android

Android does not benefit from any competitive advantage from the user standpoint. Perhaps one could argue there’s a minor high switching cost in place once people get used to a particular mobile OS. Nonetheless, if there’s any, it’s minor.

Android does benefit though from a competitive advantage derived from network effects produced by developers. The more developers and smartphones in their ecosystem, the more apps and features will there be, appealing to a larger extent of public. A case could also be made for Android benefiting of a high switching cost competitive advantage. I don’t see it that clear for users, because learning an OS can be a bit annoying, but not that much. Nevertheless, for developers, it can be quite difficult to switch OS. Firstly, they would lose access to this 3.3bn user base if they switched. Furthermore, if devs have dedicated huge amounts of time and invested money in Android’s ecosystem, they may be more reluctant to call it off. Lastly, Google provides a wide range of tools and resources for developers to create apps for Android, such as the Android Software Development Kit (SDK), which makes it easier for developers to create high quality apps for the platform.

Competitive Positioning

It is futile to analyze alphabet’s competitive positioning overall, reason for which we’ll be diving into the most relevant products to uncover how they are doing in each market.

Google Search

Google’s dominance in the search engine market is no news. The company has possessed an authentic monopoly in the market for over two decades now. The following chart displays the desktop search engine market.

Bing has been catching up lately, increasing its market share since Microsoft included Chat GPT’s capabilities into the search engine. At the moment, Google stands at almost 85% market share and it has ranged between 84-87% for the past 8 years.

Google Chrome

GChrome is the browser of choice for over 2.8bn users. Since its release back in 2008 till 2020, it kept gaining market share and after that year, it held it.

As shown in the chart above, Chrome’s market share went from 25% in 2012 to 65% at the end of 2022, which also maintained during January 2023. Although Edge has been recently turning into a threat, Chrome still dominates the market.

In a more technical and personal manner, based on a thorough comparison, I plotted the following table. Runs per minute are based on a Speedometer test which gives “the most comprehensive overview of the browser’s performance”. The agent performs two more tests; one in which Edge outperforms by 1% and the other where Google wins by 2%.

Android

Google’s mobile OS market share has trended upwards ever since inception, leading the market to become a duopoly, shared only with Apple.

Until 2019, Android consistently increased its market share, when it temporarily peaked at 75.56% and then declined to a local low of 70%. After 2020, Android returned to an uptrend and its share currently stands at 71.8%, more than double that of the nearest competitor. This means that for every 100 smartphones out there, 71 utilize Android’s operating system.

Ad Business

This is a fascinating one. I have encountered last week a 150 pages report which goes through how Google has been able to monopolize almost the entirety of the ad business. I have not yet read it completely, so I’ll not include all details. Nonetheless, I’ve been able to extract some quotes and charts that reveal how powerful Google ad business is.

“Google, a single company with pervasive conflicts of interest, now controls: (1) the technology used by nearly every major website publisher to offer advertising space for sale; (2) the leading tools used by advertisers to buy that advertising space; and (3) the largest ad exchange that matches publishers with advertisers each time that ad space is sold.”

“One troubling, but revealing, statistic demonstrates the point: on average, Google keeps at least thirty cents—and sometimes far more—of each advertising dollar flowing from advertisers to website publishers through Google’s ad tech tools”

YouTube

It’s quite hard to place YouTube in a category where it has real competitors, from a perspective of product similarity. The vertical of long-form is YT’s monopoly. Nonetheless, the platform has often been regarded as a social media, point which I don’t agree with.

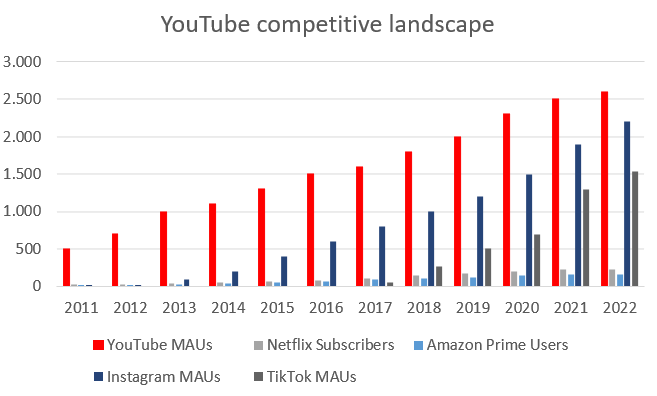

To try compare YouTube, I decided to compute some of the largest players from photo/video social media (Instagram, could be Facebook as well, but I think Instagram is a better fit for it being more visual), the largest short-form video platform (TikTok) and two of the largest streaming services (Prime and Netflix).

Since 2011, YouTube didn’t technically outgrow its peers mainly because they started on a much lower base. However, YouTube is the most used platform/app out of the selected group, with over 2.5bn MAUs. If we took into Facebook consideration, YouTube would be second, after FB’s 2.9bn.

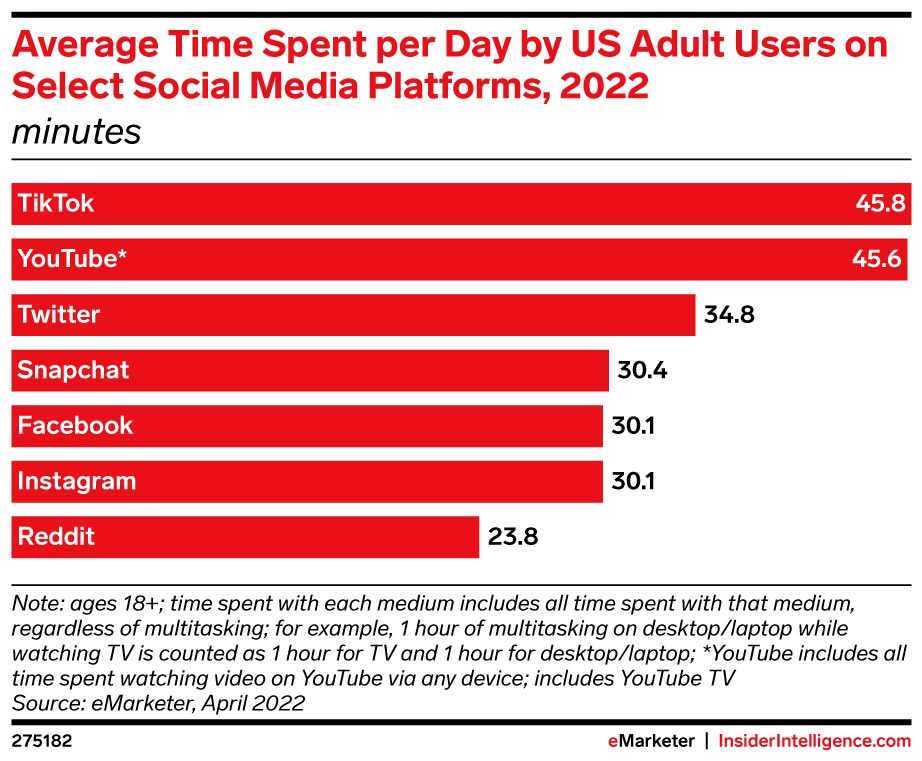

To more deeply analyze YouTube through a social media lens, the following chart aims to illustrate how engaged are users with different platforms.

YouTube is the second in which users spend the more daily time on, at 45.6 minutes, second only after TikTok. This is a fundamental metric to look at because it shows how empty, or not, are a platform’s users. Furthermore, it indicates the quality of the platform, perceived from the market’s point of view. Lastly, from a business perspective, since YouTube sells ads, it is crucial for the it to be highly utilized.

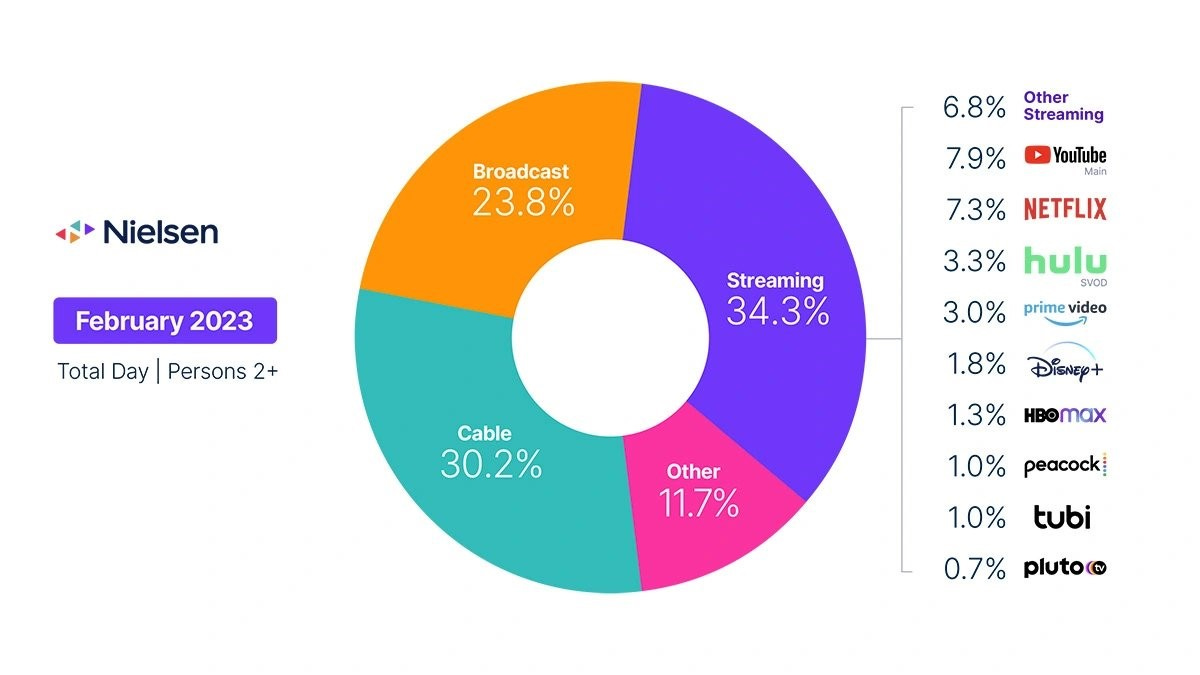

The other big industry to which YouTube belongs and is now a somewhat relevant source of revenue is TV streaming.

The above image is reported by the company. There’s most likely bias in the picked categories, but there are three of them which I think make YouTube a unique value offering. YouTube TV does not have an annual contract, does not have installation fee (it’s cloud-based) and it allows for many more streams and accounts than other services, while charging less.

As of February 2023, YouTube was the undisputed leader in the streaming market.

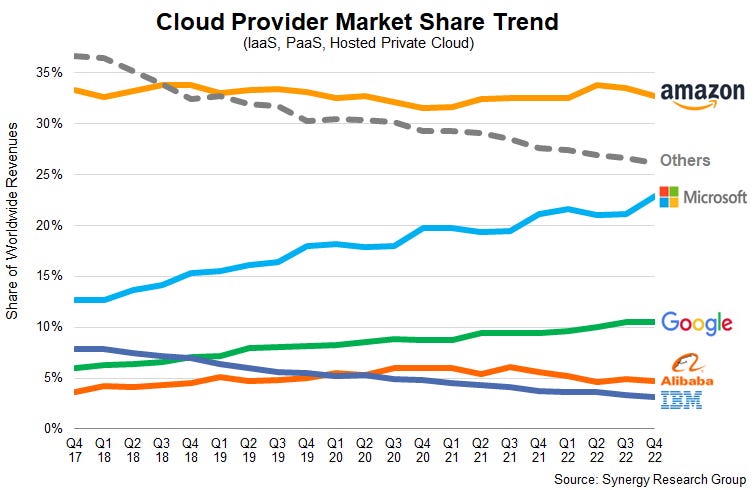

Google Cloud Platform

The last business unit we’ll dive into is GCP.

Alphabet is far from dominating the cloud computing space from a market share perspective. However, from a technical point of view, it’s actually better positioned than Amazon Web Services, at least from the estimates obtained. Despite having many less datacenters around the world, Google has been able to construct them in such a way that reach and cost efficiency are maximized. Reach can be inferred upon the regions and availability zones the company covers, and the cost efficiency, upon the mentioned DeepMind case studies performed.

As of the last quarter of 2022, Google Cloud had a third position, at around 10-11% market share. An important takeaway from the chart is Google’s continued growth, which allowed the company to capture market share from other companies.

Financial Soundness

The purpose of this section is to get a glance at how has Google historically performed from multiple perspectives. Financially, operatingly and allocating capital, perhaps enabling us to infer if:

There’s a good management behind the company

The company belongs to a naturally profitable business

The business MOAT is financially shown

Management is shareholder-aligned

Alphabet is in a financially fragile state

Google’s operating performance has been outstanding.

Revenue has gone from 21.8bn in 2008 to 282bn in 2022, growing at a 20.1% CAGR

Gross profit has grown at a 19.3% CAGR, starting the period at 13.1bn and finishing it at 156.6bn

Google’s operating income increased by more than 12x during the last 15 years, reaching 74bn in 2022 and exhibiting a 18.9% CAGR

Net income has increased at a 20.9% CAGR, going from 4.2bn in 2008 to 59.9bn in 2022

Free cash flow started at 5.4bn in 2008 and the company generated 60bn in 2022, implying FCF has grown at a 18.6% CAGR over this 15yr period

Upon the illustrated financials, we proceed now to analyze Google’s business stability from a profitability standpoint. Since 2008, the company’s margins have been fairly stable, though with slight declines across the board.

In the last fiscal year, Google’s gross profit margin was at 55.4%, 500bps lower than 2008’s

The operating margin ended the period at 26.5%, down around 400bps over the last 15 years

In the selected period, net profit margin expanded 180bps, now being at 21.2%

Lastly, free cash flow margin decreased 400bps and, in 2022, it standed at 21.2%

The fact of margins trending down over such a long period of time can be somewhat concerning. However, it can be the case where Google’s 2008 business model was simply naturally more profitable than today’s. As per that date, Alphabet basically derived all of its revenue from advertisements and had little to no CapEx or necessary investments needed to retain its leading position. This meant it was possible for the company to extract much more cents out of every dollar made in revenue.

As time went by, Google had to reinvent itself and to do so, higher expenses across fields were needed. There wouldn’t be Google Cloud Platform if it weren’t for this or perhaps all products wouldn’t have retained their virtual monopolies. Moreover, the company has been slowly immersing itself in new and unknown territory with its other bets, which can end up providing tomorrow’s cash flow.

Nevertheless, a case can be made in which management has lost its ability to keep the company cost efficient.

Before going into it, the first three costs are computed as a % of total revenues while TAC is in regards to how much of ad revenue it represents.

Operating costs such as R&D and SG&A have stayed relatively flat over the last 15 years, perhaps declining slightly. More importantly, the traffic acquisition costs Google incurs in have continuously trended downwards since 2008. This gets to show Alphabet’s pricing power at some point. If the company is able to pay smartphone manufacturers less than they’ve been increasingly earning, it means Google’s in a much higher position of power than before.

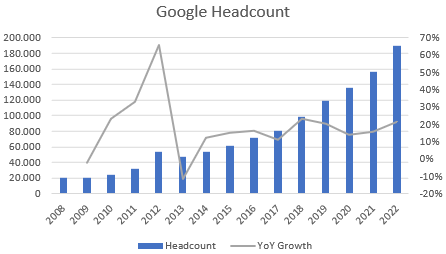

The chart above illustrates how has Google’s headcount evolved over time. The rapid increase in the period 2018-2022, with a 22% employees growth in the latter year, may suggest the company has been in an overhiring spree. Management has claimed that most hired employees are engineers and we could assume a larger proportion of them should be needed for the future growth GCP may have. Nonetheless, such rapid increase in headcount almost always comes at the price of inefficiency.

Lastly, capital expenditures have been pronouncedly increasing over the last decade and a half. This should not be surprising given the fact Alphabet has been placing a lot of emphasis in developing their cloud, building datacenters and strongly working to make them more efficiently. According to some estimates, around 60-70% of the company’s CapEx goes to developing and maintaining their datacenter infrastructure.

As of the last quarter, Google holded 113bn in cash and short term investments, while having 29.7bn in total debt. Moreover, current assets offset current liabilities by 80bn dollars. Considering both factors plus the high profitability at which Alphabet operates, it appears as if the company is at a spectacular financial shape.

Capital allocation skills

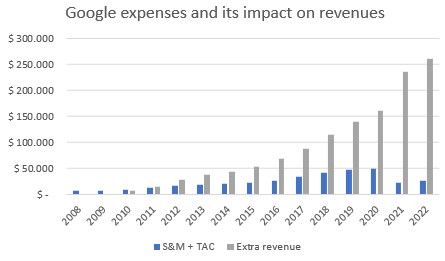

The following chart illustrates the sales and marketing expenses plus TAC Google has incurred in and the extra revenue they’ve generated. I believe S&M results cannot be analyzed based solely on a YoY increase in revenue because there’s a lot of S&M expenses that help build the brand. Therefore, ‘extra revenue’ goes for the differential between the year in question’s revenue minus 2008 revenue.

In this manner, we get a glance on how many dollars does Google spend on growing its topline and how many does it get in return. Perhaps we fall into an overstatement and an overvalue of the TAC expense given they only grow ad rev, but I’ve not encountered a better method to measure such a peculiar enterprise. Anyhow, it seems as if Google’s S&M and TAC does wonders for the company.

Google has always been immersed into naturally profitable industries, allowing the company to earn above average returns on capital.

Over the last 15 years, ROE has averaged 17% with 2022’s being at 23%

ROIC was 25% for the last fiscal year and has averaged 18% for the period

ROA averaged 13% over the last 15 years and finalized at 16%

One further interesting metric that can offer insights on how well does management allocate capital is the one mentioned in one of Buffett’s 1980s letters. Since 2008, Alphabet has retained 182bn of earnings and the market cap has increased by 1180bn, meaning that for every dollar retained, management has been able to create 5.55 dollars value.

Value return to shareholders

There’s a particular thing about Alphabet, it does not pay dividends, so they will not be included in the following chart.

Google is not a company that has historically issued a lot of debt. It seems as if it continuously rolls over its debt, issuing new one to repay old one, which kind of affects the cash flow statement. Nonetheless, for the past 3-4 years, Google has been rapidly reducing the number of stocks outstanding, making them decline by 8-9%. As a reference, in the fiscal year 2022, Alphabet bought back 59bn worth of stock.

Risks

The most real risk Google faces in my opinion is regulation. The company operates multiple virtual monopolies and a case could be made where its acting has damaged the ad market’s efficiency and competition. I have a 150 pages report to read about this and should be writing a future article on the subject.

Microsoft’s Bing AI integrations show how this new technology is set to disrupt all sort of previously conceived monopolies. It’s very much likely Microsoft will be an annoying competitor for Alphabet moving forward.

Management could continue in their path of cost inefficiency which, if Google’s margins come under pressure due to competition, could prove very destructive.

Disclosure: This is NOT financial advice.

Finally got some time to read this. Great work man!

Really great read. Interesting and clear. Thank you for the hard work!