This is my last free research article

This is the last free research article I post. I will expand accordingly on why I decided take this route in Sunday’s article. In any case, hope you enjoy the attempt of industry breakdown and feel free to subscribe after a skim.

What is Building Information Modeling?

Within software as a service, there are two categories to which products can belong:

Horizontal software refers to those services that are industry agnostic and hence spreadable among these. Spreadsheets like Excel, CRMs like Salesforce’s, are great examples of horizontal software. Their design allows them to be applicable in multiple industries and, on occasions, for a variety of purposes. Naturally, horizontal software’s addressable markets are immense.

Vertical software is designed with an industry-specific solution in mind. By definition, their addressable market is limited to the extent of the customers’, within such industry, requirements.

“For example, in the public transit market one of the mission critical aspects of the business that we help automate is the scheduling and routing of vehicles.” Constellation Software

Building Information Modeling (BIM) belongs to the latter categorization. Even though the latter is somewhat shady, assume that for now. Meant for the Architecture, Engineering and Construction (AEC), BIM is the digital process by which constructions can be created and managed. It consists of an intelligent model that enables architectures and engineers to create virtual representations of buildings, objects, envision the asset through its lifecycle and manage ongoing operations. In contrast to prior methodologies, BIM is based on parametric modeling.

Object-based parametric modeling was developed in the 80s. The intention for this new configuration is to not represent objects with fixed geometrical figures and properties, as was previously done. Instead, object-based parametric modeling revolves around setting parameters and rules, which could then be utilized to determine figures and non-geometric properties.

In essence, this involves defining the building blocks upon which objects can then be constructed. Understandably, taking the other route, by fixing and determining objects which would then be leveraged to build digital constructions, would naturally limit buildings' possibilities. Such a limit would be imposed by how vast the universe of defined objects is.

To the contrary, defining properties and parameters make up for a malleable recipe for building objects. This allows for a much broader range of building options. Furthermore, even though somewhat constrained by the set of properties and rules predetermined, users have the capability of customarily building the objects they desire.

Software Characteristics and Their Implications

Even though what we have just covered would imply for users to create any object they want, there is a problem. The purpose with which BIM technologies/platforms are developed mostly defines the end-market at which they will be aimed. Broadly, they can be created with a general or specific purpose in mind.

Given we are speaking about physics, there’s great depth as to how detailed building configurations could be. Depending on the location, the end-market, building/object’s purpose, and legal requirements, the platform that might be more convenient. Generally, niche-specific solutions are much more efficient and suited for specific tasks, compared to general-purpose ones.

The reasons for the above are mostly two. Firstly, the object-complexity each technology is capable of handling is inherent to the parametric rules and properties that are set. Therefore, some general-purpose BIM technologies might turn highly impractical and even useless for designing and dealing with complex objects. Emphasis on this aspect. On the other side, the platform and product themselves are very resource intensive. The problem, and case against a “super BIM platform”, is that companies employing BIM will not be willing to pay for capabilities and features they do not utilize.

Example of what happened with the steel fabrication process:

“BIM tools for building design focus on architectural-level objects, but a different set of authoring tools have been developed for modeling at the fabrication level. These tools provide different object families for embedding different types of expertise. Early examples of such packages were developed for steel fabrication, such as Design Data’s SDS/2, Tekla’s X-steel, and AceCad’s StruCad. Initially, these were simple 3D layout systems with predefined parametric object families for connections, copes that trim member around joining steel sections, and other editing operations. These capabilities were later enhanced to support automatic design based on loads, connections, and members. With associated CNC cutting and drilling machines, these systems have become an integral part of automated steel fabrication. In a similar manner, systems have been developed for precast concrete, reinforced concrete, metal ductwork, piping, and other building systems.” BIM Handbook: A Guide to Building Information Modeling for Owners, Managers, Designers, Engineers, and Contractors, 2008

There is in fact so much profoundness and depth that BIM technology can be customarily designed to address specific firms’ needs. An example of this is BIM Services LLC, a private company that provides consultancy and customized BIM solutions:

“Other industries have recognized the need for product model servers. Their implementation in the largest industries –electronics, manufacturing, and aerospace —has led to a major industry involving Product Lifecycle Management (PLM). These systems are custom engineered for a single company and typically involve system integration of a set of tools including product model management, inventory management, material and resource tracking and scheduling“ BIM Handbook.

This has led to a naturally fragmented industry, which has had several implications. Firstly, sub-vertical domination due to network effects. Most BIM platforms allow for custom-made solutions, plugins, and integrations from third parties and companies’ developers. This way, a community of contributors is created, and the more contributors there are in a platform, the more builders will the platforms attract. Consequently, not only do the industry fundamentals allow for the existence of many sub-verticals, but also for virtual oligopolies/monopolies in each of these. The following is an example from Autodesk’s 2023 Investor Day.

Network effects are present in most platforms, and platforms with embedded network effects are known for their “winner takes all” characteristics.

At the same time, the fragmented nature of this industry has provided fertile soil for M&A operations. Given expertise and utility are mostly encapsulated within each vertical, companies can opt for acquisitions that could expand their platforms’ scope, by adding sub-verticals for example, increasing presence in sectors. In parallel, because of this immense depth each vertical software could have, plus integrations that would enhance platforms’ utility, managers can opt for adding depth. Examples from Bentley System:

For platform depth: “Adina R&D (2022), adds nonlinear simulation capabilities to users of our comprehensive modeling and simulation software portfolio for infrastructure engineering;” 2022 Annual Report

For breadth/scope: “Power Line Systems (2022), Power Line Systems substantially completes the reach of our comprehensive portfolio for the lifecycle integration of grid infrastructure across electrical transmission, substation, and distribution assets, and communications towers” 2022 Annual Report

To further illustrate how big of an emphasis is placed on M&A, the following chart was plotted for four players. At a 2022 revenue of 1.1bn, Bentley Systems has averaged spending 42.1% of its total sales in acquisitions, and has acquired 36 companies in the past 5 years (IPOd in 2020). Nemetsheck, with 2022 revenues of 858M, averaged spending 16% of sales on M&A for the period 2014-22. Autodesk, at over 5bn in 2022 sales, averaged 13%. Lastly, Trimble averaged 13% as well at 2022 revenues of 3.6bn. Regarding the latter, an acquisition went through in early 2023, in which Trimble acquired Transporeon for 2bn.

Multiple companies’ platforms have become quite comprehensive, but customers, generally, don’t utilize a high percentage of the portfolio offerings. At the same time, customers do not yet find the completeness of their problems solved by the same platform. Therefore, BIM businesses have addressed this issue by engaging with M&A operations to continue enhancing their solutions and ultimately capture a larger share of customers’ budgets.

“Our relatively numerous and frequent programmatic acquisitions, which most often “fill white space” within our ecosystem and add their particular value principally by virtue of our existing platform” BSY 2022

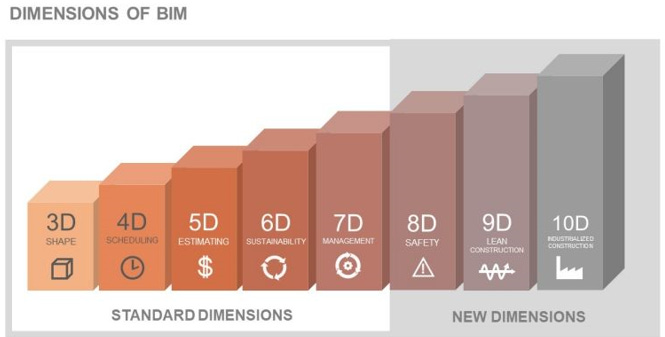

Additionally, companies might leverage acquisitions to extend lifecycle comprehensiveness. BIM technology can not only be employed for construction design, but also for stages that come before and afterwards. It might be the case that a specific platform was developed purely for 3D modeling and, as time went by, management added more capabilities so that it helps constructing companies throughout the whole process. Stages or phases of construction are nowadays known as BIM Dimensions.

Prior to turning our attention to “where does growth come from” in the industry, a pertinent observation. BIM technology is far from easy to utilize, learning curves are extremely slow, and complexity is directly tied to the platform’s purpose. One that’s meant for handling complex surfaces, such as Digital Project (owned by Gehry Technologies), will require much more training than a general purpose one, such as AutoCAD, under the consideration that the latter is not even fully parametric, which contains building applications like Architectural Desktop. What this implies, essentially, is that once a team gets used to utilizing a specific software, it is unlikely they will switch provider. The latter is further consolidated by the fact of leaders benefiting from network effects, making peers less appealing.

Lastly, within a project’s lifecycle, managers have always encountered friction when it came to managing resources and the workforce at each step of the chain. To address this issue, Enterprise Resource Planning software was developed specifically for the AEC industry. A business whose offerings revolve around this software is Procore Technologies. The company has seen a lot of traction, and multiple businesses have been started with the intention of replicating Procore’s offering. Hence this creates another avenue for acquisitions, something which Autodesk and others have already taken advantage of, as this article shows. Moving forward, it should be expected for these types of software to become either organically more comprehensive or for managers to inorganically expand their offerings, ultimately leading to a single consolidated platform.

Where Does Growth Come From?

The architecture, engineering and construction industry (AEC) had long been due for efficiency efforts. While most industries have seen their core disrupted and costs dragged down, AEC has been resilient to change. However, it has and will probably always be the case that, when a new technology emerges that allows for massive cost reduction, players adopt it. Beginning at the high end of the industry and going down, as the technology gets more efficient and less costly, so that more and more companies can afford it.

According to the BIM Handbook, A Guide to Building Information Modeling for Owners, Managers, Designers, Engineers, and Contractors, published in 2008, there are multiple benefits BIM brings:

Pre - Construction Benefits to Owner:

Before hiring an architect and putting things in motion, an owner needs to check if it makes sense to make the building from a quality and cost perspective.

Developing a schematic model prior to generating a detailed building model allows for a more careful evaluation.

Early evaluation of design alternatives using analysis/simulation tools increases the overall quality of the building.

Design benefits:

Earlier and more accurate visualizations of a design

Automatic low-level corrections when changes are made to design

Generate accurate and consistent 2D drawings at any stage of de design

Earlier collaboration of multiple design disciplines; shortens design time and reduces errors and omissions

Easily check against the design intent

Extract cost estimates during the design stage; More accurate cost estimates at the end and during the process

Improve energy efficiency and sustainability

Construction and fabrication benefits:

Synchronize design and construction planning. Allows to simulate and show what the building and site would look like at any point in time

Discover design errors and omissions before construction

React quickly to design or site problem

Use design model as basis for fabricated components. Accurate representation of the building objects for fabrication and construction

Better implementation and lean construction techniques. Minimizes wasted effort and reduces the need for onsite material inventories

Synchronize procurement with design and construction

Post construction benefits

Better manage and operate facilities. Helps to check that all systems work properly after the building is completed

Integrate with facility operation and management systems. A building information model supports monitoring of real-time control systems, provides a natural interface for sensors and remote operating management of facilities. Many of these capabilities have not yet been developed, but BIM provides an ideal platform for their deployment.

The above benefits range from pre-construction to post-construction, helping minimize errors of miscalculations and increasing efficiency and efficacy at all stages of the project. Furthermore, BIM modeling and simulation capabilities allow for accurate design and representation of future projects, making owners better assess whether a project should be done or not.

“The productivity gain for the documentation stage of pre cast and cast-in-place concrete structures has been measured in case studies and researched in numerous contexts, and has been found to be in the range of 30% – 40%.” BIM 2008 Handbook

Even though the results that come from utilizing BIM technology are overwhelmingly positive, a combination of its complexity, cost and reluctance from AEC companies, have led to an initially slow adoption. Over time, however, BIM penetration has increased across the developed world, with countries like the US, Canada, Netherlands and Australia exceeding 40% penetration.

The following chart illustrates, on the left, how adoption has trended for specific countries, comparing BIM’s 2020 penetration to the one it reached in 2023. On the right, the map shows, as of 2023, how high BIM’s overall penetration is in each region and country, ranging from 0 to 60%, with their pertinent color. Notice how there is a large portion of the world to which the technology has not yet arrived, and another big part where penetration is still below 20-25%. Moreover, almost no country’s BIM penetration exceeds 50%.

The still-low overall global penetration and the objective benefits BIM brings to the AEC industry should translate into very strong secular tailwinds for the coming decades. According to Zion Market Research, the BIM market is expected to grow at a compound annual rate of 13.9% from 2022 to 2030, reaching 52.5bn. The latter is largely influenced by how much efficiency this technology brings to an enormous market. Nemetschek expects the construction industry to grow 42% by 2030, reaching 13 trillion Euros. Penetration will continue to be further fueled by sophisticated entities’ demand of BIM-based projects.

Keep in mind that the estimated addressable market varies depending on how many verticals, use cases and end-markets are included.

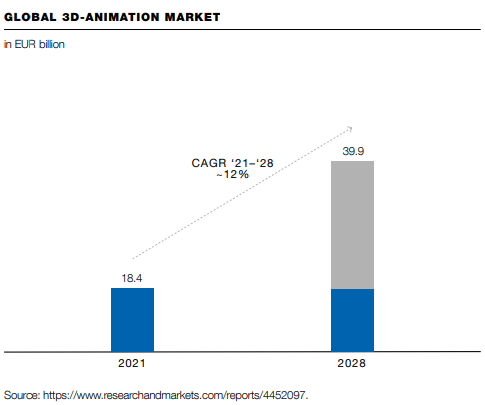

It should come as no surprise by now that applications of BIM software go beyond the AEC industry. The reason for this is that the technical characteristics with which BIM was designed allow for applications in more industries. Autodesk, for example, estimates an opportunity of 8.89bn in the design & make for media & entertainment by 2027. The expected 13.7% compound annual growth rate would be fueled by the increased demand for better virtual effects and 3D when producing content.

At the same time, and I’d say validated by Bentley’s recent actions, management foresees a 2.7bn market in the water design & operations industry, covering everything from drainage and water distribution to water treatment and retaining.

The last point I would like to raise is regarding how BIM technology allows for a better overall approach to construction. When it came to design, in accordance with the natural lifecycle of a project within this industry, companies had decided to overtake them by splitting the phases of development into sequential steps. Furthermore, when it came to designing the building, rarely were all future involved people included in the process. Alternatively, BIM technology allows for a much more collaborative approach, making more steps of the design chain be involved at a very early stage.

Having a more integrated approach towards design proves incredibly valuable for businesses since the moment at which managers have the highest ability to influence costs is at the beginning of the project. Afterwards, ability to do so becomes increasingly lower. The following chart illustrates how the design effort/effect curve shifts towards the left when taking an integrated approach, implying it offers managers not only higher ability to reduce costs, but also modify functional capabilities. Importantly, the later in the lifecycle this is tried to be done, the costlier it becomes.

“Leading architectural firms are beginning to recognize that future building processes will require integrated practice of the whole construction team and will be facilitated by BIM” BIM Handbook, 2008

Worth Mentioning Industry Trends

Lastly, before going into what I consider to be interesting companies to at least follow within this vertical, I’d like to point out some trends that have taken place during the past decade or more. These might be objectives multiple companies have been aspiring to attain or, otherwise, concepts that come up recurrently across investor days and annual reports.

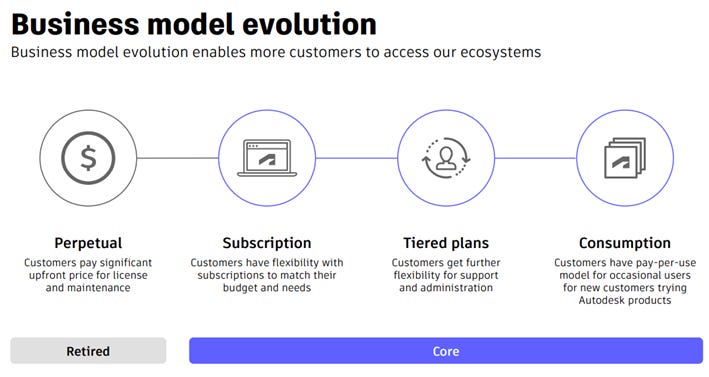

Revenue Model

Initially, BIM software began being offered as perpetual licenses, similar to what happened in many parallel verticals. This model implied for customers to buy a perpetual license of the software and utilize it moving forward. If they wanted to keep up to date with updates, they would need to buy the new license. Else, it was allowed for them to continue utilizing the version they bought.

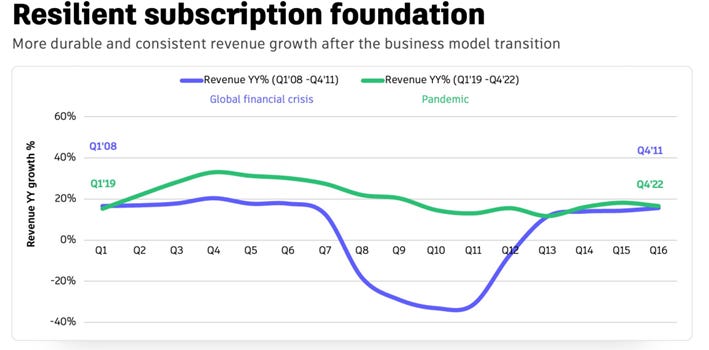

However, as time went by, managers started to notice that there was a world in which they could follow cloud giants by turning their business model into a subscription-based one. This is a recurrent pattern among businesses, including Autodesk, Nemetschek and Bentley Systems. The following image illustrates Autodesk’s case, which started to place from 2016 onward.

The SaaS business model offers companies a predictable stream of revenues, which they can leverage to better plan and invest. Moreover, customers are somewhat benefited due to the fact that subscription-based software allows the offeror to update it regularly, and for customers to get these marginal improvements as soon as possible. In Autodesk’s Investor Day, management shared how the new business model has led to resilience, which, given the software is mostly meant for a very cyclical industry, is somewhat desirable.

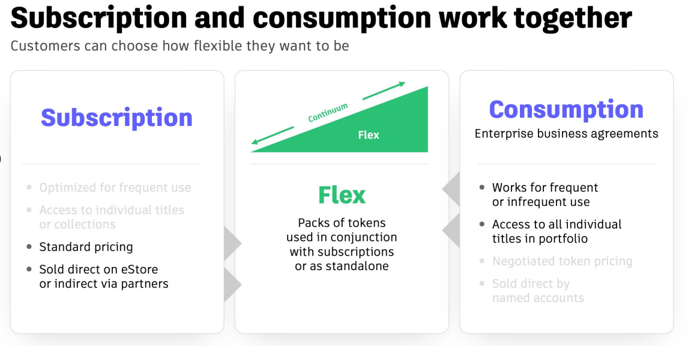

On the other hand, we saw that, even if companies now offer very comprehensive platforms, not many customers are opting for consuming everything from a single provider, or simply not at all. Nevertheless, it is in businesses’ best interest to capture a larger percentage of customers’ budget. Cross-selling tends to be a very attractive endeavor, from a financial perspective. To this end, a recurrent theme is to offer the BIM product and adjacent features on a flexible basis. Alike cloud computing, many of these are offered on a consumption basis, famously known as “pay as you go”.

“New commercial formulations. We continually innovate with new commercial formulations to align the use of our software to the needs of our users. Presently, we offer our subscription solutions by the day, month, quarter, and year. Additionally, we offer options enabling unrestricted access to our comprehensive software portfolio. We believe the flexibility in our commercial models and deployment options will allow our accounts to grow usage continuously” Bentley Systems 2020 Annual Report

Digital Twins

First and foremost, it is worth stating that the concept of “digital twins” is, broadly speaking, not new. The term has been utilized for a couple of decades now. Digital twins, essentially, imply for the virtual replication of a physical object and the dynamics encompassed within it. In some sense, it allows for not only a static replication, but also for simulations to foresee how would such object interact with its environment, hence why the “dynamics encompassed within it”.

Building Information Modeling, due to its functionality, has been understandably confused with what the term “digital twin” entails. The difference lies in the fact that the latter would suppose the virtual creation of the future (or current) building, and a model that should allow for the simulation of this building throughout its lifecycle. Further, how it interacts with the infinite variables of physical space. Foundationally, BIM models were developed with the intention of 3D design, not necessarily for simulation and prediction capabilities, nor for facilitating ongoing management.

At the same time, BIM platforms have evolved according to the increase in computing power capabilities, but this was implemented vertically. A parallel market, as mentioned earlier, was created. The software for project and asset lifecycle management have been developed almost independently from one another. Ultimately, a digital twin, as a consequence of its comprehensiveness, could in some way merge these separated markets to offer a more integrated one.

Autodesk

The company was founded in 1982 by John Walker alongside a group of programmers. The first product, which John helped create, is called AutoCAD (computer-aided design). The latter was a 2D software that allowed for the building and design of structures. The offering’s novelty and potential rapidly propelled Autodesk into success, selling tens of millions of dollars’ worth of software in a couple of years. As time went by, AutoCAD was improved. It now supports drafting in more dimensions and counts with hundreds of integrations.

Nowadays, Autodesk (43bn market cap) is the global leader in 3D design, engineering and entertainment technology. Customers utilize the company’s products for designing, visualizing and simulating potential outcomes of their project. Among the offerings, Autodesk discriminates among industries:

In the architecture, engineering and construction industry, Autodesk offers:

AutoCAD Civil 3D for ‘surveying, design, analysis, and documentation for civil engineering’.

Building Connected, a preconstruction solution.

Autodesk Build, ‘a set of project management and collaboration tools’.

Revit (Autodesk bought it in 2002 for around 130M), BIM for buildings

AutoCAD and AutoCAD LT. The latter makes it easier for sharing documents and collaborating on projects.

For manufacturing:

CAM (computer-aided manufacturing) Solutions includes a range of software that help manufacture, model out, and inspect complex products

Fusion 360 “is the first 3D CAD, CAM and computer-aided engineering (CAE) tool of its kind. It connects the entire product development process on a single cloud-based platform”.

Inventor is a set of tools that allow for 3D mechanical design, simulation, analysis and documentation. AutoCAD drawings can be integrated and, followed by further instructions, it allows for the virtual final representation of the product, prior to building.

Vault is Autodesk’s data management software

For media and entertainment:

Maya is a software that provides 3D modeling, animation, and effects, helping to create high quality content (films, videogames, animations).

ShotGrid is a ‘cloud-based software for review and production tracking’.

3ds Max is for modeling, texturing, shading, lightning and rendering. Could be seen as a complement to Maya and both are offered in the Collection.

Autodesk is a business that has a great breadth of products, with exposure to most industries and end-markets. This allows the business to “pack them” and offer them as “Collections”, which encompass a great deal of solutions, addressing all of customers’ problems. This general-purpose approach is what differentiates it from most competitors and, given the technology’s characteristics, Autodesk should continue to lead.

Given its first-mover advantage in many sub-verticals, it holds the leading position with around 60% market share in the CAD market and 65% in the BIM software market, according to 6sense. This translates into the business having finalized their FY23 with over 5bn in revenue. Autodesk’s dominance is natural due to the aforementioned industry and technology fundamentals, which allows the company to have high degrees of pricing power.

“The companies interviewed (from a letter from architects to Autodesk) claim that their costs for licensing Autodesk products increased by 70% between 2015 and 2019 alone” Article

Furthermore, this is a company that has taken advantage of circumstances and continuously adapted to what were seen as positive trends. For example, in 2016, Autodesk made the ultimate decision of turning their business, in its completeness, to a subscription-based one. The decision temporarily depressed Autodesk’s revenue and margins (there’s still not complete optimization here), but led to much more resilience.

The final point, and what I believe should be looked at carefully moving forward, is Fusion. Historically, a big concern customers have had regarding BIM technology was its affordability and the lack of a unified offering. Fusion aims to fill both gaps in the manufacturing space. In 2013, Fusion 360 was launched and, since it is cloud-based, it also allows for seamless collaboration and document sharing. The unique value proposition Autodesk Fusion entails led to rapid adoption and growth. It now has 223,000 subscriptions, which have grown at a 40% CAGR over the past 5 years.

Nemetschek

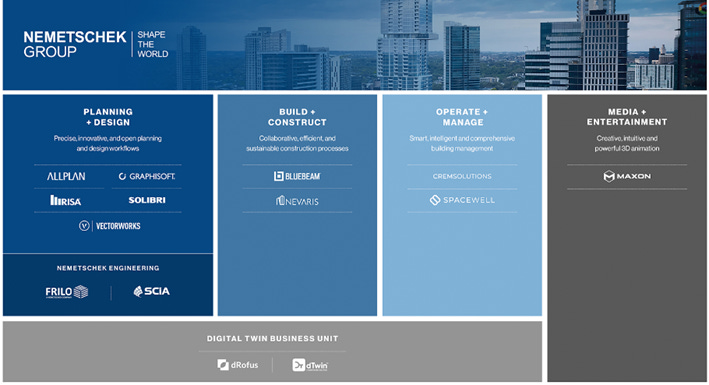

Nemetschek Group was founded by Prof. Georg Nemetschek in 1963 and was initially focused on structural design. In 1980, the company presented the first software that enabled computer-aided engineering (CAE) on computers. With the pass of decades, Nemetschek expanded operations internationally, acquired several companies, and has broadened its scope of offerings. Nowadays, the company’s market capitalization exceeds 9bn dollars and reported revenues of 858M in its last fiscal year (2022). The company is comprised of 13 brands, which are allocated in four different segments: Design, Build, Manage and Media.

Even though the approach taken resembles that of Autodesk, in the sense that management’s intention seems to be to cover as many end-markets as possible, and to cross-sell with recent signals of a unification, the first difference lies at the corporate structure level. While Autodesk is a classic example of a hierarchical structure, Nemetschek takes a much more decentralized stance. The latter is the parent holding that encompasses these 13 different brands. Even though it makes sure synergies are exploited, each subsidiary is independent, having its own management and goals.

In line with its competitor, Nemetschek switched to focusing on a subscription-based business model. As of the latest fiscal year, recurring revenues represented 66% of the total, up from 43% in 2016.

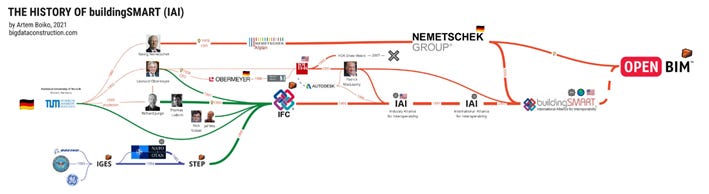

When speaking about BIM technology, a characteristic that helps differentiate them is how interoperable they are with other software. A closed approach implies for the business to offer an interdependent and closed ecosystem, which is what Autodesk mostly does. On the other hand, Open BIM has been getting traction for the past 15 years, with Nemetschek leading the way. In the AEC industry, Autodesk’s Revit competes with Nemetschek’s Archicad, which got into the Group when it acquired Graphisoft in 2006. Industry efforts have led to developing standards for ensuring interoperability.

Finally, Nemetschek shared a chart and estimate that reveals the huge potential that there is to uncap in the media & entertainment industry. On this occasion, both Autodesk and Nemetschek take the open approach. What might define whether or not the winner is among the two is how well is Nemetschek able to integrate an M&A they did in 2019, Red Giant. The media market is the one expected to expand the most in absolute terms, potentially causing the winner to outperform peers.

“This merger is a major milestone, not only for Maxon and Red Giant but also for the design industry as a whole,” says David McGavran, CEO of Maxon. “Our combined technology and know-how have the potential to progressively reshape the content creation landscape for years to come.” Nemetschek press release

Mensch und Maschine

Mensch und Maschine (MuM, 907M market cap) is a German company that was founded in 1984 by Adi Droftleff, who still serves as Chairman but is no longer involved in daily operations, with the original intention of distributing Autodesk’s CAD software, which had been just released. Nowadays, MuM Software SE is structured as a holding company, which, underneath, has MuM Management AG, that overtakes management and service tasks. The active operations are performed by approximately 40 direct and indirect subsidiaries, with 1031 employees and 75 locations worldwide.

Mensch und Maschine is composed of two different segments. On the one side, it continues to be a direct distributor of Autodesk’s software to customers. It is important to note that MuM’s distribution encompasses value-added features as well, which is why it’s called Value Added Reselling (VAR):

“The second growth driver are customer specific digitization projects, in which standard software modules are connected to individually tailor-made project solutions, adding functionality where necessary.” 2022 Annual Report

At the same time, it develops and distributes proprietary software. As of 2022, the Value-Added Reselling business generated 70% of total sales, whereas the proprietary software the remaining 30%. Interestingly, the software operates at a 26% EBIT margin, while the VAR segment at around 8%. MuM’s margins have been expanding for the past couple of years due to the software segment gaining share of overall sales.

Alike its peers, Mensch und Maschine has been engaging in M&A operations during the past couple of decades. In some cases, the company built stakes over time. This way, MuM has expanded its portfolio of proprietary sold software and continues to do so. For example, in 2019, it increased its 13.3% position in SOFiSTiK to 51%. Nowadays, the group’s software segment is composed of four subsidiaries:

Open Mind (Computer Aided Manufaturing). Their solutions are for the “process control of milling, drilling and turning in various industries”. Open Mind is MuM’s biggest software business, with annual sales of over 50M. The average workstation costs around 30 thousand dollars. It is sold at a high price because of the extreme precision and efficiency at which it operates, helping customers get a “quick payback of their high machine tool investments, which are typically in the six to seven digit range”. Open Mind software is compatible with leading CAD products.

DATAflor. Its solutions are utilized “by landscape architects for the graphic and financial planning of green areas”. DATAflor has been around since 1982 and is one of the leading providers in the German-speaking area.

M+M Mechatronik specializes in solutions of control, robotics and mechatronics for the market of automated industrialization.

SOFiSTiK serves the construction industry by developing and providing software. Some of its products are extensions to other companies’ software. For example, SOFiSTiK Bridge + Infrastructure Modeler is an extension to Revit. Furthermore, it is “the only solution for BIM design of bridges and tunnels in Revit”.

In contrast to its competitors, it is unclear whether Mensch und Maschine is placing emphasis on turning their business into a subscription-based one or not. Their VAR business necessarily implies the continuous re-selling of Autodesk’s products to new customers. In MuM’s 2015 annual report, they disclosed that around 30% of their VAR sales were recurring services they needed to provide. Moreover, their proprietary software segment seems to be sold both on a perpetual license and subscription basis.

Conclusion

BIM technology and products that have derived from 3D modeling are utilized in a wide array of industries, not only AEC. The company that almost completely dominates the market is Autodesk, which holds over 50% market share in the main verticals. However, it is important to note that the details with which the software can be developed are infinite in some sense, therefore allowing for the existence of very niche products.

Autodesk’s general-purpose technologies would be the clear winner if we are speaking at a broad level. The network effects they carry should, I think, continue propelling and maintaining their dominance. Moreover, the fact of Autodesk’s portfolio being so comprehensive is what allows the business to take a “closed” BIM approach when it comes to the main verticals in the AEC industry.

Nemetschek is a business that, like Autodesk, possesses a broad portfolio of offerings. However, generally speaking, the group is aiming for open BIM technology, allowing for cross-interoperability with other software. The strategy should yield handsome results if more solutions are developed. Historically, industries have naturally tended towards modularity, for which there’s a slight probability that this happens in this one as well.

Mensch und Maschine operates as a distributor and value-adding partner of Autodesk, and it is a software provider. The first of both businesses has very low margins given the fact that they re-sell (charged for the license) and adapt Autodesk’s software to specifically address customers’ needs. Business models with this custom-made characteristic are known for the high associated costs. On the software side, MuM owns several players in niche markets.

My sense is that the safest company to bet on is Autodesk, though I suspect the three of them will inevitably capture a great deal of the expected industry growth. I think Autodesk seems the safest, on a modest time horizon, because its products are mostly the ones developers continue to learn in universities. The perhaps riskiest one, without being risky, is Nemetschek, given the completely different approach taken. Time will tell whether or not the industry tends towards the open approach.

Finally, I believe the best risk/reward investment might be Mensch und Maschine. This is due to the fact that I do not think Autodesk will replace it as a distributor nor it will do the job itself. Going after MuM’s low margin business would make no sense for Autodesk, considering the complexity element of doing so. Furthermore, margins should continue to trend upwards for MuM as the software business continues to take share of total sales. Finally, I think niche products like the hyperMILL, offered by Open Mind, will not get displaced at the high end of the market from products such as Fusion 360.

Keep in mind I’m speaking at the fundamental level, not about current prices.

Personal Commentary

This is the last research article I post for free. Most likely, I’ll cover one of this companies in depth in future research. Thank you very much for reading.

Contact: Giulianomana@0to1stockmarket.com

Disclosure: This is not financial advice and shouldn’t be taken as such.

gracias lo agradesco mucho saludos

excelente trabajo muchas gracias