In the three previous articles, we learned most fundamental principles needed to build a portfolio (some of them are for future articles, like how to read financial statements, a 10k); Risk Profile, Risk Return Curve, Volatility/Beta, How to Screen and How to Research. Today, it will be about an example of an actual portfolio (not mine).

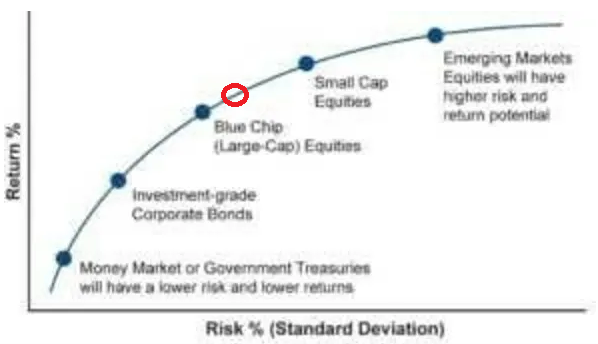

First, the investor’s Risk Profile had to be determined. According to his horizon, income, liquidity needs, insurance and emotional risk aversion, it was inferred the investor’s Risk Profile was somewhat conservative.

Given his theoretical position on the curve, the next step was to find the highest quality companies and weighting them for that the overall portfolio ‘risk’ to be near the selected spot. As expressed in Portfolio Building Part 3, we based the stock selection on:

Mission Statement

Thesis

Industry

Management

Financial Soundness

Competitive Advantage

Historical Performance

Risks

What do we arrive to?

Portfolio’s Financials:

Thesis and MOAT:

Many of these companies have multiple competitive advantages as well as multiple parallel thesis playing out. To keep it short, I tried to select the strongest MOAT out of the most promising individual service or product the businesses provide.

When thinking of weights, I generally think of two things:

Resiliency

Future Growth

It would be nothing but logical to want exposure from those secular trends one believes will drive the most economic growth for the different countries. Once identified these trends, it is about looking for the best positioned company to capture the most possible growth out of them and which have shown resistance on turbulent periods. Resiliency could be inferred upon historical financials of the companies and their current stance, as well as the strength of their competitive advantage.

Among the industries I’m most confident looking forward are:

Cloud-based products

Cloud Computing

Semiconductors

Mobile

Advertisements

Electric Vehicles

Digital Payments

AI, Robotics, RPA

E-commerce

Then it should come as no surprise why Google and Microsoft would lead this theoretical Portfolio. Google acts as a portal to the two most used technologies that are continuously driving spending; Mobile (Android) and Internet (Google Search). The company has multiple apps with hundreds of millions and some of them with billions of active users.

This makes it count with probably the largest 1st party data base in the whole world, making its advertisements the best at targeting audience. In parallel, many applications play by themselves their role in other secular trends. Lastly Google is the third largest player and growing rapidly in one of the most promising secular trends for the decade, Cloud Computing.

On the other hand, Microsoft has exposure to many cloud trends and, secondarily, hybrid work trends. The company counts with the second largest player in Cloud Computing, Azure. It has the most used hybrid work tool, Teams, and at the same time it owns the portal connecting companies with employees, LinkedIn. Microsoft also owns Windows and the whole Microsoft Packages, the most used professional tools. It has a dominating dev tool, GitHub. And, as if all that wasn’t enough, the company has been migrating to a much more resilient business model:

If interested in further information, check this tweet:

These are the sort of things that could be contemplated when deciding how much to allocate to each position. A case like both of this could be made for every company included in the portfolio. Probably in the future, a deeper dive will be published regarding each business. At the moment, the two published research are on:

Accenture:

ASML:

Personal commentary

This is NOT financial advice, take it as information. The objective of this article is not to provide you with a portfolio, but to help you think of what could be contemplated when building one.