Looking for a job

I’m studying for a Master’s degree at Brandeis, in Boston. I’ll be graduating in May of 2024 and looking for a job in a long-only equity fund, in the line of the companies and philosophy I follow here. If you know of anything, I’d really appreciate you letting me know.

Contact: giulianomana@0to1stockmarket.com

Article

I usually try to escape writing about the obvious. There is little incremental value I can add on widely covered topics. Moreover, given they’re mostly well-known, it is very likely that you are already familiar with them, which makes reading another article about it, a partly waste of time. That’s the reason why 90% of Sunday articles are about subjects I find curious and the approach I take is a purely personal one. It’s what I remember or understand. Probabilities of publishing something that’s somewhat novel increase dramatically under such conditions.

When I read Nick Sleep’s letters, back in March, I only wrote one article about them. His writing is so peculiar and delightful it was very difficult to grasp the essence of his philosophy. Nevertheless, there was a concept I knew many people were familiar with, which should’ve been a must-share, but, honestly, I didn’t really understand it.

Being familiar with the subject allowed me to have some conversations around it and these past weeks I’ve been talking to a friend that’s very well read and is familiar with Nick’s ideas. He explained to me the concept, which almost immediately triggered an unbelievable connection.

Scale Economics Shared

Nicholas and Zakaria, at Nomad Investment Partnership, came up with the description of a business model. They noticed a pattern among some very successful companies and were able to put into words what these were doing. Furthermore, their fund was known for its highly concentrated positions, with most capital being allocated within this small universe of companies that had this business model.

Scale economics shared imply for a company that, firstly, benefits from scale. The latter would be in the form of operating leverage, expanding margins, product of very high upfront investments and not necessarily high variable costs. Then, what these companies do is to pass this scale advantage to its customers. They prefer for their margins to not expand by lowering prices and, instead of making extra profit, it is customers who get to save more.

“Scale economics shared operations are quite different. As the firm grows in size, scale savings are given back to the customer in the form of lower prices. The customer then reciprocates by purchasing more goods, which provides greater scale for the retailer who passes on the new savings as well” Nick Sleep, 2008 Letter

“Our judgment is that relentlessly returning efficiency improvements and scale economies to customers in the form of lower prices creates a virtuous cycle that leads over the long-term to a much larger dollar amount of free cash flow” 2006 Letter

“For example, it is interesting to note that the business model that built the Ford empire a hundred years ago and is illustrated in the chart below (dated 1927), is the same that built Sam Walton’s (Wal-Mart) in the 1970s, Herb Kelleher’s (Southwest Airlines) in the 1990s or Jeff Bezos’s (Amazon.com) today. And it will build empires in the future too.” 2012 Letter

It was not until after a year of writing about Tesla and 4 months of studying disruptive innovation that I couldn’t go further in this line. But I think there is something here.

Why does it work?

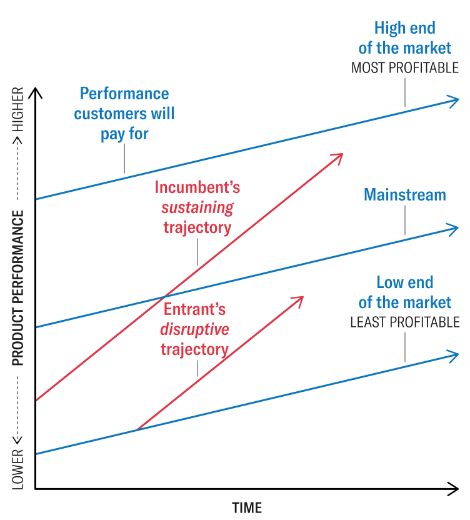

The Innovator’s Dilemma tries to answer why do good firms, led by good managers, fail. Paradoxically, it is the pursuit of profit what makes them fail. Companies begin either at the low end of the market or in a new industry, producing for previously non-consumers. What happens afterwards is that these new companies tend to perform sustaining and efficiency innovations until they perish, under the pressure of a new disruptive company (which could happen after generations). It is the classic upmarket movement we’ve gone through over and over.

This logical strategy is deeply flawed. By focusing on higher margin products, on higher tiers of the market, companies neglect low end customers. They overshoot them in terms of performance they need, creating a gap that a new disruptor can fill. Nicholas’ scale economics shared business model would suppose a change in the disruptive technology’s trajectory.

I think this would imply businesses to stay at the low end of the market forever, which does not necessarily mean there’s no profit there, making the trajectory flat. However, it might also be the case that, because these efficiency innovations are being passed on to consumers, the company behind such a process may be continuously altering what the low end of the market represents. Each time it saves customers’ money, it brings the low end of the market lower and lower.

I’m still not seeing it very clearly, but I would suppose this not only fills all gaps that would give room for disruption, but also discourages new entrants for coming to this market.

Personal Commentary

I absolutely think there is something here, but I need to read and think about it a bit more. I’ll try to re-read Nick’s letters in the coming months and see if I can take this a bit further. Hope you enjoyed the article!

I'm reading through the Sleep letters now.

Any one can try to disrupt anything. Sleep points out that competitors have a vast moat to cross in terms for building a loyal base of customers (Costco Members and Amazon Prime Members), that the companies are not idle and are changing their competitive stance as you attempt to disrupt them. The widest moat is mental: getting the attitude right for passing through savings. Sleep shared: "To understand how important Every Day Low Price is to Jim Sinegal, the firm’s founder, consider the following story which was recounted to us by a company director. Costco bought 2m designer jeans from an exporter and shipped them into international waters and re- imported the jeans for an all-in price of U$22 or so per pair. This was U$10 less than the firm had sold the jeans for in the past (offering the potential for a 50% mark-up) and half the cost of most other retailers. One buyer recommended taking a higher gross margin than was usual (i.e., more than the usual 14% mark-up) as no one would know. Apparently Sinegal insisted on the standard mark up, arguing that if "I let you do it this time, you will do it again". The contract with the customer (very low prices) must not be broken."

Thanks for the insights. If Costco and Amazon are examples of scale economies shared, do you mean that these cannot be disrupted?