Mid-2024 Shareholder Letter

Performance and meditations on portfolio management

Shareholder letters compose the space wherein I communicate the evolution of my investment philosophy. I mistakenly believed that last year’s depicted my approach as an investor, but it was merely an exposition of elements widely recognized and reproduced. It consisted of what makes for a good business and the soundest strategy I’ve read of. Onward, in these writings, I will explore the ideas that have captivated me the most, portrayed as most promising to apply in this endeavor. Additionally, I will try to articulate, to the best of my capacity, how I think, which I believe is instrumental to communicate.

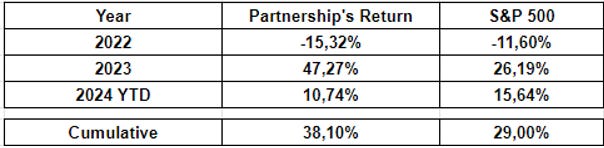

The portfolio finalized the first semester of 2024 with an accumulated return of 38.1% since its inception in late January of 2022. Although I’m indifferent about how indexes perform, they do provide an approximate yardstick with which results can be contrasted. The following table illustrates the portfolio and S&P’s performance on each calendar year as well as accumulated.

Note: Interactive Brokers has an error when calculating period returns, which we are investigating. The only reality is the dollar amount with which we started in 2022, 20% of which was added in May/June of that year, and the dollar amount as of this writing. Cumulative returns are based on these two numbers, whereas yearly periods are partially approximated with given information.

Even if analyses behind decisions are correct, time is required for results to manifest their rightness. Within short time frames, the portfolio can underperform the index. In fact, it will do so more often than it may be believed. The only metric I try to optimize for is returns since inception 20 years out. Having a basket of 500 companies outperforming the selected businesses on a price basis over 6-36 months does not concern me. If the thinking is right, results will follow. In other areas of life, immediate whims and desires need to be postponed for improving the prospects of long-term outcomes.

Continuous outperformance throughout calendar years is virtually impossible, unless the portfolio manager is unbelievably unique. Over the past 100 years, there may have been less than five people like these. Impossibility being the case, trying it implies wasting effort. It represents a tradeoff of not learning anything valuable in exchange for worse results than could be obtained otherwise. I candidly encourage you to distrust commonly held practices, for the latter provide, by definition, average results, or worse.

Risk and Man’s Problem

Risk embeds a fascinating concept. It is vividly elusive, undefinable in the final analysis. This is a strong disadvantage for a species that likes to characterize themselves as superior because of their intellect and scientific advancements. Historically, and more pronouncedly over the past 450 years, mankind has fallen in love with mathematics, and rightly so. We try to reduce everything to a single number. Taken to the extreme, I believe this to be a dreadful practice, which has affected people’s thinking.

Man cannot live with uncertainty. Anxiety and stress are rapidly triggered, both of which cause deep suffering. I profoundly understand how good of a patch numbers have acted as in this respect. Suddenly, answers pop up. Numbers are taken at face value. They now fill all voids that emanate from uncertainty. The investment community has psychologically benefited from this phenomenon. However, it has been at the cost of performance, in my opinion.

My job is not to pay tribute to my consciousness by maintaining it in the comfort zone. I have concluded that being “remorselessly rational” will yield the best results for the capital under management. It is very curious to observe the illusion that commonly held beliefs portray. We are inclined to suspect that what’s approved by society has been necessarily subjected to critical judgment and is therefore rooted on rationality, making it “true.”

Studying Darwin’s Origin of Species has confirmed a former suspicion of mine. Before his masterpiece was published in 1859, mankind believed in the independent creation of species. Only after scientists witnessed the demolition of each of their arguments could they accept that they were wrong. Darwin spent 20 years carefully preparing the layout of his theory, for he knew that people are reluctant to change their minds.

I cannot afford to seek refuge in commonly held beliefs if they are detrimental to obtained results. Therefore, it has been my job to understand what are thought of as good practices for portfolio management and business analysis, and critically question them. I try to conserve those that objectively work and eliminate the ones that do not. Metaphorically, I’m intending to build a mind capable of recognizing the potential truthfulness of natural selection in a world that thinks otherwise and bets accordingly.

Richard Feynman helped me get further in this line of thinking. In Cargo Cult Science, a speech he gave at Caltech in the 70s, Richard speaks about pseudosciences; those disciplines and areas that seemingly follow scientific practices. Notwithstanding their effort, false conclusions are drawn. Shady premises coupled with dubious assumptions converge into flawed analyses. Problematically, because of how well they cover a defective core, people think their results are true. Richard spoke about how difficult it is to truly know something, consequently leading to only a handful of things being really known. Higher degrees of certainty can be achieved through experimentation and theorization, but certainty is almost never reached.

When it came to risk, I found no useful framework. The investment community twisted the concept, leveraging its elusiveness, to a certainly appealing point, but neither true nor useful. I’m inclined to agree with some experienced investors who define risk as it is colloquially referred to. Risk represents the possibility of something going wrong. Overextending beyond this broad definition has been a massive mistake. The first and only step I may agree with taking is assigning probabilities to things going south. However, I do recognize that, even though this implies assigning a number, one has to be aware of its profound inaccuracy. An appropriate risk management strategy may lie between both ideas.

I believe to think about investments and weights as a reflection of the number of questions I am able to answer. Good investing is unequivocally a form of foreseeing the future, for businesses’ value depend on their future. The only mechanism by which I believe risk can be reduced is by sorting out potential future states of nature, therefore by thinking.

“Risk is what it’s left after you think you’ve thought about everything”

I suspect this realization is what caused a detour and twisting of the concept. Living with such uncertainty is deeply daunting. Furthermore, it transforms an investor’s job into a purely intellectual one, whereby the investor doesn’t show any work on an ongoing basis. Ideas and “potential states of nature” are impossible to reduce to even a set of words, creating an immense obstacle. With unguaranteed results and complete exposure of one’s mind, it’s a frightening path to take.

Burford Capital

For it is my belief that I will carry on with this endeavor for a long time, I needed to think about how to optimize returns for the long term. When I expanded my investment horizon by ten years, I realized some of the held companies’ expected above-average growth would cease, thereby threatening returns. More importantly, the philosophy I made use of to purchase businesses in 2022-23 was opportunistically right, but it may be condemned to underperformance if maintained long enough.

Investing is an incredibly and increasingly demanding activity. By definition, repeatable things that yield good results do not last. In this line, the spread of information has helped investors to more rapidly recognize high quality companies. Therefore, the latter become overpriced or fully priced most of the time. Some occasions may arise when they get repriced substantially lower. Incidentally, these may represent the only times when buying these businesses is a good idea. However, it is not that clear to my eyes.

Purchasing after some of these declines still implies buying an asset that is priced for lasting two decades at least. Carefully deliberating over this presumption has perplexed me. Capitalism embeds a system that makes thriving very tough. Eternally sustaining success is impossible. It is a question of when will domination stop, not if. Likewise in nature, species show a period of gradual increase, and a subsequent one of decline. Competition between organic beings highly resembles that between businesses. Enduring is virtually impossible and requires unusual aptitude.

Realizing this terminal problem forced me to re-think the whole approach taken. I believe a new one needs to be built. Although I performed my own analyses on held companies, it is extremely simple for the mind to hide behind other investors’ view, biasing one’s own in the first place. Burford represents the first investment where the analysis performed has exclusively personal inputs. Independent mindedness complemented with good business sense are crucial for succeeding in investing. Incidentally, both need to be cultivated, and I believe experimentation is required. Otherwise, lessons and skills are not tested against reality. The lack thereof impedes growth, terminally condemning an investing journey.

I will inevitably be wrong, probably more frequently than not. It is my responsibility to think about the risk present in decisions made and limit the extent to which it affects performance. Burford, therefore, provides an interesting example of how risk is accounted for in the weight I assign to companies.

Investing is about betting on how an ecosystem may evolve. Within the whole activity, we may speak about two ecosystems. Broadly speaking, investing is one, while the world surrounding specific companies could be another one. Each of these are different composition of variables. It is an investor’s job to assess the relevance of each variable and, more importantly, their knowability. Some things are incredibly important, but ultimately unknowable. Destining time in trying to figure them out is not only futile, but value-destroying. The opportunity cost of time and thought is infinite. Time wasted in this quadrant could be employed in learning and trying to know variables that can be known in the first place. I’m further inclined to believe that one has to choose, among unknowable variables, the ones which are, in some sense, feasible to approximately determine.

When speaking about a specific company, the ultimate question that matters is how much it is worth, which depends on the future cash flows it will produce. In what I believe I use as framework, the degree of certainty with which I can answer this question determines the weight I place on the bet. If I do not know what a business does, what types of assets it has, how management has historically allocated capital, what are the industry’s future prospects, I have no insight whatsoever as to how much could the company be worth. These are all knowable variables around which questions arise. The more I can answer, the higher the perceived certainty of the value estimate.

After confronting numerous questions, I decided for Burford’s weight to be 6.5%. Partly because my judgment has not been fully built is that I try to be overly cautious. Furthermore, there are two specific questions that could severely alter multiple of Burford’s future states of nature. I have not yet satisfactorily answered any of both. A successful response materially increases, in my mind, the likelihood of the foresaw cash flows occurring, thereby allowing my understanding to bet more heavily.

One of the questions is “why should legal finance exist in the first place? Does it actually benefit society?” An interesting idea is that only net positive industries and businesses endure the long run, or at least they have it easier to. Jonathan Molot wrote a paper in 2009 titled “A Market in Litigation Risk,” where I found a reasonable answer to these questions. Notwithstanding this, I currently lack the knowledge to objectively assess the validity of the argument. The second question is “how could regulatory changes affect Burford’s business?” This is an unbelievably obscure question, to which I cannot shed much light.

These matters are of the utmost importance. If I counted with a satisfactory answer to both questions, maybe the maximum weight I would place on this bet could be 15%, if the discrepancy between value and price justifies it. The two themes play a major role in the industry and company’s future cash flows, for they strongly alter their durability, quality, and actual occurrence.

Why 15% and not a higher or lower weight is the other topic related to risk that I believe I account for. I would argue that the distance from 0% to the assigned weight reflects the degree of certainty with which I believe I can estimate a business’ value. The distance between the assigned weight and 100%, which would mean investing the entire portfolio, represents an estimate of how many important questions I think I’m missing.

The number and quality of questions depends entirely on how much I know about a business. For I do not know everything, there are certainly important topics that could affect the investment about which I haven’t thought. Therefore, the 85% in this case would constitute the things that I don’t know that I don’t know. The distance between 6.5% and 15% accounts for the things that I know that I don’t know.

An interesting thinking exercise is to play around the idea of knowing with certainty what a company’s cash flows will be. In this case, it would be like estimating the value of a bond, which can be done quite precisely. Under some assumptions and leaving aside other considerations, why wouldn’t one bet 100% of their portfolio on such an investment if it offers desirable returns? For it is impossible to reach such a level of information, the maximum weight will account for how far I feel I am from that threshold.

Aiming for Less

It has become evident how difficult investing is. Even though recent periods may incline one to argue otherwise, I’d expect a reversion in perception. Once difficulty is recognized to be widespread, the importance of thinking is enhanced. Deciphering and solving these intellectual puzzles compose a large part of my job. I must observe that a purchase decision needs to be also accompanied by a discrepancy between value and price. One would want to buy an asset for as little a percentage of what it’s worth as possible, for good investing is receiving value in excess of what it’s paid for.

Investment opportunities whose expected returns are attractive do not emerge very frequently. Reading and meditating over the sophistication behind the pricing mechanism and how wise crowds are helped me form some hypotheses. The market is efficient most of the time.

Having there only been a minority of companies that performed exceptionally well and another minority that has done above average rapidly helps conjecture that all opportunities analyzed cannot possibly offer good future prospects. I’m currently inclined to believe that frequently “finding” attractive opportunities is the result of a flawed analytical process. Being as close to certain as possible in the analysis performed is immensely demanding. I would, nonetheless, expect it to get “lighter” with experience, for discarding should get easier.

I’ll be prone to acting only rarely. In pursuit of risk minimization, decisions will only be made in high degree of certainty territory. Certainty of returns obliterates potential returns from my perspective. This will cause me to ignore businesses that end up performing very well, but whose future prospects I’m not able to evaluate. Incidentally, these do not concern me.

Including low-quality businesses or overpaying for one are massive, but avoidable, mistakes. The fundamental aspect of this strategy consists in avoiding as many mistakes as possible. Weighting according to the degree of certainty with which the decision was made is what makes this a viable strategy. If all decisions were equally weighed at, for instance, 1% of the portfolio, it is illogical to adopt this strategy.

From a practical standpoint, I spent four months deeply reading, writing, and thinking about Burford as an investment. Naturally, it is still the company I meditate most about. One would be initially inclined to disqualify such a process. But, theoretically, how much time would it be worth spending on getting to 100% certainty, which would allow one to allocate 100% of their capital? Time employed reading and thinking is time devoted to climbing in the scale of certainty. The objectively farther one can go, the more weight can be placed on the idea at no incremental risk. Maybe risk even declines.

Simplicity

Earlier this year, I decided not to invest in an industry whose fundamentals I couldn’t fully understand, namely Building Information Modeling (BIM) Software. In contrast to Burford’s research, after reading and writing about how BIM software works and going through companies’ annual reports, I couldn’t yet understand the technicalities behind the technology. It is my belief that extreme attention needs to be paid to true fundamentals, which applies to business analysis, learning disciplines, and all endeavors wherein one intends to perform appropriately.

Humans have longly admired complexity; I certainly find it captivating. Fighting against this tendency, which otherwise gets to a systematic cause of misjudgment, is an arduous task. This caused me to delay the decision behind not investing in this industry, which is a mistake I am trying to learn from.

I believe everything can be learned. Depending on the subject, more or less time needs to be dedicated. It was very rapidly that I was struck with how complex BIM software is. Reluctant to accept my incapacity to rapidly understand it, I kept reading and researching for 2-3 months. I don’t consider this to be wasted time, for I learned about engineering, physics, and software, but I believe I could have utilized time in higher-returns learnings.

The concept of a “too hard pile” may be the one I struggle the most in implementing. Two elements ultimately matter, namely: (i) the cash flows a business will effectively produce; (ii) how much one pays for the business. Cash flows are industry agnostic. They are either generated or not. There is no correlation between complex operations and increases in cash flow. In fact, complexity may provide more room for committing mistakes, translating into lower levels of cash flow.

Similarly, when building an investment thesis, there may exist an inverse relation between the difficulty with which it is articulated and future returns. Complexity could cause a specific asset to be inefficiently priced. Nonetheless, I believe it is almost impossible to utilize this as an edge. Deep understanding requires strong formation in certain disciplines and topics. Developing expertise takes time. It is very likely that, while an investor is devoting time to building expertise for exploiting a situation, the asset gets efficiently repriced in this regard.

Striving for simple is highly counterintuitive and, ironically, difficult. It needs to be earned. Struggle and effort must precede it. The illusion that unearned simplicity creates is unmeasurably damaging. True and deep understanding are rare. They are forged by reading and thinking. I haven’t found a way to bypass the intellectual combat that’s required for understanding something. However, oneself is the easiest person to fool, thereby facilitating one’s access to delusionary territory. I believe that drawing conclusions while standing on this faulty soil is a massive but commonly made mistake.

For the reasons laid out in the foregoing paragraphs, I’m trying to make simplicity one of the pillars upon which the investment philosophy is built. Demanding its presence in decisions drives a large part of the thesis behind making only a handful of them. The investment opportunity needs to scream obviousness. Being capable of detecting these when the investment community misses them is what I am working on.

“Pick problems you can solve”

Building Judgment for the Long Term

Thinking about capital allocation as a decades-long journey severely changed my perspective. With my current knowledge and understanding, it would be arrogant and ludicrous to believe I can do well throughout time. Even if already-taken decisions fare well over the coming 5 years, I strongly doubt their endurance. This being the case forces me to think five years ahead. How can I allocate capital appropriately once past-decisions fuel runs out?

Unequivocally, I suspect the core element behind long-term success in this endeavor is having a good judgment. Recognizing this has little merit. The difficulty lies in building it, for not even successful investors can deeply break down how they do it. Behavior and decision-making are untransmissible in their ultimate form.

The mechanism I will utilize to, hopefully, build a good judgment is simple: I will make decisions. To enhance learning and improve my analytical skills, I will emphasize independent thinking, or as much thereof as I can. If external inputs are to be found in a buying or selling decision, it is likely for the mind to hide behind it, thereby providing a perfect element for avoiding accountability. However, it is the latter that drives improvement.

Making decisions therefore exposes oneself to this huge disadvantage. Incidentally, I believe this to be the subconscious reason why most people eschew the task altogether. Furthermore, and more critical, if the person whose inputs are tested does not count with expertise on the subject, decisions will inevitably be mediocre. For I have been barely evaluated as an investor, it is unclear whether decisions will be right or not. I am vividly aware of this fact and therefore devote most time to think about how to limit the capital’s exposure to my ignorance. The questions-framework for weighting represents one of such systems.

I will be inclined to frequently sacrifice “obvious” returns by not weighing a position as I believe would be more accordingly. I have been repeatedly proven wrong, on a wide range of topics and matters. Consequently, although I may occasionally arrive at the conclusion that some security is severely mispriced, I will only rarely exceed a certain threshold when weighing. I’m certain to not yet count with enough knowledge nor tested judgment as to weight in accordance with my perception. I further believe myself to be underestimating my personal world of the unknown. In consequence, we will continue transiting a methodical yet perceived-as-higher-security path for the foreseeable future.

Notwithstanding the downside embedded in the procedure adopted, I believe it will help maximize returns since inception decades out. Accepting this set of short-term headwinds will allow us to benefit from an ever-enduring tailwind. It is the only path I see for being a good capital allocator in ten years and sustainably thereafter.

Nvidia

The decision to sell Nvidia has cost above 30 points of performance in 14 months. It is the costliest mistake I have made while managing the portfolio. No matter its phenomenally negative impact, if I were to face a similar situation, I believe I’d make the same decision. In hindsight, fueled by very powerful biases, turns of events seem obvious. But buying and selling need to be done in foresight, with a wide array of potential states of nature in front. Betting on obscurely unlikely events implies risking the capital under management, which is something I eschew doing. It’s fundamental to note that the perceived likelihood of occurrence depends on one’s understanding, which in this case was superficial.

Investing in an asset of which I know nothing resembles gambling, with maybe less probabilities of succeeding, for we are transacting with, on average, sophisticated people. Of Nvidia I know very little, and I have no clue whatsoever as to how it can look down the line. The fact that it was included in the portfolio was a fortunate event, considering the former statement. Holding it would have been a mistake, for the decision would depend entirely on randomness. Fundamentals evolved astonishingly well. In fact, I wasn’t even aware of the possibility of this occurring, for such revenue, net profit growth and expectations evolution, had not been experienced by any company in the past, as far as my understanding goes.

The situation resembles picking a number in the roulette. Analogously, the picked number, of which I withdrew the chips once I noticed how reckless the buying decision had been in the first place, ended up being the winner. Deeply deliberated analysis was never involved in the operation. Although this decision turned out to be very costly, it may well be that in the future we avoid incurring big losses by employing a similar process. It’s not about the companies we don’t invest in, but about the ones we do invest in.

Ultimately, and in line with making only a handful of decisions, missed opportunities do not matter. What’s important is to be right in the decisions made, or at least not to be fatally wrong, and fatality can only come from possessed assets. This is fundamentally tied to avoid betting big on a business whose fundamentals end up unfolding unfavorably. Mistakes will inevitably be made. Future states of nature will cause some decisions to look foolish, as occurred with Nvidia. I believe this price needs to be paid for optimal performance, which involves minimizing risk.

Holding and Understanding

Over the past years, I found that buying a seemingly undervalued security is not as mentally taxing as holding a seemingly overvalued security. This may be the element that costs the most percentage points of performance. Continuously trading a wonderful business such as Walmart, Costco, or Amazon, is the mistake that’s punished the most. Shortcuts are nonexistent and, I would argue, not needed. Buying equity over these companies implies having capital intrinsically appreciating by 15-25% per annum over several decades. Greed encourages one to aim for more; arrogance makes one think they can experience such returns while avoiding volatility; and pride facilitates fooling oneself into thinking they are making the right decisions by being in and out of these companies. All massive mistakes I recurrently make, though I try to limit the extent to which they affect performance.

Holding companies that are expensively priced seems to be a potential requirement for enjoying the continuance of their fundamental growth. Rational conviction in reaching an appealing destination is the fundamental pre-requisite. Selling Nvidia was a decision triggered by how expensive it looked. There are occasions where abrupt declines or spikes are driven by underlying fundamental changes, and others where the market overestimates certain events’ impact.

Not understanding a business causes a persistent misjudgment of the general picture. Expensive companies sometimes are so for a reason. Lacking the information to properly assess the situation is the mistake I made in Nvidia’s case. It must be observed that, even if I counted with deep understanding of Nvidia’s operations, I wouldn’t have arrived at the conclusion that fundamentals would evolve as they did. Notwithstanding this, I am trying to build a body of useful knowledge, capable of drawing valid inferences from a wide array of scenarios.

Sometimes, the market pushes an asset’s price well in excess of its estimated intrinsic value. Selling is not necessarily the best response to this event, for, what if the share price permanently lives ahead of the estimation? Nicholas Sleep argued in the mid-2000s that all businesses, indeed all of them, will be meaningfully mispriced eventually. The problem lies in selling a good business cataloged as overvalued, expecting a big decline, and having the first brutal repricing in a decade. Furthermore, one always needs to consider a potential persistent error in the value estimation.

I cannot overstate the impossibility of recurrently timing these declines and I understand portfolio managers who try them. A sense of risk mitigation and flawed rationality urges one to. In this regard, I am trying to find an equilibrium between avoiding being foolish and reckless. At the cost of performance, I have, since inception, tilted towards potentially being foolish. Recklessness is a deadly trait in this business. Nonetheless, for it is out of holding that most wealth has been created, a balance needs to be found.

Closing Remark

I believe it is vital for myself to express, as distinctly as I can, how the portfolio is being managed. There are numerous unresolved matters on my side, but transparency is a trait I’ve always respected, hence why I expose some of these. Naturally, communicating behavior and reasoning encounters verbal obstacles, which I try to overcome. Patience is fundamental for any substantial result to materialize, and I have several reasons to believe that rationality should tilt the probabilities of desirable future states of nature in our favor.

Contact: giulianomana@0to1stockmarket.com

Happy to read you again! Thoughtful letter as always with great insight into your process! Thanks for sharing it with us!

Thanks for a brilliant read my friend!