Microsoft reported quarterly results on Tuesday after the market closed. In this article, I’ll go over the company’s financials, management’s commentary, and outlook. At the end, I’ll share my take on the quarter and what I’m doing portfolio-wise.

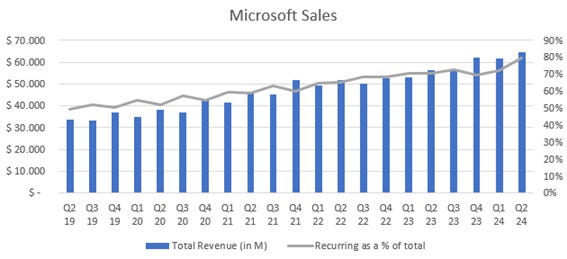

Microsoft reported record sales during the last quarter of their fiscal year, coming in at 64.7 billion dollars and growing 15% yearly. For the full year, Microsoft’s revenue was 245 billion, up 16% YoY. More importantly, during the past quarter, services’ revenue dramatically outpaced that of product revenue. Recurring revenue as a percentage of total increased 8pps QoQ, getting to 80%.

Gross profit increased 14.4% yearly to 45 billion dollars, implying a 69.5% gross profit margin, which slightly declined. The company reported 27.92bn in operating income, with a margin of 43.1%. Net income generated was 22bn during the quarter, with a net profit margin of 34%, declining 170bps YoY.

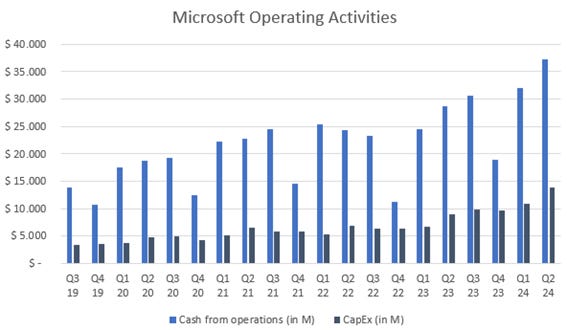

Microsoft brought in a record 37.19 billion dollars in cash from operating activities, representing a 29% yearly increase. On the other hand, capital expenditures amounted to 13.87bn, materially up yearly and sequentially. Hyperscalers are incurring massive CapEx related to infrastructure building. The race for cloud dominance is very real.

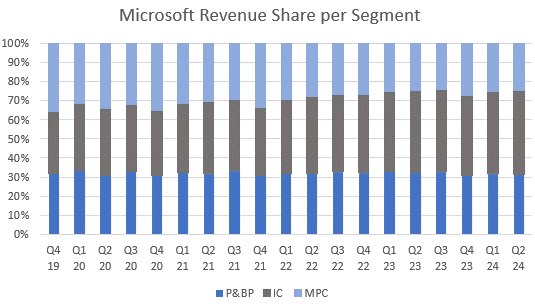

Prior to diving into each segment’s particular performance, a general overview. It’s interesting to note that intelligent cloud keeps gaining share of total sales, while more personal computing’s decreases. During the quarter, Productivity and Business Processes generated 31.4% of total sales, while Intelligent Cloud and MPC, 44% and 24.6% respectively.

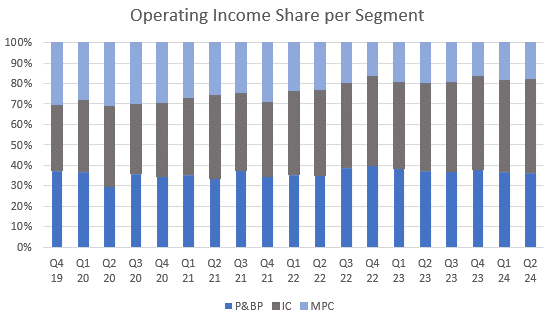

Operating income contribution is relatively similar. However, due to IC and P&BP’s superior margins, their share of total operating income is higher than their share of total sales. Intelligent cloud contributed 46% of total operating income, while Productivity & Business Processes and More Personal Computing, 36% and 18% respectively.

During the quarter, productivity and business processes had sales of 20.31 billion dollars, up 10% yearly. Moreover, it operated at a 50% margin, generating 10.1 billion in operating income. The segment’s operating margin was flat yearly and down 190bps sequentially.

Management’s Commentary on P&BP:

Copilot customers increased 60% quarter-over-quarter.

400+ healthcare organizations have purchased DAX Copilot to date, up over 40% QoQ.

Dynamics 365 now generates 90% of Dynamics’ total sales.

Microsoft Teams saw YoY usage growth, with Teams Premium surpassing 3M seats, up 400% YoY.

LinkedIn members grew and the platform had record engagement.

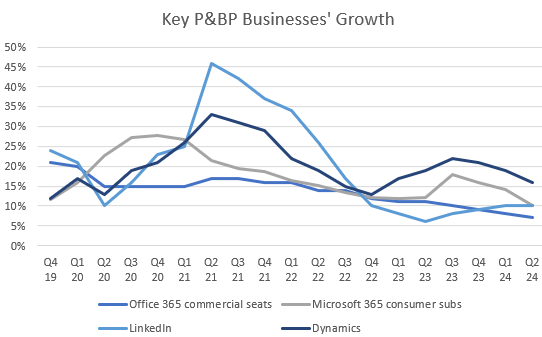

Office 365 commercial seats increased 7% yearly, which continued decelerating; whereas consumer subscriptions grew 10% to 82.5 million. LinkedIn’s growth, on the other hand, kept stable at 10% yearly. Over the past 12 months, LinkedIn reported revenues of 16.3 billion dollars, up 9.2% YoY. Lastly, Dynamics generated sales of 6.5 billion dollars, up 19% YoY. During the quarter, Dynamics and cloud services grew 16% YoY, while Dynamics 365 grew 19%.

Intelligent Cloud reported revenues of 28.5 billion dollars, growing 18.8% yearly. The segment operated at a 45.1% margin, which was up yearly but down sequentially, having operating income of 12.85bn.

Azure’s growth decelerated sequentially to reporting 29% on a yearly basis. It is very interesting to observe that Azure’s AI Services, namely those acquired and offered mostly based on OpenAI, contributed 8 points of the 29. Over the past couple of quarters, AI Services have contributed significantly to Azure’s topline. On the other hand, server products and cloud services’ sales increased 21% yearly.

Management’s commentary on intelligent cloud:

Arc customers surpassed 36,000, up 90% YoY.

Azure AI customers grew 60% YoY, exceeding 60,000. Average spending per customer keeps increasing.

Microsoft Fabric’s customers increased 20% QoQ to 14,000.

GitHub Copilot’s customers grew 180% YoY, surpassing 77,000.

GitHub is at a 2 billion dollars run rate.

Power Platform MAUs increased 40% YoY, crossing 48 million.

Defender for Cloud, Microsoft’s cloud security solution, had over a billion in TTM sales.

Lastly, more personal computing generated revenues of 15.89 billion dollars, growing 14% on a yearly basis. The segment’s operating margin was 31% during the quarter, declining 300 bps YoY and slightly sequentially.

Over the past twelve months, Microsoft’s gaming offerings increased sales by 44% yearly. It is to be observed that Activision contributed 48pps. On the other hand, Windows generated 23.2 billion in revenue, growing 8% YoY, after a double-digit decline in 2023 (FY). Lastly, sales derived from search and news ads increased slightly yearly, to 12.57bn.

Management’s commentary on MPC:

Bing and Edge took share.

Microsoft’s gaming offerings have now over 500 MAUs across platforms.

Management Commentary and Outlook

Satya opened the call by mentioning the momentum that’s immersed in the whole ecosystem. Cloud and software offerings are gaining traction, and most products keep increasing their market share. On the other hand, other businesses like LinkedIn and Nuance are excelling with no signs of them running out of fuel.

The latter two are interesting to remark, for both are showing how AI can enhance almost all of Microsoft’s software offerings. Copilot within Nuance and AI-powered LinkedIn premium are appealing to lots of users and, in the case of Nuance, healthcare organizations.

Azure is Microsoft’s heart. All cloud-based offerings are powered by it and its infrastructure services have escalated immensely over the past 5 years. Nonetheless, AI Services are keeping Azure’s growth from decelerating. During the quarter, the business took share, with demand for AI services being in excess of available capacity. Commercial bookings increased 17% YoY, with numerous 10M+ and 100M+ dollars contracts for Azure. Remaining performance obligations, on the other hand, increased 20% to 269 billion dollars.

To support the underlying demand Azure is experiencing, the company is committed to substantial investments. Almost the completeness of capital expenditures are destined to continue building datacenters and the required infrastructure to support the coming decade(s) demand.

For the next quarter, management expects:

An increase in CapEx.

P&BP revenue to grow 10.5% YoY to 20.45 billion dollars at the midpoint of guidance. Microsoft 365 subscriptions are expected to keep driving Office sales, LinkedIn’s growth is expected to be high single digits, and Dynamics to grow low to mid-teens.

IC Sales are expected to grow 19% YoY to 28.75 billion at the midpoint. Azure’s sales are expected to grow 28.5%.

MPC revenue is expected to grow 10.5% YoY to 15.1 billion at the midpoint.