I know many of you follow this newsletter especially because of my Microsoft’s coverage. That being the case, I decided to leave this earnings review for free. Hope you find it useful. At the same time, I wanted to announce that I’ll be publishing the first part of Burford’s research on Wednesday.

Microsoft reported results on January 30th. The company generated revenue in excess of 62bn dollars during the fourth quarter of 2023, increasing 17% on a yearly basis and exhibiting a 4yr CAGR of 13.8%. It’s worth highlighting that Activision contributed to 4pp of revenue growth. During July, a court filing was leaked, which illustrated management’s self-stated ambition for the next decade. By 2030, they are aiming for sales of 500bn dollars, for which, were they to reach such goal, a reacceleration of revenue was due.

A metric that’s generally overlooked when analyzing Microsoft’s quarterly results is their service and other business. The latter consists of those services whose usage can be sold on a recurring basis. Since Satya Nadella took over in 2014, emphasis has been placed on Microsoft’s recurring-revenue-generating business. As of this last quarter, service and other revenue was 43.07bn, representing 69.4% of total revenue. Its share was up 80bps YoY. The remaining 30% is derived from their products business, mostly sold in one-time payments.

Note: Microsoft’s fiscal year is two quarters ahead of the calendar. However, my charts are computed according to the calendar year.

Moving down the income statement, Microsoft generated 42.39bn in gross profit, implying a margin of 68.3%. The latter expanded 150bps on a yearly basis. Operating income for the quarter was 27.03bn, with a respective margin of 43.5%, up almost 500bps YoY. Lastly, Microsoft reported net income of 21.87bn, compared to 16.42bn last year.

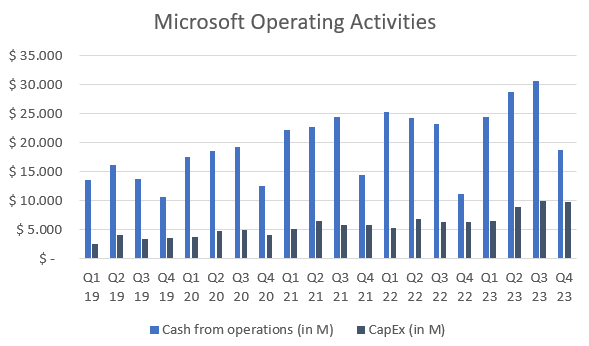

Turning to the cash flow statement, the company brought in 18.85bn in cash from operating activities, an increase of 68% compared to 2022’s fourth quarter. On the other side, capital expenditures amounted to 9.73bn. The latter experienced a dramatic rise during 2023 as management called for an increase driven by investments in cloud and AI infrastructure.

Before going into a detailed analysis of each segment’s performance, a general overview. During the quarter, the Productivity and Business Processes (P&BP) business generated 19.24bn in revenue, growing 13% YoY. Microsoft’s Intelligent Cloud (IC) grew its topline by 20%, exceeding 25.8bn dollars. Lastly, More Personal Computer’s revenue was 16.89bn, up 18.6% YoY.

With what respects to operating income share as a percentage of total, P&BP, IC, and MPC, contributed 38%, 46.1% and 15.9% respectively. Over time, the first two segments have increased their share on a substantial basis, now reaching 84%. This is a byproduct of the higher margins at which they operate and the faster pace of revenue growth.

Breakdown by Segment

Microsoft is a business of businesses. This image always helps me remember what’s encompassed where.

Productivity and Business Processes

Along with Intelligent Cloud, this is one of the two business units I believe matter the most for the company. In here, we have products that still have long runways, can be sold at high margins with room for operating leverage, have a thesis on their own, are mostly subscription-based with strong lock-in effects, and are immersed in this hybrid-and-growing industry of professionals and productivity with a leading position.

Productivity and business processes generated 19.24bn in revenue, growing at a 13.2% rate YoY. Moreover, it operated at a 53.4% margin. The latter expanded 540bps compared to last year and was slightly below last quarters. Operating income was 10.28bn, up from 8.17bn.

Within this segment, the main offerings I pay attention to are Dynamics, with a focus on Dynamics 365, Microsoft Office, with Teams in mind, and LinkedIn. All products had been growing at double-digits for a long time, accelerating during the pandemic, and then digested the demand that was pulled forward.

This past quarter, Office 365 Commercial seats grew 9% on a yearly basis while Microsoft 365 Consumer Subscribers increased 15.8%, reaching 78.4M. The main difference between both is that commercial seats are for enterprises, while subscribers are mostly professional individuals.

On the other hand, Dynamics overall generated 1.57bn during the quarter, growing 21% YoY, and slightly from last quarter. Dynamics 365, the most important component of Dynamics, grew 27% on a yearly basis.

LinkedIn, a business I believe still has a long runway ahead and it’s filled with optionality, grew 9% compared to last year. After decelerating for almost three years, its topline is starting to grow at more rapid rates. During the quarter, LinkedIn generated 4.19bn in revenue.

Management Commentary on P&BP

“More than 230,000 organizations have already used AI capabilities in Power Platform, up over 80% quarter-over-quarter.

Dynamics 365 once again took share.

Research shows as much as a 70% improvement in productivity using generative AI for specific work tasks.

Record usage of Teams.

More than 400M paid Office 365 seats.

LinkedIn’s new AI features also continue to increase business ROI on the platform, and our hiring business took share for the sixth consecutive quarter”.

Intelligent Cloud

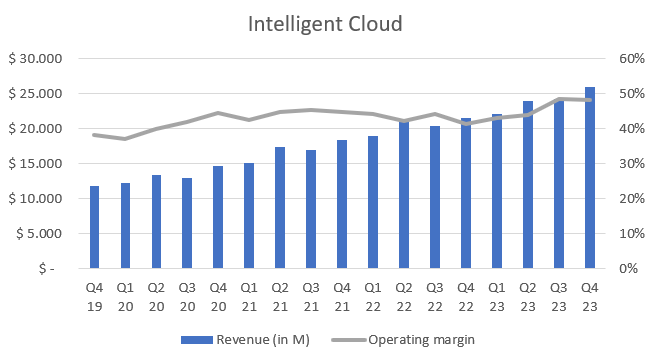

The IC segment generated 25.88bn in revenue, growing 20.3% yearly and 6.6% sequentially. Moreover, the business has grown at a 21% CAGR for the past 4 years. This business’ growth is absolutely remarkable, now being at a 100bn+ run rate. More importantly, Intelligent Cloud had operating income of 12.46bn. The segment’s operating margin expanded 670bps YoY to 48.15%.

Intelligent Cloud constitutes a very large part of Microsoft’s thesis because of the nature of its business units, all of which possess great fundamentals. Additionally, most of them are immersed in industries that are continuously expanding and that generally have a “winner-takes-all” tendency, leading to strong pricing power.

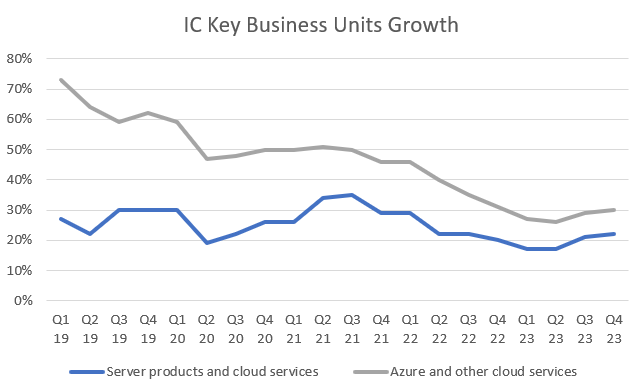

Azure, the most relevant component of Microsoft’s ecosystem, grew 30% yearly. Two quarters ago, management announced Azure had accounted for more than half of their cloud business for the first time. Taking this into consideration, I estimate Azure’s topline to be between 65-75bn. For some perspective, AWS grew 13.2% YoY to 24.2bn.

Management Commentary on IC

“Azure again took share this quarter, with our AI advantage.

We now have 53,000 Azure AI customers. Over one-third are new to Azure over the past 12 months.

Over half of the Fortune 500 use Azure OpenAI today.

Cosmos DB data transactions increased 42% year-over-year.

GitHub revenue accelerated to over 40% year-over-year, driven by Copilot. We now have over 1.3 million paid GitHub Copilot subscribers, up 30% quarter-over-quarter.

Copilot for Security has more than 1 million customers, with 700,000+ of them using 4+ products

The enterprise mobility and security installed base grew 11% to over 268 million seats.”

More Personal Computing

More personal computing had been struggling in the recent past, mostly as a byproduct of the pandemic. After returning to yearly growth in the previous quarter, the trend continued in this one. MPC reported revenues of 16.89bn, representing an increase of 18.6% YoY. Moreover, it generated 4.28bn in operating income, expanding its margin by 200bps yearly to 25.3%.

Microsoft’s gaming segment has been a somewhat secondary element to my eyes, but with Activision, this might change. In October, the company closed the acquisition, for which they paid 75.4bn, mostly consisting of cash. The new business will be reported within More Personal Computing.

Satya is trying to build an ecosystem with high quality IP to which gamers could only access with Game Pass. In addition, the trend towards cloud gaming seems to propose the fundamental change that’s required for turning this industry into a subscription model. In any case, gaming revenue was 7.11bn, up from 4.75bn last year, though Activision’s contribution was 2.1bn.

Management Commentary on MPC

“Usage of cloud-delivered Windows increased over 50% year-over-year.

Gaming MAUs across devices are over 200M

Hours streamed increased 44% year-over-year.”

Management Commentary and Outlook

Pronounced tone of optimism. Satya opened by stating this was a record quarter, exceeding expectations, and how crucial of a role Microsoft Cloud is playing. The latter surpassed 33bn in quarterly revenue, increasing 24% on a yearly basis. Commercial RPOs ended at 222bn, growing 17%, and suggesting a persistent growth in the mid to high teens for the near future.

The conference call was mostly structured around how Microsoft is leveraging all of its AI software and infrastructure. Management has stated in the previous quarters AI was going to abruptly change the company’s operations. In this one, they spoke about its deployment at scale. LinkedIn, Power Platforms, Microsoft Office, Dynamics, GitHub, and almost all of Microsoft’s offerings are benefiting from the company’s efforts on the AI front. Moreover, it’s being claimed that customers’ productivity is increasing extraordinarily when utilizing these new features and technologies.

Microsoft is winning new customers by infusing AI across the whole ecosystem. At the same time, Azure AI services are highly influencing Azure’s results. Accordingly, Azure grew 30% on a yearly basis, but 6 points of this growth came from Azure’s AI services. Artificial intelligence is therefore propelling the completeness of Microsoft’s business forward. In fact, AI Service drove high demand for Azure’s large, long-term contracts.

It is important to highlight that capital expenditures came lower than expected “due to delivery for a third-party capacity contract shifting from Q2 to Q3”. These investments in data centers are in response to what management foresees demand to be in the near future. Finally, as a consequence of this contract shifting, management expects capital expenditures to “increase materially on a sequential basis driven by investments in our cloud and AI infrastructure”.

For the full fiscal year 2024, Amy mentioned that the operating margin is expected to increase by 1-2pp. Turning to segment guidance for the next quarter, management called for the following:

In Productivity and Business Processes, revenue is expected between 19.3-19.6bn, an 11% growth at the midpoint. LinkedIn’s growth is expected at mid to high single digits; Dynamics is expected to grow at mid-teens, driven by Dynamics 365; and Office 365 to grow revenue at 15%.

Intelligent Cloud’s revenue is expected to be between 26-26.3bn, representing 18.5% growth at the midpoint. Azure’s revenue growth is expected to be similar to this quarter, driven by a strong contribution from AI.

For More Personal Computing, Microsoft expects revenue of 14.7-15.1bn, implying growth of 12.5% at the midpoint. Search and news ads revenue, ex-TAC, is expected at mid to high single digits. Finally, gaming revenue is expected to grow in the low 40s, with an impact of 45 points from Activision.

My Take

I tend to be extremely skeptical of new technologies and new trends. Reading history brings perspective on this sort of matter. Moreover, when a new technology emerges, Clayton Christensen has shown the impossibility of assessing its future prospects. In the same line, even if the addressable market ends up being extremely large for AI, it is not obvious that such results would be translated to investors’ pockets, as happened with the PC market.

Having said this, Microsoft seems to have been holistically empowered. The offerings the business has possess a truly long runway. Given most of them are aimed at the industry of hybrid work, software, and cloud infrastructure, I was invariably expecting double-digit growth for the coming years. However, AI integrations across the board have propelled the business forward, which is now growing in the high teens.

Satya’s performance since taking over in 2014 has been remarkable. He shifted the completeness of Microsoft’s business towards a subscription-based model, launched highly lucrative and potential initiatives like Dynamics and Teams, made key strategic acquisitions such as GitHub and LinkedIn, and placed Azure in a fantastic spot, taking share in the cloud computing industry. Nadella has now made a major investment in OpenAI, which helped launch Azure AI Services, fueling Azure’s demand, and leading to AI implementations at scale across Microsoft’s ecosystem.

Microsoft has been on a wonderful track and never lost it. And, apparently, the climb now seems to be steeper. But even without this “positive shock”, Microsoft is a conglomerate of spectacular businesses. Within software, cloud and hybrid work, the company possesses strong and consolidated players in markets that are expected to continuously grow in the coming time. To my eyes, most of Microsoft’s quarters have been exceptional in the recent past, with this one being in the same line.

Personal Commentary

I hope you found the earnings review useful. Next companies to cover are Google, Texas Instruments, Visa, Zoetis, Mercado Libre, and perhaps Burford and Winmark. Reminder that I’ll be publishing the first part of Burford’s research on Wednesday.

Contact: giulianomana@0to1stockmarket.com

Crazy to think that Microsoft is so intrench in our daily lives that it can be consider nearly as a commodity. You can be sure that your Teams, Cloud services or Outlook will open and be reliable as gas you put in your car or electricity for the lights. A blue chip growing 13% per year top line is unbelievable. What a wonderful company it is! Thanks for your review,as always. Cheers!!