Microsoft reported results on October 24th. The company generated 56.5bn in revenue, growing 12.7% on a yearly basis and exhibiting a 4yr CAGR of 14.3%. Microsoft was expected to return to more rapid growth eventually, in line with their 2030 500bn ambition.

However, what most eyes miss here, but I pay special attention to, is the revenue composition. Microsoft derives revenue from, on the one side, what they label as products, which mainly consists of one-time payments, like hardware sales. Services is their second revenue source, which include mostly software/cloud-based offerings and, due to their recurrent-usage nature, imply a subscription model.

Note: Microsoft’s fiscal year is two quarters ahead of the calendar year. I will use calendar for there not to be any confusions.

Subscription-based offerings tend to be much more resilient, making up for a fundamentally stronger business. Since Satya Nadella became CEO, emphasis has been placed on turning Microsoft into a subscription-based business, or as close to that as possible. Consequently, recurring revenue as a percentage of total sales have been continuously trending upwards, now standing at 73%, increasing 300bps QoQ.

Moving down the income statement, Microsoft generated 40.2bn in gross profit, increasing 16% on a yearly basis. The latter implies a margin expansion from 69% last year to 71% in this one. Operating income was 26.89bn for the quarter, with the operating margin expanding by 470bps to 47.6%. Lastly, Microsoft produced 22.29bn in net income, meaning it operated at a 39.4% margin, up 440bps over the comparable Q.

During this last quarter, Microsoft brought in a record 30.58bn in cash from operating activities, increasing 31% YoY. Capital expenditures, at the same time, were also a record 9.9bn dollars. Microsoft has been heavily emphasizing the importance of rapidly developing an extensive and high quality cloud infrastructure, which has translated into a physical competitive advantage over other cloud providers. Free cash flow for the quarter was 20.66bn, up from 16.9bn last year.

Before going into a detailed analysis on each segment’s performance, a general overview. During the quarter, the Productivity and Business Processes segment generated 18.59bn in revenue, growing 13% yearly. Intelligent Cloud’s revenue was 24.25bn, increasing 19% year-over-year. Finally, More Personal Computing finally returned to yearly growth at 2.5%, generating 13.6bn.

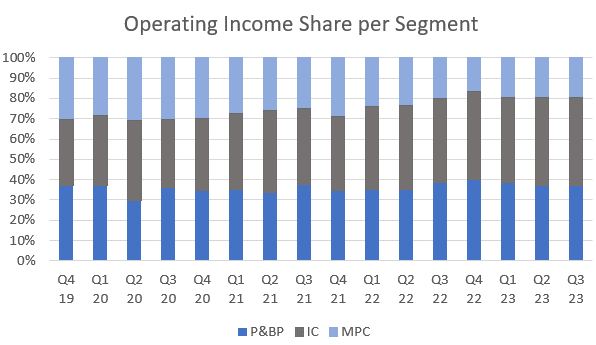

More importantly, the margins at which segments operate are vital to determine how much are they individually contributing to Microsoft’s bottom line. With what respects to operating income share as a percentage of the total, P&BP, IC, and MPC, contributed 37.1%, 43.7% and 19.2% respectively. I’d say it’s objectively good to see this is the case, as with revenue share. P&BC and IC are fundamentally superior businesses than MPC.

Breakdown by Segment

Microsoft is a business of businesses. This image always helps me remember what’s encompassed where.

Productivity and Business Processes

Along with Intelligent Cloud, this is one of the two business units I believe matter the most for the company. In here, we have products that still have a long runway, can be sold at high margins with room for operating leverage, have a thesis on their own, are mostly subscription-based with strong lock-in effects, and are immersed in this hybrid industry of professionals and productivity with a leading position.

Productivity and Business Processes generated 18.59bn in revenue, growing 13% on a yearly basis and 1.6% sequentially. Moreover, it operated at a record 53.6% margin, which was up 300bps YoY and up 410bps QoQ. The latter means the business unit did 9.97bn in operating income, up from 8.3bn last year.

Within this segment, the main offerings I pay attention to are Dynamics (Dynamics 365 is key), Microsoft Office (Teams is key) and LinkedIn. All products had been growing at double digits for a long time and growth accelerated during 2020/21. LinkedIn even got to grow at 40%+ rates.

This past quarter, office 365 Commercial seats grew 10% while Microsoft 365 Consumer Subscribers grew 17.8% to 76.7M now. The main difference is that commercial seats are for enterprises and consumer subscribers are professional individuals, mostly. Commercial seats growth rate seems to be somewhat stabilizing in the low double digits, while subscribers’ growth dramatically accelerated.

Dynamics grew 22% YoY, further accelerating from Q1’s 17% and Q2’s 19%. Dynamics 365, perhaps the most important component of Dynamics, was a major contributor to this, growing at a 28% rate during the quarter, also accelerating from the previous Q’s 26%. Microsoft started disclosing Dynamics revenue when they ended their last fiscal year, in July. This past quarter, Dynamics generated 1.54bn in revenue, up from 1.26bn last year.

Lastly, LinkedIn grew 8% on a yearly basis. This is the first quarter were growth rates for LinkedIn accelerate QoQ since the second quarter of 2021. The business unit generated 3.91bn in revenue, up from 3.62bn last year. My impression of the declining growth rate had been more of a digestion that needed to happen. LinkedIn experienced unusually high demand during 2020/21, part of which was most likely pulled forward. This, added to the weak job environment, have impacted LinkedIn results. But re-acceleration is good to see and, given its size, an above 8% rate is a very healthy growth.

Management commentary:

Dynamics 365 took share for the 10th consecutive quarter

We’re becoming the Copilot-led business process transformation layer on top of existing CRM systems like Salesforce

Teams MAUs grew to 320M (up from 300M two quarters ago).

There are more than 2,000 apps in Teams store and some of them exceeded 1M MAUs on Teams

LinkedIn surpassed 985M members. There are more than 450M newsletter subscriptions globally, up 3x. Premium sign-ups were up 55% YoY. The hiring business took share for the 5th consecutive Q

Intelligent Cloud

The IC segment generated 24.25bn in revenue, showing high and persistent growth. On a yearly basis, IC grew 19%, reaccelerating from the previous Q’s 15%. Being now at an almost 100bn run rate really shows management’s brilliance at operating this business unit. More importantly, this was accompanied once again by operating leverage. Intelligent Cloud did 11.75bn in operating income, implying a 48.4% margin. The latter expanded 430bps YoY.

Intelligent Cloud constitutes a very large part of Microsoft’s thesis because of the nature of this business, with fantastic fundamentals. Like in the previous segment, there are many businesses embedded here, with most of them having shown very rapid growth, profitability at scale, and with still long runways ahead. Among some of the secular trends Microsoft has leaders in are cloud computing, cloud security and open-source development. With Open AI’s deal, Microsoft set strong foot in this mysteriously and apparently immense market.

Note: Caution is advised with what respects to AI’s TAM forecasts.

Azure, probably the most relevant component of Microsoft’s ecosystem, grew by 29%, re-accelerating from last Q’s 26%. Keep in mind the company does not report Azure on an isolated basis, but it includes it with other cloud services. Nevertheless, management announced in the previous Q that Azure accounted for more than half of their cloud business (110bn then), meaning Azure was at a 55-65bn run rate. Acknowledging this highlights how remarkable this business’ momentum is. For some perspective, AWS grew at 12%, though at a 90bn run rate.

Management commentary:

Azure again took share as organizations bring their workloads to our cloud

We have the most comprehensive cloud footprint, with more than 60 datacenter regions worldwide…also have our AI services deployed in more regions than any other cloud provider.

More than 18,000 organizations now use Azure OpenAI Service

Azure Arc customers increased 140% YoY to 21,000

We are the only other cloud provider to run Oracle’s database services

More than 16,000 customers are using Fabric (launched in May of 2023)

GitHub Copilot has over 1M paid users and more than 37,000 organizations have subscribed to Copilot for Business, up 40% QoQ.

More than 126,000 organizations have used Copilot in Power Platform to date

We see high demand for Security Copilot, the industry’s first and most advanced generative AI product

Our SIEM Microsoft Sentinel now has more than 25,000 customers and revenue surpassed a $1 billion annual run rate (launched in 2019).

The enterprise mobility and security installed base grew 11% to over 259 million seat

More Personal Computing

The last segment that Microsoft reports results in is called More Personal Computing, one which has been posing trouble for the past couple of years. The pandemic got this business to grow extremely fast and the profit formula goes mostly around one-time payments, which makes revenue dependent on quarterly sales. At the same time, secular tailwinds backing this business up are not as pronounced as with IC or P&BP, making this extra demand a complete pull forward. Partly due to these reasons, MPC has struggled with growth and profitability.

However, after four quarters of declining revenue (YoY), this past quarter the segment returned to yearly growth. The business unit reported 13.6bn in revenue, up 2.5%. Moreover, it generated 5.17bn in operating income, up from last year’s 4.21bn. It appears as if the business is finally stabilizing and getting back to its prior levels of profitability.

In this segment, there has not been any product of extreme appeal to keep an eye one, or at least from what I think makes up for Microsoft’s thesis. Nevertheless, it is in here where they have Bing’s revenue and their gaming segment. The first of them has suddenly (this year) become, to the eyes of the market, a potential growth driver moving forward due to AI integrations. I’m skeptical of such view.

The gaming segment has been a somewhat secondary element to my eyes, but this might have changed this last quarter. Satya is trying to turn this business into a much stronger one, fundamentally, making it a subscription-based offering. What I have been seeing here, which was further ratified by the Activision deal, is that management is trying to build an exclusive ecosystem of IP. They did this by acquiring more than a dozen game developer studios over the past decade and very valuable IP, like Minecraft.

This IP would be distributed to gamers through cloud gaming, something Azure powers and that allows for a much better UX, decreasing latency and removing the need for downloading games. What would grant access to this ecosystem is the Game Pass, a monthly subscription. Finally triggered by Activision’s size, it might be time to start paying attention to this segment. Gaming generated revenue of 3.9bn, up 8% YoY.

Management commentary:

We rolled out our biggest update to Windows 11 ever, adding 150 new features, including new AI-powered experiences

We introduced Copilot in Windows

Microsoft Edge has now gained share for ten consecutive quarters

Record hours played per subscriber this quarter

Management Commentary and Outlook

Satya opened his remarks around Microsoft Cloud business’ momentum. This past quarter, it surpassed 31.8bn in quarterly revenue, implying a well over 120bn annual run rate, and growing at 24% YoY. Almost all of Microsoft’s businesses are taking share and growing comfortably double-digits.

What appears to have caused another uptick for the cloud segment is Copilot. Ever since the team developed GitHub Copilot (which I believe was a first of its kind) in 2021/22, emphasis has been placed on transferring this capabilities, in one way or another, to other business units. Copilot is some sort of AI assistant that Microsoft started making available in Microsoft 365, Power Platform, Dynamics, LinkedIn, Teams, etc. Based on what management claims, customers are excited with these releases and Copilot, across platforms, is driving immense demand.

Moreover, given Copilot and OpenAI services require high degrees of computing power and run on Azure, the latter experienced higher than expected growth. Azure is at a 60-65bn run rate and still growing at high 20% rates. Management guided for 26-27% Azure growth in the next quarter and for growth to remain “roughly stable” throughout H2 (Q1 and Q2 of 2024).

It is clear that, to remain in this trajectory, investments are needed. Microsoft incurred 9.9bn of capital expenditures this quarter and plans to step this up. Investments in cloud have provided a physical competitive advantage to Azure over other cloud providers:

“We have the most comprehensive cloud footprint, with more than 60 datacenter regions worldwide, as well as the best AI infrastructure for both training and inference. And we also have our AI services deployed in more regions than any other cloud provider.”

For their outlook on the next Q, management mentions:

P&BP revenue is expected to grow 11-12% to 18.8-19.1bn. Office 365 is expected to grow at 16%, driving the segment, LinkedIn at mid-single digits and Dynamics in the high teens.

IC revenue in the next Q is expected at 25.1-25.4bn, growing 17-18%. Azure’s growth for the next Q is expected to be 26-27%.

MPC revenue of 16.5-16.9bn, which includes Activision’s impact. Gaming Is expected to grow in the mid to high 40s, with 35 points of impact from Activision.

Capital expenditures are expected to increase driven by investments in cloud and AI infrastructure.

My Take

The impressive thing about Microsoft’s quarterly reports is that they deeply show how long of a runway the company still has. Several billion and tens of billion business units still carry strong momentum and, for where information points to, continuation is expected.

Management’s publicly-made ambition of 500bn in revenue by 2030 seem plausible. Whether you look at Dynamics, Azure, Microsoft 365, Teams, Power Platform, GitHub, cloud security offerings, or wherever you look at, businesses continue taking market share while comfortably increasing margins. LinkedIn has been under some pressure and management mentioned negative bookings growth again on Talent Solutions, but, until the tough hiring environment goes by, it is difficult for this to mean LinkedIn is in actual trouble. I highly doubt the latter is true.

What’s also remarkable here is the fact that operating leverage keeps kicking in at Microsoft, also making their margin expansion ambition more plausible. This is, in my opinion, a positive and reminded consequence of what has been happening in Microsoft’s overall business.

As I mentioned in the past couple of quarters, the focus is on Intelligent Cloud and Productivity and Business Processes. These two have intrinsically superior fundamentals than MPC and, as long as they keep gathering share, margin expansion should be a possibility. P&BP’s 53% (!) operating margin, expanding 400bps YoY, gives a clear show of this.

Finally, Azure, which I reiterate, is the most important element of Microsoft’s thesis, keeps taking share, and its physical competitive advantage is showing. This, added to Azure OpenAI Services and Copilot will, according to management, continue to drive high growth rates for the coming quarters.

In conclusion, another bright quarter from a fantastic business.

Personal commentary

I hope you enjoyed the review or at least found it partly useful. If interested in Texas Instruments, Google, Visa, Zoetis or Mercado Libre, I’ll be covering them in the coming weeks. I’m quite short of time so they will take some time.

Contact: giulianomana@0to1stockmarket.com

Disclosure: This is not financial advice

Thank you my friend!