I was going to write a thread covering Microsoft’s earnings, but there’s just too many things I’d like to mention and, at the moment of this writing, transcripts aren’t even out. So, I suppose an article would suite the task better. I’ll split this article in two parts, an overall analysis and a segment breakdown.

Overall Analysis

Microsoft’s revenue grew 2% YoY making the company earn 52.7bn dollars for the second quarter of their 2023 fiscal year (they use a different fiscal year than most companies). In constant currency, revenue grew 7%, which means that FX headwinds were over 500bps.

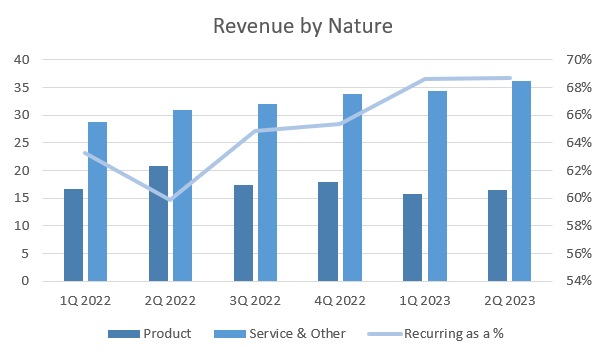

The first and very relevant point I wanted to address is the composition of revenue and how that trend has gone for the past years. The following chart shows how much revenue is Microsoft earning from Product, Services & other, and the line is what percentage does the latter represents of total revenue.

As seen, Product revenue has suffered quite a fall since 2Q 2022, but services & other seem to continue thriving. It is worth highlighting that the latter mainly consists of cloud services with most of them charging clients in a recurring basis. The line showcases that Microsoft’s software offerings as a % of the whole is trending abruptly up, increasing 800bps YoY and standing for the second quarter in a row at 68%. The reason for me mentioning this is that recurring revenue is known to be far more resilient than product revenue.

Gross profit for the company was 35.25bn, up from 34.76bn. Gross profit margin was at 66.5% for the quarter, down slightly YoY. More importantly, if we focus again on the composition of revenue, services gross profit margin increased 220bps YoY to 67.5%. On the other hand, product’s GPM declined 430bps YoY, causing this overall drop in the margin.

Operating income for the quarter was 20.39bn, down from 22.24bn on the comparable. Operating margin standed at 38.6% and declined 440bps YoY. In the image above, it is observable how relatively rapid the company increased operating costs while not increasing revenue in the same share. Particularly, R&D expenses grew 19% YoY, very much in line with the previous years’ reports, but completely detached from the business performance. Past R&D has proven extremely rewarding for the company, but past returns do not guarantee future ones, so we shall see if this capital was well employed. Lastly, G&A also increased dramatically, almost 70% YoY. This could be an actual concern when evaluating Microsoft’s cost efficiency. However, last week Satya already acknowledged this when the company announced 10k layoffs.

The last section of the income statement consists on the image shown above. I believe there’s nothing worth mentioning so we’ll get right to the bottom line. Net income declined year over year, from 18.7bn to 16.42bn with its margin falling 510bps to 31.1%. Again, small changes here, the damage was done at an operating level.

The last thing I’ll mention in this section is Free Cash Flow. In this quarter, Microsoft produced 4.9bn in FCF, making the margin fall to a new recent low of 9.4%. Capital Expenditure went up 6.8% YoY so, kind of in line with the business, not a drastic increase.

“Cash flow from operations was $11.2 billion, down 23 percent year-over-year as strong cloud billings and collections were more than offset by a tax payment related to the TCJA capitalization of R&D provision as well as higher employee and supplier payments. Free cash flow was $4.9 billion, down 43 percent year-over-year. Excluding the impact of this tax payment, cash flow from operations declined 7 percent and free cash flow declined 16 percent.”

Adjusting for this change, adj FCF would have been 7.3bn, down from 8.7 last year.

Segments

The Productivity and Business Processes business unit generated 17bn in revenue, growing 7% YoY and 8.17bn in operating income, exhibiting an unchanged margin of 48%.

Intelligent Cloud made 21.5bn in revenue in the current quarter, growing 17% YoY and produced 8.9bn in operating income, which’s margin declined 400bps YoY to 41.3%.

More Personal Computing’s revenue declined 19% YoY to 14.2bn and its operating income was 3.32bn; this margin dropped around 1200bps.

MPC mainly consists on selling hardware and Windows related licenses. This business unit has been losing share on the completeness of the company, meaning Microsoft is turning more and more to be a Software and Cloud company (shown in the Revenue by Nature chart), which is not that bad after all. If we look at the margins and resiliency each segment has, I believe it should be logical to opt for P&BP and IC over MPC. In conclusion, MPC is hurting the business, but the other segments (which in my opinion make 90% of Microsoft’s thesis) are still performing and at 40%+ margins.

The following contains the most relevant information from the earnings call, in which Microsoft gives a ton of information. They give it in kind of a chaotic way, I’ll try to group it per segment, but some mistakes may be made.

Productivity and Business Processes

Power Automate has more than 45k customers, up 50% YoY.

Dynamics 365 now represents over 80% of Dynamics revenue and a new Supply Chain Platform was introduced.

Microsoft 365 is rapidly evolving into an AI-first platform. There are 63M consumer subscribers, up 12% YoY.

Microsoft Teams surpassed 280 MAUs (+3/4% YoY). The number of third party apps with more than 10k users increased 40% YoY. There are more than 500k active Teams Rooms devices, up 70%.

“Viva Sales is the “Super App” in Microsoft 365 for sellers. We’ve seen strong interest since making it generally available this Q.”

80% of enterprise customers use five or more Microsoft 365 applications.

LinkedIn’s revenue grew 10% and its user base surpassed 900M. Newsletter creation was up 10X YoY. More than 45% of hirers on LinkedIn are explicitly using skills data to fill their roles.

Paid Office 365 commercial seats grew 12 percent year-over-year.

In our per-user business, the enterprise mobility and security installed base grew 16 percent to over 241 million seats.

Intelligent Cloud

“Enterprises have moved millions of cores to Azure, and run twice as many cores on our cloud today than they did two years ago.”

Arc customers doubled YoY to 12k

“We have the most powerful AI supercomputing infrastructure in the cloud.”

“Last week, we made Azure OpenAI service broadly available and already over 200 customers are using it.”

Announced the completion of the agreement with OpenAI

Azure ML revenue has increased 100% for 5 quarters in a row

GitHub is now used by 100M developers (up from 90M last Q)

More than 1M people have used GitHub Copilot to date

“With Nuance DAX ambient intelligence solution, physicians can reduce documentation time by half, improving the quality of their patient interactions.”

“Over the past 12 months, our security business surpassed $20 billion in revenue, as we help customers protect their digital estate across clouds and endpoint platforms. The security business continues taking share and it’s trained on over 65tn signals each day. The number of organizations with four or more workloads increased over 40 percent year-over-year.” This last one is phenomenal news.

More Personal Computing

The number of PCs shipped declined during the quarter, but time spent per PC was up nearly 10%

Monthly active devices reached an ATH this quarter

Cloud delivered Windows is gaining traction, with usage of Windows 365 and Azure VD up over 66% YoY

Windows 11 adoption continues to grow because of its security and productivity value proposition

Microsoft Edge gained share for the 7th consecutive quarter. DAUs of the Start personalized content feed was up 30% YoY

New highs for Game Pass Subscriptions and game streaming hours. MAUs surpassed 120M during the quarter

Back to overall analysis

Most results came in line with management’s expectations, except for some particular cases like advertising. There were also results ahead of expectations, as was the case of Microsoft Cloud, which’s revenue was 27.1bn and up 22% YoY. Commercial RPOs stand at 189bn with 45% of them recognizable in the next 12 months and the other part on the subsequent 12 months. This shall give an approximation of what the future year could look like.

They mentioned several times that they witnessed a weaker than expected December, on all regards, mainly in the US. This has made Microsoft guide for the following:

Productivity and Business Processes revenue between 16.9-17.2bn, growing 11/13% in cc. The growth driver is expected to be Office 365; LinkedIn is expected to grow mid-single digits; Dynamics growth is expected low to mid-teens driven by Dynamics 365

For Intelligent Cloud they expect revenue of 21.7-22bn or 17/19% growth in cc. Azure’s growth in cc is expected to be 33/34% in cc (that would be like 30-31%).

For More Personal Computing, revenue is expected between 11.9-12.3bn, down 14/18% YoY. Devices and Windows OEM should continue declining rapidly until pre-pandemic trend is reached

COGS are expected to grow 1-2% in cc and operating expenses 11-12%.

My Take

After reading everything, I find Microsoft earnings results to be reasonably satisfactory. The business model trend continues to be clear onto what I consider to be the thesis for the next decade (IC and P&BP). There were some concerning elements like the rapid deceleration of LinkedIn’s growth, mainly affected by the advertising sector’s weakness, though engagement continued to tick upwards with the platform having over 900M people and hirers demanding more skills.

The macro context has been weakening for the past months and it got to affect Microsoft’s topline growth and bottom line’s, the latter suffering more. Xandr and Nuance acquisitions are still being integrated so they are hurting the operating costs the company has, I’d expect normalization for later this year.

Both regards made management guide for 11-12% increase in operating expenses for next Q. This is not particularly concerning since they have addressed the issue and committed to continue working to achieve further efficiency. At the same time, Microsoft’s business units have an operating margin of 40%, 43% and 16%. Even MPC’s operating margin could be considered high in its industry, so there’s room to temporarily give a little in such a downturn cycle.

Personal Commentary

I really enjoy writing these kinds of articles and would love to know if you enjoy this or find it useful (or not). If you do, I’ll try to consciously dedicate more time to writing earning reviews. Anyway, hope you enjoy and will read you below if any feedback arises. Feel free to subscribe below!

Disclaimer: Not financial advice.

Nice analysis 👍

Good stuff my man!