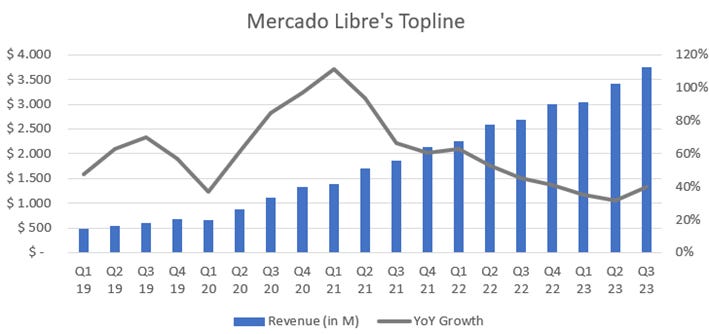

Mercado Libre reported results on November the first, after the market closed. Revenue came in at 3.76bn, growing 40% on a yearly basis, and re-accelerating from the previous quarter’s 31%. Sequential growth was 10%. On an objective note, it is nothing but remarkable how Mercado Libre’s topline has grown over the past 4 years, exhibiting a 58% CAGR.

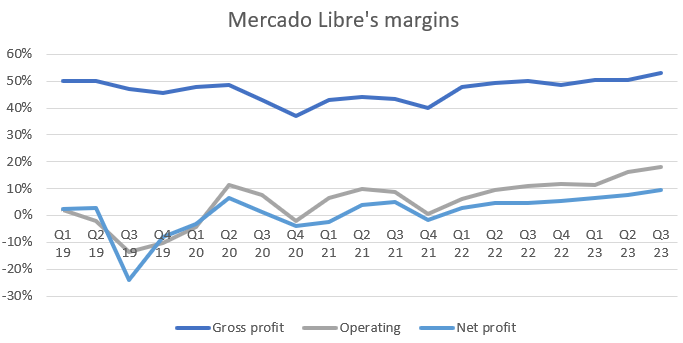

Moving down the income statement, Meli had gross profit of 1.99bn during the third quarter of 2023. Its respective margin stood at 53.1%, up from 50.1% in the comparable. Operating income was 685M, implying an operating margin of 18.2%, which expanded 620bps YoY. Finally, the company generated 359M in net income. The net profit margin expanded 470bps on a yearly basis, being 4.8% last year.

Turning into the cash flow statement, cash from operations was 941M over the quarter, growing 30% on a yearly basis. Cash from operations has dramatically risen over the past quarters, which makes a subsequent normalization somewhat expected. On the other hand, capital expenditures during the 3Q were 126M. Trailing twelve months operating cash flow stands at 4.75bn, while CapEx, at 441M.

Even though this gives the appearance of Meli being a capital-light business, there’s a significant portion of the company’s logistics costs that flow through COGS.

Prior to diving into each segment’s performance, one piece of data. Mercado Libre’s active users surpassed 100M on Q2, reaching 108M. During the third quarter, unique MELI active users increased more than 10% sequentially, getting to 119.8M.

Now, onto both of Mercado Libre’s businesses.