Mercado Libre reported quarterly results last Wednesday. After this review, the only company left to cover is Zoetis. As with companies that have many business units, we will first analyze Meli from an overall standpoint and then dive into details.

The company generated 3.4bn in revenue, growing 31% year over year and 12% sequentially. Mercado Libre experienced extremely rapid growth during and after the pandemic ended. The pattern of digestion is something we’ve seen in many companies covered in these past weeks. However, Meli distances a bit from the crowd as growth, even though it has been decelerating, still remains at high rates.

During the second quarter of 2023, Mercado Libre had 1.72bn in gross profit, with its margin being at 50.4%, up 100bps YoY and flat sequentially. Operating income was 558M dollars, implying an operating margin of 16.3%. The latter expanded 670bps on a yearly basis and 510bps QoQ. Finally, net income was 262M for the quarter with the net profit margin expanding 300bps YoY to 7.7%.

Moving into the cash flow statements, cash from operations was 1.41bn, which was dramatically up on a yearly and sequential basis, though still down from last year’s quarter. There is some seasonality embedded in the business, so the latter shouldn’t be a surprise. Trailing twelve months operating cash flow stands at 4.53bn. On the other hand, capital expenditures were 114M. Both variables leave free cash flow at 1.29bn, or a 37% margin.

Even though this gives the appearance of Meli being a capital-light business, there’s a significant portion of the company’s logistics costs that flow through COGS.

Before going into each particular segment’s performance, one piece of data. Mercado Libre’s ecosystem surpassed the 100M unique active users in the first quarter and, in this one, reported having over 108M.

Mercadolibre, the marketplace

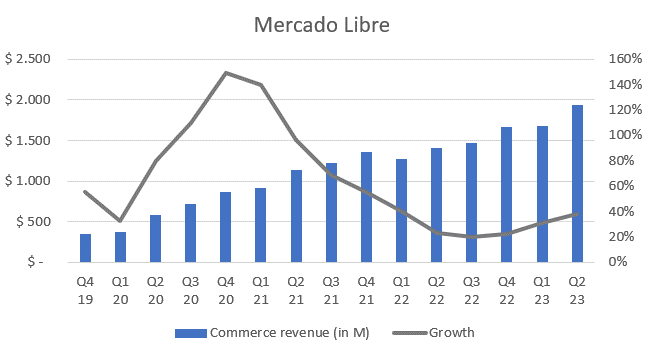

Meli’s e-commerce revenues rapidly increased with the pandemic’s boost and then decelerated to more normal growth rates. On this last quarter, they were 1.93bn, growing 38% YoY and 15.5% sequentially. Commerce topline has been accelerating for the past quarters. In Q4 of 2022, revenue grew at 22%, then at 31% during the first quarter and 38% on this one. Objectively remarkable.

Gross merchandise volume was a record 10.5bn for the quarter. GMV increased 23% YoY and 11% sequentially. Growth rates have been hovering in the 20-25% range for 8 quarters now. The reason why revenue grew much faster than GMV is that the take rate was raised, from 16.4% last year and 17.8% during the first Q to 18.4% in this one.

Lastly, items sold via the platform give some general sense of how are supply and demand trending, for which I consider it to be a relevant metric to analyze. During the second quarter of 2023, a record of 325M items were sold through the marketplace. This meant an 18% yearly increase and 5% on a sequential basis.

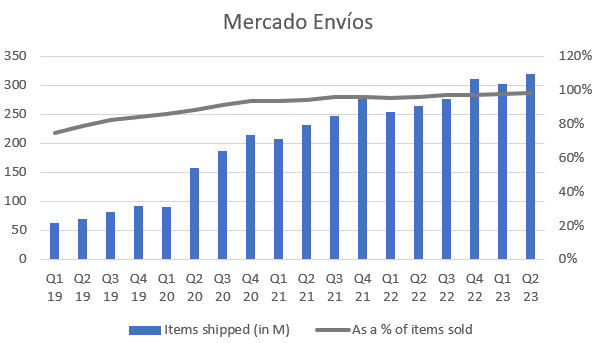

Moving forward, Mercado Envíos has been having a stellar performance for the past years. In this quarter, 319M items were shipped via the company’s logistics arm, growing 21% YoY and equal to 98% of total items sold. Furthermore, 111M items were shipped during the same or next day of the purchase. ‘Same-day or next-day shipments reached 56% of deliveries’. In the same line, ‘almost 80% of shipments were delivered within 48hs across Latin America.’

Fintech

Within Mercado Libre’s Fintech offerings, the company has Mercado Pago and Mercado Credito. The following revenue chart will be showing both businesses together since Meli only started reporting their credit revenues in mid 2022. Anyhow, fintech revenues were 1.48bn for the quarter, growing 24% YoY. Curiously, even though it highly decelerated, it still grew 8% sequentially.

Meli’s digital payment ecosystem has been in a persistent uptrend for several years, now reaching 45.3M users, up 18% YoY and 3% QoQ. Moreover, total payment volume has been remarkably growing as well, showing truly uncapped demand. This past quarter, TPV was 42.1bn dollars, up 39% YoY and 13% sequentially. Quarterly TPV has multiplied by a factor of 8 during the past 4 years.

What I always highlight in this business unit is how rapidly off-marketplace TPV is increasing. That is the key of the business because if it were to only grow at par of GMV, demand would be continuously capped to what’s transacted within the platform, 10.5bn in this quarter for example. Management’s emphasis on expanding Mercado Pago’s addressable market beyond the marketplace is proving wise. Total payment volume off-marketplace as a % of total TPV now stands at 74%.

Moving on, Mercado Credito had been gaining share of overall fintech revenue for a while, getting to 44% in the second and third quarter of 2022 (when data begins). In response to macro uncertainty and other internal factors, Meli decelerated the pace at which it offers credit to merchants and consumers. This past quarter, Credito generated 596M in revenue, up 12% YoY, but also 11% sequentially.

Total credit portfolio was 3.25bn, up 21% YoY and 6.5% sequentially. I’m no expert in credit risk, for which I cannot faithfully dive into the details. I’ll therefore leave you the data below.

Management commentary and outlook

Management started by talking about the momentum Mercado Libre has had for the past years. This is something they always mention in conference calls, but, in the most recent ones, it is accompanied by another color. Rapid growth is now followed by margin expansion with Meli showing very high levels of operating leverage. The team mentioned this results are a testament of both things, the opportunity out there and the cash the company could be able to generate if it were to focus on that.

It called my attention how Meli’s team emphasized the truly enormous opportunity that’s ahead. Even though this is a somewhat recurrent theme, they referred to growth vectors and avenues for investment several times. Management believes it is important for them to balance between this short-term margin expansion and long-term scale and overall size of the business. Nevertheless, they specifically addressed this to keep investors somewhat calmed with what respects to margins, but it felt as if they will utilize a high percentage of the generated cash to invest in all promising verticals.

As a matter of fact, this quarter’s acceleration is seen as “a consequence of all the investments that we have been putting into the business for several years. So, our logistics improvement, the user experience, and our investments and technology, the assortment and selection expansion, our retail business, our efforts to ensure price competitiveness”. All of the mentioned improvements led the company to surpass the 10bn in GMV mark for the first time.

What’s curious about the latter accomplishment is that it was mainly driven by Brazil and Mexico, with the latter overtaking Argentina as the second largest commerce revenue contributor to Mercado Libre. Furthermore, a whole page from the open remarks was dedicated to what the team has accomplished and is planning to do in Mexico. Several digital payments products were introduced and geographically expanded within the country. Management has been highlighting Mexico as a true growth driver moving forward and it appears to already be harvesting some results. The opportunity ahead remains immense for both e-commerce and digital payments in Mexico.

Management does not provide guidance. As final isolated highlights:

“our Advertising business remained strong, with revenue reaching the equivalent of 1.6% of GMV”

“We've been extremely pleased with the market share gains we've been delivering across the board over the last few quarters.”

“with regards to the credit card in Brazil. We more than tripled the number of cards we issued in a given quarter.”

My take

Mercado Libre had a spectacular quarter, as it’s almost always the case. What is remarkable is that, after 2022, the company is still focusing on the giant addressable market that’s still out there, but driving heavy operating leverage at the same time.

Commerce continued to accelerate with GMV and the increased take rate leading the way. Moreover, Meli has gained market share across the board. The only ‘negative’ factor from this Q was the rapid deceleration fintech revenues experienced. However, it is actually remarkable they still grew 24%. Growth digestion never happened, even after experiencing 100%+ growth rates during 2020-21. It would be normal if digestion were to happen.

Finally, in line with an idea discussed in this article, it seems as if Mercado Libre is starting to feel as a really distant leader. Or at least that’s what Peter Thiel would think after listening to the following:

“I think Latin America has become one of the most intense competitive scenarios in the world probably. We have the big American player investing heavily in the region, we have Asian players, we have local players to defend their position.”

Personal commentary

The only company remaining for an earnings review is Zoetis, which will be published in the coming week. The second part of Zoetis research will probably be published in 10-15 days, it’s already written. Hope you enjoyed the article and make sure to be subscribed to receive the next ones!

If you missed the previous ones, check them out here:

Earnings reviews (Google, Microsoft, Texas Instruments, Visa, ASML, Tesla)

Disclosure: This is not financial advice.

Appreciate your work Giuliano!