Mercado Libre continued with their stellar execution. We’ll go through the earnings as a whole and then break the review down to the particular segments.

The company reported revenues of 3bn, up 56% YoY from the previous year’s 2.1bn, and 15% QoQ. Since the second quarter of 2019, Meli has grown its revenue at a rate over 50% in 13 out of 15 quarters, many of them having grown at 60%+ and some even at 90%+.

Mercado Libre is starting to give signs of pronounced operating leverage. Costs of net revenue grew 20% YoY, making gross profit increase 70%. Gross profit margin expanded 860bps, from 40% to 48.6%. Furthermore, operating income increased from 24M in the comparable period to 349M in this quarter. This would imply the company’s operating margin stands at 11%. Lastly, net income increased from being negative 46M to positive 165M, resulting in a profit margin of 5.5%.

The last two points I want to emphasize at a business level are CapEx and Unique Active Users. Capital expenditures have declined YoY, from 196M to 112M, meaning Meli is being able to continue to run their operation at an extremely asset-light level. This led to the company doing over 1bn dollars in free cash flow over the fourth quarter of 2022.

Management has commented that CapEx was exceptionally low in 2022 and that we should expect them to increase investments throughout 2023. They mainly spoke of investing in fulfillment and logistics solutions for Mexico, a country that’s turning into a larger portion of Meli’s revenue.

“we do anticipate some incremental investments when we look at '23 versus '22 in terms of capex, primarily on the logistics front as we build incremental capacity that we are needing in some markets, primarily in Mexico”

The other field in which Mercado Libre is investing is in Mercado Ads, their advertising solution. Here’s what management said about it.

“So, I think over the last probably two or three quarters, we've been very consistent about talking about the new product deployment and how we've accelerated our focus and investments on technology and ad tech business. We've doubled the engineering headcount there in probably half a year.”

Even though disconnected from financials, this metric helps evaluate at a qualitative level how’s Mercado Libre ecosystem baring. Unique active users have increased over 18% YoY, from 82M to 97M, implying the company has continued grabbing market share across the board.

“MercadoLibre strengthened its leadership of the e-commerce market in Latin America, as our data indicates that we achieved market share gains across the entire region with Brazil and Mexico standing out” Management

Before going through each segment, here are the overall numbers at a glance:

Mercado Libre

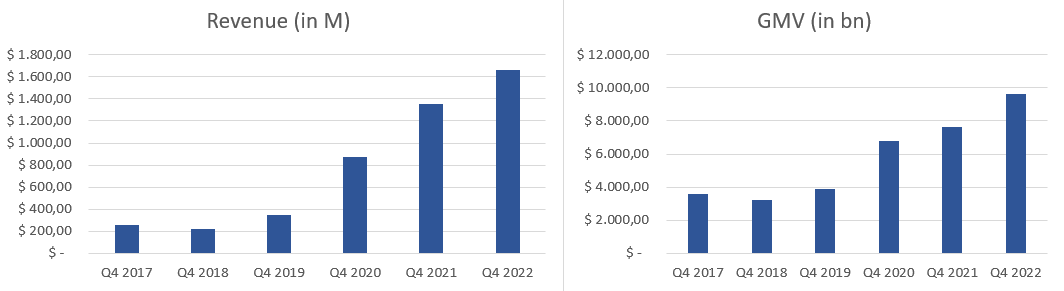

Mercado Libre (the marketplace) recorded commerce Revenue of 1.66bn, up 36% (FX neutral) from the fourth quarter of 2021. In line with it, gross merchandise volume was 9.6bn for the quarter, up 35% YoY. Over the past 5 years, both metrics have achieved a 45% and 21.7% CAGR, respectively. This gets to show why e-commerce, and particularly in South America, have such strong tailwinds. Considering the macro headwinds that have been in place and how e-commerce companies have reported overall, it is possible to conclude that South America turned out to be a resilient region.

To further measure how’s the platform’s health, we’ll go through how have the following metrics evolved. As of the fourth quarter of 2022, the company reported that 321M items were sold through the platform and that there were 406M live listings.

Items sold have increased 11% YoY and have multiplied by 4 over the course of the past 5 years. On the other hand, live listings grew by 34% YoY and have increased from 114M in 2017 to 406M in this Q. Lastly, unique active buyers have increased by 13% YoY, from 40M to 46M, achieving a 5yr CAGR of 22%.

Mercado Envíos

I thought it would be pragmatic to evaluate Mercado Envíos’ performance after the platform’s given both are interrelated. The following chart illustrates how many items were shipped with Mercado Libre’s logistics solution and what percentage did that represent out of the total number of items sold

Items shipped were 311M in the fourth quarter of 2022, up from 276M in 2021. More importantly, the company got itself to deliver 97% of total items sold, an improvement of 100bps over the comparable period. Lastly, items sold within 48 hours decreased from 80% last year to 76% this one. However, this number has overall trended upwards since the 50% registered in 2019.

Mercado Pago

Mercado Pago has had a fantastic performance for the past three years, now almost reaching 800M in revenue. Keep in mind the following chart displays revenue coming from all fintech solutions, which includes transactions done via MP and credit solutions offered by Mercado Crédito.

Mercado Libre reported 1.34bn in revenue for their fintech segment, increasing 93% YoY on a FX neutral basis, from 773M last year. This business unit has managed to grow its topline eight-fold over the past 5 years, beginning at 180M in Q4 of 2017, exhibiting a CAGR of 49%.

Mercado Pago’s performance as a whole can be examined by the total payment volume transacted through the app. TPV has grown over 80% YoY (FX neutral), from 24.2bn in the fourth quarter of last year to 36bn in this last one.

Over this past half a decade, Mercado Pago’s total payment volume has increased at a 52% CAGR. At the same time, it has achieved an almost 100% penetration in Mercado Libre’s site. Since management knew this would have eventually happen, they’ve been working on expanding fintech solutions to appeal to the common public, beyond the marketplace. Total payment volume off the platform began being 25% of the total in 2017, but it has increased to today’s 72%. This trend is fundamental since it uncaps Mercado Pago’s growth, it removes the natural ceiling the marketplace would suppose.

Mercado Pago was already a significant player in the digital payments industry, but it is becoming an extremely comprehensive solution, helping it reach more people and have more use cases.

“Now, with a complete product stack, Mercado Pago is well positioned to become a leading financial services provider in the region, enabling us to foster financial inclusion across the region.” Management

Transactions are a very appropriate indicator of Mercado Pago’s actual demand. Transactions have increased over 60% YoY. Over the last 5 years, transactions have grown at a very fast pace, going from 73M in the fourth quarter of 2017 to 1.6bn in this past quarter, exhibiting an 87% CAGR. Upon this data, we can infer people are utilizing MP to do smaller transactions, which is positive. The more used it becomes for mundane tasks, the more intricate it will get with South America’s economy, strengthening Mercado Pago’s position.

Lastly, active fintech users were 44M for the quarter. They were up 27% from the 35M users Mercado Pago had in the comparable quarter.

Mercado Crédito

Out of the total 1.34bn, Mercado Crédito amounted for 560M and grew 88% YoY. This sector’s revenue had not been reported until last quarter, we only have the last 3 year’s revenue. In 2022, credit solutions did 2bn in revenue, up from 809M in 2021 and 246M in 2020. Mercado Libre shares a lot of insights of this business unit in the quarterly presentation.

Originations increased 64% YoY, up to 2.8bn in this last quarter. Investors have been worried of the risk at which Mercado Libre exposes itself by carrying forward this sector. However, even though the yearly growth is high, origination have remained quite stable for the past couple of quarters and management is focusing on keeping risk low:

“Mercado Crédito's portfolio was broadly stable at $2.8bn as we took a cautious approach to originations. In Q4’22, our credit business delivered an annualized IMAL* spread of 48%, helped by improvement in asset quality, with our <90-day NPL falling sequentially to 10% broadly flat year-on-year.”

Revenue grew 88% YoY, but it has barely increased quarter over quarter, reflecting lower origination. Lastly, the company mentioned several times they’ve been working towards originating better quality.

Management Commentary

“all of the focus in terms of technology over the last few quarters probably begins to put us on equal footing with some of the largest and most successful technology platforms” (Referring to the ads business)

“The profitability of our Commerce business improved substantially year-on-year in the fourth quarter”

“Development of technology for Mercado Ads has been a major focus during 2022.” (…) “These efforts increased the presence of ads, thus improving monetization of the marketplace and playing an important role in revenue growth and margin expansion. We still see plenty of upside to be captured.”

“in terms of the model, we charge for both rental space, and we charge for inventory that doesn't rotate quickly enough and generates inefficiencies in terms of floor space. What we've been saying over the last few quarters is that we have dual objectives of introducing monetization behind fulfillment yet at the same time, still push adoption and usage of that service”

My Take

In absolute terms, I think the quarter was spectacular on all fronts. In relative terms, it’s been a normal quarter for Mercado Libre. 2020 and 2021 proved to be a severe issue for many companies that grew more than they were used to. Almost all of them are citing ‘tough comps’ and are seeing little to no growth, or some’s revenue is even declining. This is not bad, it is natural, when companies experience one of these abnormal periods of growths, they then have to digest it, which means they’ll experience a short term headwind. In Mercado Libre’s case, the rule does not seem to apply. In 2020, the company grew 73% to 4bn in revenue, following a 2021 in which it grew 77% to 7bn. Now, they’ve reported 10.5bn in revenue in this last fiscal year, 2022, which means another 50% growth over 2021.

Moreover, 2022 has been accompanied by increased efficiency, from all perspective, but without impacting the business. Gross margin expanded over 800bps, the operating margin over 1100bps and net profit margin 600bps. However, even though the company spent less at an overall level, Mercado Envíos kept growing penetration, Mercado Pago’s TPV grew at 80%, the marketplace grew GMV by over 30% and the credit portfolio as well.

The upside at a topline and at an operating level are very large. The company keeps expanding its catalog of offerings and becoming an ‘everything business’, now focusing more than before on advertisements, a sector they mentioned has ‘an attractive EBIT margin’.

Lastly, I think the continued investments Mercado libre has made over the past couple of years have been very rewarding, making the company the authentic and undisputed leader in every main market they operate. I believe further investments to solidify their position in Mexico can be in that line as well.

Personal Commentary

This is the company I’m most familiar with (it’s from Argentina as I am) and always am really looking forward to reading their results. Hope you enjoyed this recap, I tried to write it as fast as possible so you could extract the most value out of it.

Disclaimer: Not financial advice.