MELI Q1 Earnings Review

Mercado Libre has been growing at an extremely fast pace for the past few years and drastically accelerated during the pandemic. In the first quarter of 2023, Meli grew its topline by 35% YoY, getting to over 3bn for the second consecutive quarter. As companies get larger, it is natural for growth to slow down. However, Meli’s growth rates are coming down but quite slowly, in comparison to many others that saw themselves favored by the pandemic. This is very positive since it means the consumers’ demand for the company’s products is sky high.

Meli was once somewhat optimized for profitability, but in 2015 the company decided to double down on the opportunities they were overtaking and invest more. This made margins overall compress, falling from the 16% net profit margin at which it operated. Nevertheless, since the fourth quarter of 2021, margins started expanding again.

In the first quarter of 2023, Mercado Libre did 1.53bn in gross profit, implying a margin of 50.6%, up 290bps from last year. Operating income was 501M and its margin expanded by 1030bps on a yearly basis and 80bps sequentially. Finally, the company’s net profit margin was 6.6%, increasing 370bps.

Mercado Libre’s operating cash flows have been all over the place for the past years. However, they seem to now be consolidating at the 800M mark. In the last quarter, Meli had 859M cash provided by operating activities, strongly up from last year’s outflow and down sequentially. On the other hand, capital expenditures were 89M, below the 130-150M average of the past couple of quarters. This leaves the company’s free cash flow at 770M.

Management commentary on CapEx:

“There were certain investments in logistics that we initially had budgeted for the first quarter that have been pushed back into second, third, and fourth quarter. Our capex trajectory also will be somewhat volatile as new warehouses and new nodes come into play in different markets “

Before going into each particular segment’s performance, one piece of data. MELI has now surpassed the 100M unique active users in this quarter, across their whole ecosystem.

Mercadolibre (marketplace)

Meli’s e-commerce revenues rapidly increased with the pandemic’s boost and then came down to more normal growth rates. On this last quarter, they were 1.67bn, a 31% increase over the comparable period and barely flat sequentially. The reacceleration from 22% the fourth quarter of 2022 to 31% in this one is worth mentioning.

We will further break down the marketplace performance looking at other relevant metrics. Gross merchandise volume, for instance, was 9.41bn for the quarter, increasing 23% yearly and declining by 2% QoQ. The reason why revenue increased faster than GMV did was simply that MELI raised its take rate to 17.8%, compared to 16.7% last year and 17.3% last Q.

Lastly, items sold via the platform give a general overview of how are supply and demand trending. During the first quarter of 2023, 309M items were sold via the marketplace, up 16% YoY and down 3% sequentially. The latter should be of no concern since fourth quarters tend to be the strongest.

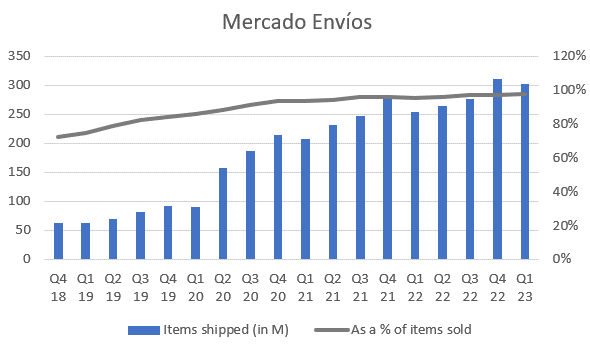

Moving forward, Mercado Envíos has been having a stellar performance for the past years. In this quarter, 302M items were shipped via the company’s logistics arm, equal to 98% of total items sold. Furthermore, 99M of these were delivered on the same or the next day, giving strong signs of this network’s value. Within 48hs, 77% of all deliveries were made. As a final footnote, the total managed network penetration was 93.4% and there were over 7400 (record) of Meli Places (hubs to drop off or pick up items).

Fintech

Within Mercado Libre’s Fintech offerings, the company has Mercado Pago and Mercado Crédito. The revenue chart will be showing both metrics together since Meli only started reporting their credit revenues in mid 2022. Anyhow, fintech revenues were 1.36bn for the quarter, growing 40% yearly and slightly on a sequential basis.

Meli’s whole digital payment ecosystem is growing rapidly, now reaching 44M quarterly unique active users, up 25% YoY. Moreover, total payment volume has been growing remarkably during the past few years, showing truly uncapped demand. It now reached 37bn dollars, up 46% year over year and around 3% QoQ.

What I want to highlight in this business unit is how rapidly off-marketplace TPV is increasing. Mercado Pago was created with the objective of facilitating digital payments within the marketplace. However, the collateral effect was that people started utilizing it as an authentic neobank, for their everyday lives. Off-marketplace TPV has grown by 13x in the past 4 years, now representing 73% of total TPV. If Mercado Pago hadn’t expanded its operations outside the marketplace, TPV would be limited by the GMV. Therefore, by being Mercado Pago a digital payments solution to all people, the total addressable market the business has, increases dramatically.

Moving on, Mercado Crédito had been gaining share of overall fintech revenue for a while, getting to 44% in the second and third quarter of last year (when data begins). 2022 and 2023 were very uncertain times in what macro concerns and, for this reason, Meli decelerated the pace at which it offers credit to merchants and consumers. This past quarter, M Crédito generated 536M in revenue, up 33% YoY.

The credit portfolio totals 3.04bn, growing on a yearly and accelerated its sequential pace once again. I’m no expert on credit risk nor on these types of business model, it’s homework I have pending. Here is the other chart Meli provides:

And, management context on the business:

“Mercado Credito delivered another solid quarter of profitability. We continue to be cautious about the risk that we take on, and, in that context, the portfolio’s size was similar to the prior quarter, and focused on lower risk cohorts. Non-performing loans are at comfortable levels. As a result, the business maintained a high margin.”

Management commentary and outlook

Management emphasized the high growth and the momentum all business units are showing. Moreover, they discussed this translated into the ecosystem surpassing 100M UAUs, but, in contrast to the previous years, also to operational leverage. Mercado Libre has been more cautious when allocating capital and the higher increase in topline compared to costs, led to margin expansion across the board.

Regarding the marketplace, one of the metrics management believes gives proof of the company’s good execution is the take rate they are able to charge to customers and merchants. The team mentioned the higher take rate was driven primarily by shipping fees, ad revenues and minor price increases to offset rising costs.

When talking about Mercado Pago, management has been clear all along the way, they want it to become a comprehensive suite of offering within digital payments. To this end, the company developed and launched several new products and services in the past quarters, while testing things like Insurtech and Savingstech. Additionally, their money-market-like return offering with instant availability has been proving spectacular for attracting money to Mercado Pago.

“So, what we have seen is a significant increase in asset under management, which is growing over 100% year over year.”

Furthermore, Meli’s team believes their credit solution is key to growing their payments ecosystem. With the objective of expanding its reach, Meli’s credit card was made available for the first time in Mexico and initiatives are being taken to increase awareness in Brazil. At the same time, they have also ‘slowly re-accelerated credit card issuance in Brazil, expanding the distribution of this product through the digital account’.

Finally, in the conference call, a topic that covered a large part of the opening remarks was the advertising business. Mercado ads continues to be a major area of investment for the company and it is starting to deliver promising results, gaining momentum:

“Mercado Libre served millions of unique buyers in the first quarter of 2023 with 7 out of 10 searches being unbranded.”

“So, on advertising, the business continues to grow very nicely. It grew at 62% year on year, which is very much in line with the growth rate over the past three quarters.”

Management also mentioned something that caught my attention. They mentioned their ‘unparalleled first party data’ and the benefits this has for their ad business. Advertising is about showing the right ads to the right buyers and, to correctly identify (or target) these people, a crucial element is data. Meli could truly turn out to be one of the greatest at targeting ads in the e-commerce space in LatAm since Mercado Libre has been gathering data for more than 20 years.

My Take

Meli’s quarter was spectacular, as have been most of them for the last years. The main ‘concern’ with the previous ones was profitability or the company giving signs of them. However, these past 2-3 quarters have shown not only a continued rapid growth and momentum across the board, but the operating leverage kicking in reveals the business true nature.

Disclosure: This is NOT financial advice.