Many companies have now reported their last quarter results. This article is intended to give an easily-digestible and short overview of the most ‘relevant’ businesses that today operate, large techs.

I have already written a detailed review of Microsoft and Google’s earnings, in case you want to dive a bit deeper into them, I’ll leave the links here.

The table below provides a financial overview of how large techs have performed during the quarter. Toplines did not change that much, with most of them being between -5% and 2% year over year. Overall, Amazon outgrew its peers as of revenue, increasing it up to 149bn for the quarter. As last earnings season, Tesla was an outlier, having grown its revenue at 37% YoY to an almost 100bn annual run rate. Tesla is still quite small in comparison to the giants, making a higher growth rate more ‘easily’ achievable.

Margins were all over the place. In almost all cases, they dropped severely from the comparable quarter. Each one of them is a whole world on its own, but in general terms, this is due to:

Tough comps. 2021 was an outlier in all of them, where revenue got way ahead and costs couldn’t keep up. The situation has now reversed.

Inflation

Lack of cost discipline (mainly due to overhiring)

The last point has already been addressed by most large techs. Amazon laid off 18k people, Microsoft 10k, Meta 10k and Google 12k. Neither Apple nor Tesla have taken the same road as their peers.

Advertisement Sector

Nowadays, almost all companies look for ways to expand horizontally and, among the 6 large techs, 4 of them now actually compete in the advertisement market.

I did not LinkedIn marketing solutions because Microsoft didn’t mention it during their conference call. Overall, the sector has been weak for the past year and it kept that way during the last quarter. At the same time, as mentioned, weakness is perceived higher because of how the advertising companies performed in 2020/21. Here are some quotes from the different management teams on the sector:

“At the same time, we saw a further pullback in spend by some advertisers in Search in Q4 versus Q3. In YouTube and Network, the year over year revenue declines were due to a broadening of pullbacks in advertiser spend in the fourth quarter.” Google

“Advertising spend declined slightly more than expected, which impacted Search and news advertising and LinkedIn Marketing Solutions.” Microsoft

“Sellers, vendors, and brands continue to look to Amazon's advertising capabilities to reach customers” Amazon

“Going into Q1, I think as I mentioned, we are – I think there’s still a lot of uncertainty around the outlook.” Meta

Amazon’s ad business is extremely strong and still demanded, heavily outgrowing its peers. However, the ad sector’s weakness narrative is not an act. The IO Fund has estimated how much money have companies been destinating to marketing. Not only shows the big impact the overall sector has had since 2021, but it also tells how big of an impact did it have in 2020/21.

Cloud Computing

This sector is the one that catches the most eyes and for a good reason. Perhaps out of all business solutions each of the 3 companies have, the one with the biggest total addressable market is their cloud computing segment. The following table displays the yearly and absolute financial performance each segment has had.

Microsoft does not report Azure’s unique financials, which is why I utilized Microsoft’s IC segment as a whole.

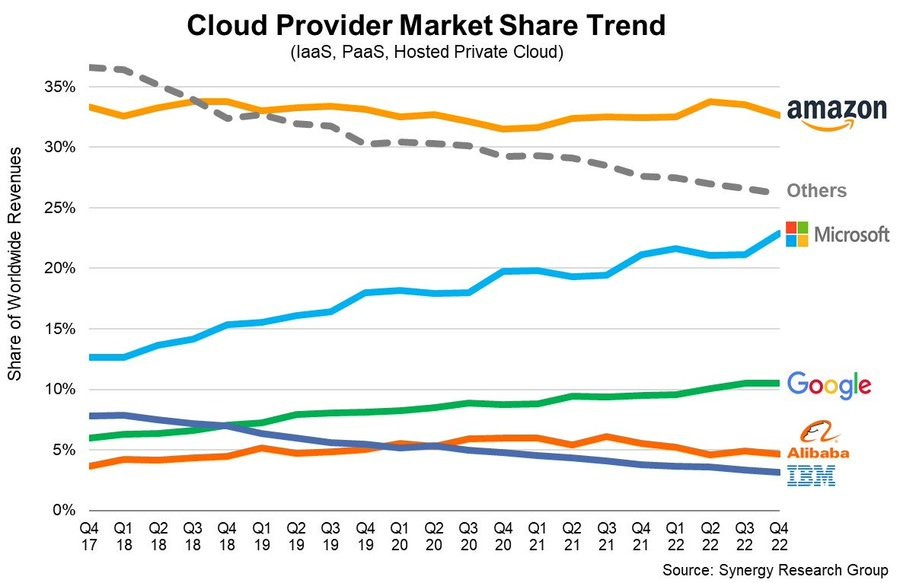

The chart below illustrates how Microsoft Azure, Google Cloud Platform and Amazon Web Services have performed on a topline basis for the past 5 years. Keep in mind Azure’s growth is reported as ‘Azure and Other Cloud Services’

All 3 have experienced major deceleration over the course of these years, but it’s only natural as they grow larger and larger (AWS is already an 80bn) run rate business. What mainly catches my eye is Azure’s high and persistent growth, which allowed it to capture a ton of market share.

Management commentary and guidance:

“We saw moderated consumption growth in Azure and lower-than-expected Growth” (..) “we exited Q2 with Azure growth in the mid 30s in constant currency and from that, we expect Q3 growth to decelerate roughly 4 to 5 points in constant currency” Microsoft

“But by and large, what we're seeing is just an interest and a priority by our customers to get their spend down as they enter an economic downturn “ (..) “So far in the first month of the year, AWS year-over-year revenue growth is in the mid-teens.” Amazon

“In Q4, we saw slower growth of consumption as customers optimized GCP costs, reflecting the macro backdrop” (..) “For Google Cloud, we remain excited about the long-term market opportunity and the trajectory of the business”

Tesla

Perhaps I’m a bit biased, but I continuously find Tesla’s performance to be extraordinary, under almost all parameters. Tesla has become an 80+bn run rate company and it’s growing its topline at 37%, while peers business units like AWS or IC are growing at 20% and 17%, respectively. Of course, it’s not how many dollars do you make, but how many dollars do you keep.

Since the company is still not fully optimized for profitability, it falls short over its peers in operating income and, even if not disclosed, probably in free cash flow as well. However, Tesla’s 2022 has been a major turn in the company’s fundamentals.

Margins were in negative territory, but they slowly climbed their way up. The most remarkable is the operating margin the company has achieved, standing comfortably at 16% for 2022, which is more alike a tech company rather than a vehicle one. I don’t want to dismiss the importance of Tesla needing to maintain it. The achievement is impressive, but it now must maintain them, which will ultimately prove the business intrinsic fundamentals.

Some key management commentaries:

“Demand far exceeds production, and we actually are making some small price increases as a result.”

“The trend is very strong toward use of FSD. And as you alluded to, the -- with each incremental improvement, the enthusiasm obviously increases. And so, I think something that still a lot of people out there don't quite appreciate is that Tesla -- of course, Tesla is as much as a software company as a hardware company, but Tesla is really one of the world's leading AI companies”

Personal Commentary

I hope you enjoyed this article. The idea was for you to have a general overview in the most concise and detailed way possible. I don’t think I achieved that, but I’ll keep improving.