All large techs, excluding Tesla, reported earnings last week and I believe it would be a good practice to recall them and extract the most important pieces.

In general terms, there are some points in common when looking at companies but, when done so as a whole, little to no points. Except Meta, all of them are still growing revenue, with Tesla leading the way.

Since all companies have several business units, I believe it would be more interesting to analyze the subgroups that arise from these monsters. At the same time, it would be insightful to approach the concerning and relevant topics.

Ad-tech Sector

The advertisement sector is, as known, cyclical, though I believe there’s a misconception regarding this. When the economy slows down and gets tough, companies diminish their spending overall. But, as in every market, money flows to quality. In the ad sector, the more cyclical offerings are the ones that are low quality, which would be the first a company would consider on cutting. Google search is the perfect example of a high-quality ad offering, its resiliency has proved over and over for the past decade.

Overall, Google ads grew this quarter, driven by Search; Meta’s revenue fall for a second quarter in a row; Amazon is still outgrowing its peers by a lot though it does not disclose its operating results.

Google’s operating margin is from all services offered, from which these 3 represent an 85% approx. Margin compression is alarming, which may be mainly due to the abnormal headcount increase during the quarter. However, I’d wait some quarters to see if the actual fundamentals from Google ads have deteriorated.

Some of Google’s remarkable extracts from the conference call:

“There’s 1.5bn MAUs in Youtube Shorts, 30bn daily views”

“Search had healthy fundamental growth. The largest driver of deceleration was ‘tough comps’”

The other player in the sector, which does not disclose it as a separate segment is Microsoft. It participates in this market through Linkedin marketing solutions, as well as their search ads solutions (through bing). In the conference call, management mentioned two noticeable things:

“weakness in Marketing Solutions from the advertising trends”

“Search and news advertising revenue ex-TAC, increased 16 percent and 21 percent in constant currency”

Cloud Segments

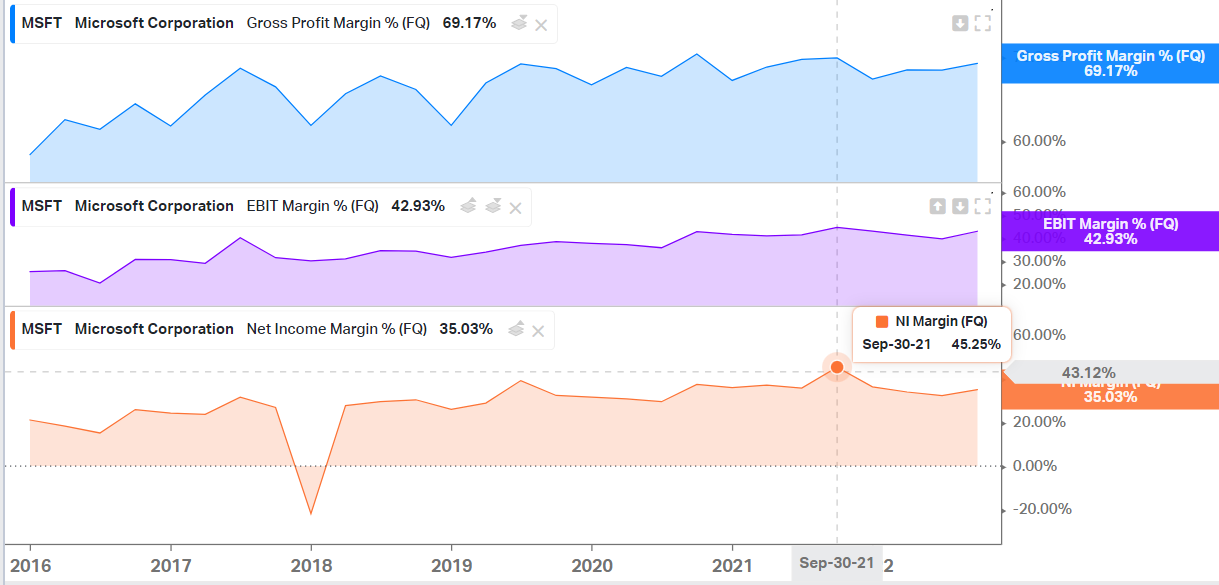

The cloud space is acting as if nothing were happening. We are seeing sequential deceleration, but deceleration is only natural to companies as they grow. This segment is characterized by its strong fundamentals, as Microsoft shows with its 43% operating margin, so it’s good seeing the three companies rapidly growing.

Google Cloud Platform is still lagging its peers in terms of market share, but it seems to be getting closer to them. Growth on GCP has accelerated sequentially and its competition has guided for about 20% growth for IC, with about 30% growth in Azure; and Amazon has guided AWS to grow 20-25%. Google could take advantage of its momentum and grab some market share.

Helpful extracts on the topic:

“We’re pleased with the momentum in cloud (…), unveiled more than 100 new products, announced new relationships and nearly 300 new capabilities to support hybrid work.” Google

“Our current backlog balance for Q3 is $104 billion. So it's about a little less than 60%, I think about 57% up year-over-year.” Amazon on AWS

“Arc customers doubled; Azure ML rev grew 100+%; Github crossed 1bn in ARR; Cosmos DB is the go-to database.” Microsoft

Margins

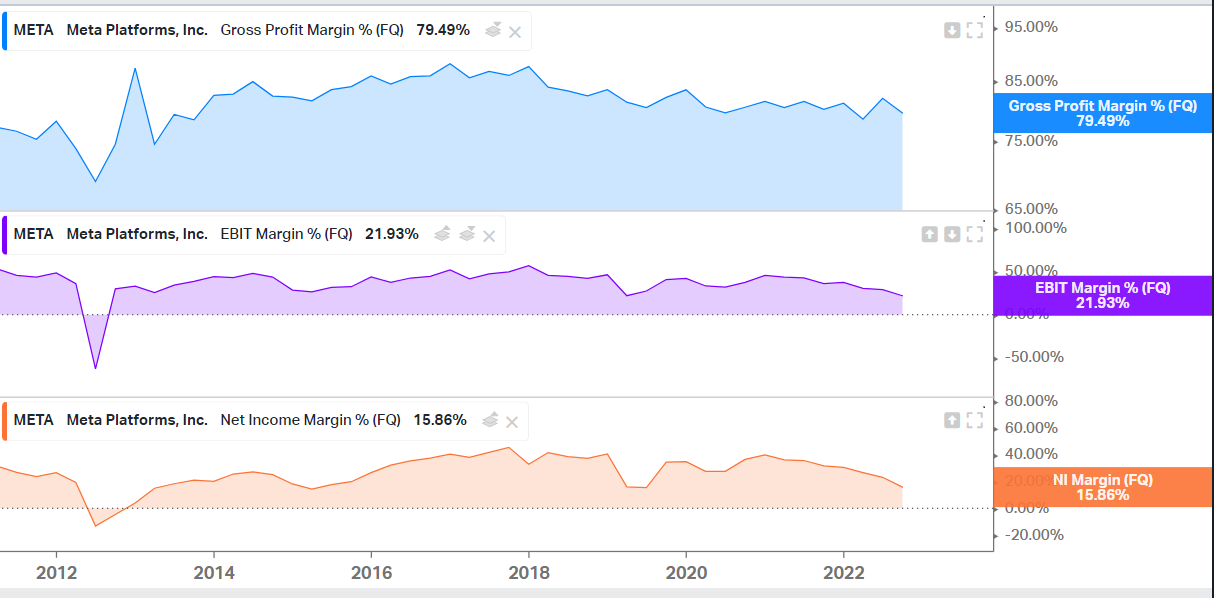

This was the most concerning topic among Microsoft, Google, Amazon and Meta. Meta will be discussed in the last section of this article as a separate item.

Microsoft had a severe yearly margin compression, but it doesn’t seem concerning at all. As shown below, it is not that the business fundamentals actually deteriorated, but rather that 1Q22 saw a major spike in operating efficiency, making it a really tough comp to compete with.

The main disparity between both Net Income margins was due to taxes provision.

Google also saw some concerning margin pressure this quarter. In this case as well, margins are still near their 10yr averages. The apparent yearly deterioration is mainly due to the spike in operational efficiency they had in 2021, when demand was absurdly strong. Here’s what management said about it:

“some of the margin upside last year was due to timing issues. And we had a very strong growth in revenues, a surge in revenues and a lag in investments that we said was a timing difference. And you are seeing some of that here.”

In Google’s case, it may be a bit more concerning since the decade trend seem to be downwards, as opposed to Microsoft’s. Still, few more quarters of normalization will tell, we have to leave behind that abnormal 2021.

The other factor worth mentioning is the headcount increase, which was of 36k employees, up 24% YoY. It is by no means ignorable. assuming an average salary of 100-200k, the extra operating cost oscillates between 3.6bn-7.2bn. Worth to keep a close eye on how they move going forward in this regard.

Amazon’s operating efficiency has been under pressure for some time now so it’s nothing new. Regarding this, management said the following: “Our network doubled over the last 2.5 years. While we're making strides in productivity and network optimization, we still have work to do there.” They also mentioned rising energy and fuel costs were impacting their overall operating margin.

Tesla’s Operating Leverage

Tesla reported spectacular ER in my opinion. Summary:

Revenue grew 56% to 21.45bn

GPM decreased 150bps

Operating Margin increased 260bps

Free cash flow was 3.3bn, implying a margin of 15% (an improvement of 600bps)

Net Income was 3.3bn, up 103%

Reiterated 50% growth in annual deliveries on a multi-year horizon

Tesla has been expanding its margins for quite some time now. The impressiveness of the achievement is mainly due to the very tough macro and of Tesla being allegedly an ‘automotive company’. Elon said margins even suffered from headwinds so, once past this, they should continue to expand. The main concern regarding the quarter may be the pronounced mismatch between deliveries and production. Regarding it, Elon mentioned the following: “we actually have to smooth out the delivery of cars intra-quarter because there aren’t just enough transportation objects to move them around.” Another gap is expected in Q4.

One more extract regarding a much-awaited topic, Full Self Driving:

“We’re expecting to release the full self-driving software to anyone who orders the package by the end of this year”

Meta

Meta experienced its second revenue decline in history, the first one being on Q2 this year, and is expecting a third YoY decline on Q4.

The business has always shined for its fantastic fundamentals, getting an 80+% gross margin, a 40+% EBIT margin and a high 30% net income margin. However, for the past two years approximately, Meta has been changing its focus towards a very different thesis (metaverse). This change in focus is making it overspend to get this new business unit going and this overspending is quite abrupt. Meta is still having an 80% gross margin, so the damage is being done at an operative level. YoY, total costs and expenses grew 19% while revenue declined 4%. Costs are being driven by R&D, which makes sense given their shift in thesis.

The second extra item worth mentioning is Capital Expenditure. Year over Year, it increased 111%, which made free cash flow be the lowest in years, barely breakeven.

This is a very risky play management is doing, impossible to determine if it’s the right thing to do or not. At the moment, financials are suffering. On the other hand, I’d like to highlight some keynotes on the actual core of Meta, its family of apps, which appears to be doing well, despite everything.

Family of Apps MAUs increased 4%, to 3.71bn

140bn Reels plays across Facebook and Instagram each day, increasing 50% from six months ago

Combined revenue run rate across Facebook and Instagram Reels crossed 3bn.

Billions of people and millions of businesses use WhatsApp and Messenger every day

Click-to-Messaging ads is the fastest ad product, with a 9bn annual run rate

Click-to-WhatsApp passed 1.5bn run rate, growing more than 80% YoY

Meta is spending a lot of money with unforeseeable and uncertain returns and it will continue doing so for the coming future. The core of the business is actually doing fine, but this absurd spending is making the overall business fundamentals trend down.

Personal Commentary

I covered what I considered to be the most concerning and interesting topics among the group. If you believe I missed something, feel free to contact me through Twitter’s DM. Hope you enjoyed the article!

Excellent updates my friend. You own any of these names?