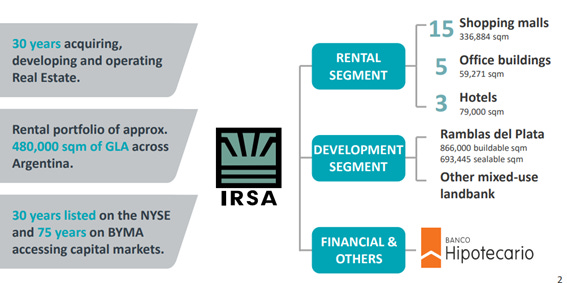

Irsa is an Argentinian company with a large real estate portfolio, has been publicly traded for over 30 years, never defaulted on its debt, and lately went through a complete restructuring. I suspect the risks present in the business have been greatly diminished by management’s past 5-years actions and that the business itself is simple enough to be understood well. Moreover, I believe there’s strong cash generation capacity from the portfolio of assets it owns. When complemented with a healthy balance sheet, high insider ownership, and cash returned to shareholders, Irsa appears to me as a promising investment.

Although I’ve largely ignored engaging and depending on economic analysis in the past, I must observe that the main reason I got to research Argentinian companies, besides the fact that, incidentally, I live in Argentina, is that the country is facing huge structural changes. The economic environment no longer seems to posit a mid-term threat and, if reforms get fully implemented, it might not even posit a long-term threat. Notwithstanding this, considering the country’s history, it remains a risk present in the investment.

Having said this, I became more familiar with how countries’ prosperity manifests itself. Two indicators I’ll remark on are low-level, controlled, inflation, and a continuously increasing GDP per capita, which entails the average individual getting increasingly wealthier. In consequence, this boosts consumption and investment, both local and, once the effects are internationally recognized, foreign as well. The obverse might also occur if the government inspires confidence. It’s thus that I was inclined to investigate Argentinian securities and came across Irsa, which could potentially benefit from all tailwinds embedded in an economic recovery and growth thereafter. It’s a perfectly fine business that has been subject to Argentina’s calamities.

I’ve been thinking about Irsa since May 2024, but decided to wait for further assurance about the country’s future prospects. When these things occur, there’s too large a number of risks that escape the common spectrum thereof. More importantly, my intention is not only to play re-ratings, but hopefully benefit from an intrinsic value increasing longly after the investment is made. The latter could’ve only been assured, to some extent, if the country’s restructuring solidified.

Finally, before going into the analysis, there’s an element that’s got me puzzled for the past couple of months. Irsa is technically controlled by another publicly traded company called Cresud, which has a 53% stake in Irsa. Eduardo Elsztain is the person who essentially owns Cresud and Irsa, whose family members are on both boards and running the companies. I cannot infer to what extent this dynamic affects Irsa’s operations and equity holders, probably due to my ignorance.

However, I’ve always been suspicious of Argentinian management teams, having anecdotally heard of how they operate in general. Although incredibly talented, there’s always a sense of shadiness. There are too many things going on. Maybe this changes hereafter, but it’s a risk I cannot fully grasp that I thought should be mentioned beforehand.

I believe the past 5-years actions, track record in debt payback, and insider ownership, partly insulate equity holders from being taken advantage of. Furthermore, the business’s income is very high margin, mostly from royalties, and generates a lot of cash. I believe the chances of the large underlying margin of safety being eroded are incredibly low. Nonetheless, I think these risks should be reflected by appropriately sizing the position.

Business Overview

Irsa is, at its core, a real estate company with operations mostly centered in Argentina’s capital, Buenos Aires. It focuses on land development and buildings for various purposes. Over the decades, the company has acquired and developed shopping malls, office buildings, and hotels. On some occasions, Irsa acquires stakes in such enterprises. Management has complemented this by acquiring land for future usage and obtaining concessions for certain entertainment and convention centers.

Since Elsztain acquired and started running Irsa in the 90s, the company slowly began constructing its portfolio. Shopping malls were under a vehicle called Alto Palermo Centros Comerciales (APSA), in which Irsa had a 95% stake. The office portfolio was separately managed.

In 2014, both segments were merged under a single vehicle called Irsa Propiedades Comerciales (Irsa CP), which operated as a subsidiary. The rationale behind the decision was to increase efficiency and improve the cost structure of the whole corporation.

Over the subsequent years, Irsa used to pay a portion of its dividends in Irsa CP shares. In 2017, the company sold an 8.1% stake in the secondary market for $140M. After this transaction, Irsa held an 86.5% stake in Irsa CP.

In pursuit of further simplification of the corporate structure, increase efficiency, better incentive alignment, and improved liquidity, management decided to merge Irsa and its subsidiary in 2021, Irsa CP, where Irsa would be the absorber. The combined entity would then own all assets and obligations, presented on a single balance sheet. After the event, shareholders approved in the general meeting of September 2021 for Irsa to issue $152M in equity.

Shopping portfolio

Irsa’s shopping portfolio consists of 16 shopping malls, one of which was purchased in November of this year. Nine of these are located in Buenos Aires, whereas the remaining 7 are distributed throughout the country, though concentrated in major cities. Two malls are in Córdoba, and one in Santa Fe, Rosario, Salta, Neuquén, and Mendoza. It is to be observed that Córdoba, Rosario, Salta, and Santa Fe are the 3rd, 4th, 7th, and 8th, most populated cities in Argentina, with populations between 570,000 and 1,600,000. CABA, where malls are to be found within Buenos Aires, has a population of over 3 million people.

In aggregate, Irsa has approximately 370,000 sqm in gross leasable area across the portfolio and 1,485 stores. Collectively, they get tens of millions of visitors per year.

The company follows a dual billing policy within shopping malls. Tenants pay a fixed base rent and a variable component, which is a percentage of the tenant’s gross sales, generally ranging between 2-12%. Although Irsa collects the highest amount among both, allegedly, I believe it is the case that the contract seems to establish that tenants’ payments must always exceed a certain minimum. Nonetheless, in times of economic pressure, which has systematically been the case in Argentina, Irsa has been understanding with people, sometimes working out different payment schedules.

Combined, this base and variable rate make up almost 75% of the total revenue that shopping malls generate for Irsa. The remainder comes from other services, most of which correspond to admission rights, parking, and commissions. Key money and the brokerage fee must be paid in advance and when lease renewals effectuate. As of 2019, the amounts were 5x the base rent for the brokerage fee and 8x the base rent for the admission rights. These have not been disclosed as of the more recent past, but I suspect remain fairly in those ranges, considering Irsa’s reported revenue from these sources.

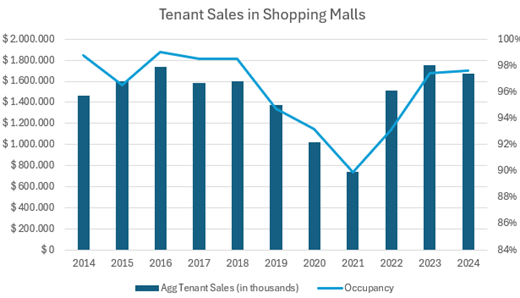

The following chart illustrates the percentage of revenue that the fixed and variable components represented of total rental income. The lowest rental income that shopping malls generated was $37.9M in 2021, with $23.9M being base rent, and $14M corresponding to the royalty on gross billings. Rent derived from a percentage of gross billings seems to have been increasingly taking share of total rental income. This suggests either that stores are doing increasingly well, or that there’s been some change in Irsa’s royalty fee. I’m inclined to suspect that, if the economy recovers and begins to grow, this source will contribute meaningfully more to Irsa’s rental income.

Aggregated tenant sales finished a mostly flat decade. In 2014, the portfolio of malls had total tenant sales of $1.46 billion, whereas in the fiscal year 2024, tenants had sales of $1.67bn. I must observe that Irsa’s fiscal year starts and ends in June of the calendar year. As of the writing of this report, namely December 2024, Irsa is finishing the second quarter of its 2025 fiscal year.

Notably, occupancy levels in shopping malls remained high, mostly above 94%. In the period 2019-2020, the country went through a severe recession, followed by the pandemic, which was managed quite peculiarly by the Argentinian government. For the whole of the pandemic, Argentina was one of the most restrictive countries. Overall closures had a negative impact on sales, which was enhanced by lower tourism levels.

What’s interesting about Irsa’s portfolio of real estate assets is that they are high quality and require very low levels of expense for continued maintenance and operation. The gross margin that Irsa has on revenue generated by shopping malls has been around 90% for the past 8 years. The operating margin has been more volatile because of around $25M in mostly fixed OpEx. When malls have normal years, with tenant sales around $1.4bn, Irsa’s operating margin on shopping malls is around 70-75%.

Note: The operating margin is computed on an adjusted basis. I took out the fair value adjustments that run through the p&l every single year.

Even though the book value of a business is rarely a precise estimation of its economic value, I believe there’s a huge dissociation between both with this company, which causes a two-fold problem, namely: (i) very volatile income statements; (ii) it’s much harder to assess Irsa’s earnings power at a first glance.

On the first point, I think most investors, when they come across an awful income statement, the company turns into an easy pass, which is perfect for a potential misprice to occur. In 2023, for instance, Irsa’s reported operating margin on malls was 49%, instead of the adjusted 73% margin. This is more pronounced with their office portfolio and land development segment, which largely impacted the company’s overall operating margin.

Irsa reported 692bn pesos in carrying value for their shopping mall portfolio as of June 2024; an amount that is equivalent to $513M. Over the past 5 years, the company has written down these assets for a total of $41.8M. This leaves them at 5.1x their adjusted FY24 operating income, or at 5.7x their reported operating income. This would mean Irsa is carrying its 15 shopping malls, excluding the last acquisition, at $1,531 per leasable square meter. In essence, a group of assets that have systematically generated lots of cash, even through terrible recessions, is carried at such a value.

The company has not only focused on acquiring and building shopping malls, but also on expanding individual ones. Over the past time, Irsa spent great effort in acquiring locations, land, buildings, or houses, next to constructed malls so that they could expand their operations. This way, Irsa has increased the shopping portfolio’s GLA by 53,521 square meters.

Since 2018, total tenant sales per square meter have averaged $4,110. By extrapolation, we find that Irsa’s expansions have led to approximately $220M in extra tenant sales per year. If we assume Irsa’s take rate on that is 5%, then the company increased its revenue by $11M annually. When operating at a 70% margin, this in turn translates into $7.7M EBIT. These numbers must of course be taken with a grain of salt, for the economics differ between malls.

The most recently completed expansion was in 2020, to Alto Palermo, which increased its GLA by 3,900sqm. During FY24, Alto Palermo has 20,733sqm of GLA, and reported total tenant sales of $217M, implying $10,500 in sales per square meter. With this in mind, Irsa might’ve increased total tenant sales by $41M with this last expansion, which translates into $2M in revenue and $1.4M in EBIT. Although the actual investment seems to not have been disclosed, Irsa estimated it at $28.5M before construction.

After considering non-rental income, the expansion might yield 6.5% per annum, though there may be some boost to all store sales. I must nonetheless observe that Alto Palermo is the mall with the highest sales per sqm in Irsa’s portfolio. It also probably holds the best location, and I ignore to what extent this impacts the investment required. Although it is not a mind-blowing yearly return, I can’t picture how it could cease to yield for at least a couple of decades. Furthermore, it’s an investment in tangible, high quality, assets, which have tended to preserve wealth very well in Argentina. This idea is at the core of Elzstain’s approach to business.

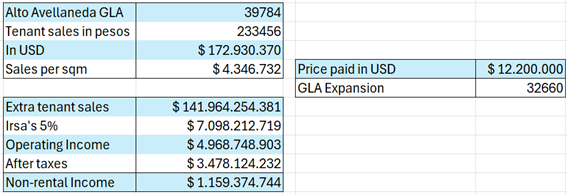

In August of 2024, Irsa acquired a location adjacent to the Alto Avellaneda mall for $12.2M. The property has a total area of 86,600sqm and buildable area of 32,660sqm. As of its current numbers, Alto Avellaneda’s tenants generate $4.300 in sales per sqm. Considering the extra GLA, this might translate into over $140M in total tenant sales. With a 5% average royalty and 70% operating margin, Irsa’s incremental EBIT would be $4.9M. After taxes, this leads to $3.47M in NOPAT. However, if we remember that Irsa’s income has a non-rental part, equal to ¼ of the total, we get that non-rental income on this expansion might be around $1.15M. The ultimate return on capital will depend on construction costs, but economics seem encouraging, mainly due to the life expectancy I suspect these assets have.

The last case I’ll mention in this line is a very recent one. On December 3rd, Irsa announced the acquisition of Terrazas de Mayo, a shopping mall located in Buenos Aires, outside the main part of the city, which is where most of its other malls are. The shopping has 33,720sqm of GLA, 90 stores, and 10 cinema theaters. Irsa agreed to pay $27.75M, 60% of which has already been paid. It’ll be unclear what the economics of the deal are until Irsa discloses the mall’s numbers (if it does). Terrazas de Mayo presumably has 7 million visitors per year.

Lastly, Irsa carries all-risk insurance for its portfolio of shopping malls, which would cover damages caused by most natural phenomena and social outbreaks. At the store level, tenants must secure adequate insurance. If the loss they experience upon an adverse event exceeds the proceeds from the claim, Irsa might face a loss.

Office portfolio

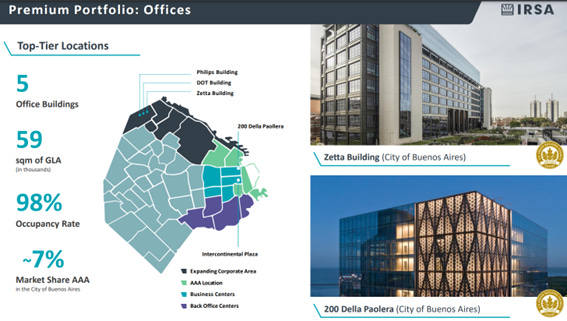

Irsa has 5 office buildings, although some are not wholly owned, for the company might have sold floors or units within them. This is the case of Della Paollera, for instance. The following image illustrates Irsa’s office portfolio, which, collectively, adds up to 59,000sqm of GLA.

Leases tend to have an average term of between 3 and 10 years, are generally stated in US dollars, and rates are mostly at market values.

In contrast to the shopping malls, what’s interesting about the office portfolio is that Irsa has placed great emphasis on diminishing its footprint. The company sold numerous units and floors over the past couple of years. As of 2018, the office portfolio had an aggregate 115,000sqm of GLA, whereas it finished the third quarter of 2024 with 59,000sqm. It must be observed that, at the same time, Irsa built and added a building to the portfolio, called Della Paollera, which is located in a premium area of the city.

Della Paollera offers a great illustration of Irsa’s past years’ rationale. Irsa began its construction in 2016 and inaugurated it in December of 2020, although work progress in June of 2019 was 95%. Throughout construction, the total investment presumably amounted to $110M, granting the company 30 office floors, or 35,000sqm of GLA, and 316 parking spaces. Over the past 4 years, Irsa has sold 23 floors for a total consideration of $232.2M, equivalent to $7,631 per square meter. After these sales, Irsa still owns 3 floors.

In addition to this, in 2021, Irsa made 2 large sales. The Bouchard 710 building, acquired in 2005, was sold for a total price of $87.2M; for it had 15,000sqm of GLA, Irsa sold it for $5,800/sqm. On the other hand, the company also sold 13 floors of Torre Boston for $83.4M. Considering the 13 floors had a total of 14,640sqm of GLA, each square meter was priced at around $5,700.

In April 2022, Irsa announced the sale of the República building for a total price of $131.8M. The building had 19,885sqm of GLA and 178 parking spaces. 80% was paid in cash, and the residual was in the form of land, namely 46 hectares in Buenos Aires, the province. This land counts with 521,000sqm of buildable area.

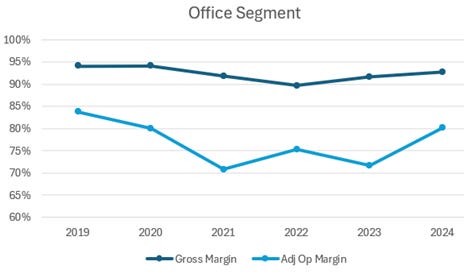

Irsa’s office portfolio is mostly composed of premium buildings, which is on which I’ll base the following chart and numbers. Since 2020, and ever theretofore, the rental price per square meter has been relatively stable, averaging around $24-$27/sqm. Occupancy levels in these premium offices stayed at 80%+ even through the pandemic, exhibiting resilience.

To shed some light on the attractiveness of the above-mentioned sales, I’ll utilize the last sale of a Della Paollera floor, which was 1,197sqm. At a $24.4/sqm monthly rental rate, the floor might’ve been rented for around $350,000 per year. When considering its selling price of $7.1M, its cap rate would have been around 5%. It’s worth noting that this floor sale price was below the last few years' average.

The office segment has generated total revenue of $18.1M, $12.6M, and $12M in 2022, 2023, and 2024, respectively. This is largely attributed to the company’s reduction of the portfolio. Margins have been systematically high since expenses associated with floor rentals are quite negligible. Notwithstanding this, Irsa had to do severe write-downs of their office assets due to the economic environment, as it did with shopping malls. Over the past 3 years, the reported operating margin for the office segment was -101%, -27%, and -348%, from 2022-24 respectively.

The carrying value for the office portfolio was $225M as of June 2024, implying $4,385 per square meter. This was down from almost $420M in 2022, when the “fair value” per square meter was estimated at $6,515.

To conclude this segment, the following chart captures management’s historical thesis for investing in real estate assets; and, more specifically, in premium real estate assets whenever possible. The value per square meter of constructed high-tier properties has tended to rise in Buenos Aires.

Hotels

As of November 2024, Irsa owns a stake in 3 hotels, all of which were acquired before the turn of the millennium. The company owns 100% of Libertador, 76% of Intercontinental, both located in Buenos Aires; and 50% of Llao Llao, a very exclusive and symbolic hotel located in Bariloche, in the southern part of Argentina.

Throughout the past couple of decades, all three hotels have done very well, except in 2020-21 due to the pandemic. Their public consists of wealthy Argentinian families and tourists. This feature has been particularly helpful for the portfolio's continuous resilience. Nonetheless, the Argentinian currency's latest appreciation in the parallel market, and if it happens hereafter, would pose a tangible headwind to the business, for it makes things more expensive to tourists and, to the extent that salaries do not catch up, to the Argentinian population as well.

Occupancy has been around 60% on average in the different hotels, with Llao LLao’s being higher and with a much higher rental rate.

The Hotel segment generated revenue of $45M in FY24, up from $41M in 2023 and $25M in 2022. Irsa does not tend to make fair value adjustments in the same manner as it does with its offices and shopping malls, for which the reported headlines are representative of the segment’s economics. The gross margin was 53% during 2024, the highest it’s been since 2019, and the segment’s operating margin was 29%.

The hotel segment is the lowest margin segment Irsa has. Moreover, it has a fixed cost component that represents a much larger percentage of total sales than other segments. This has caused the segment to operate at very volatile margins. When sales contract, margins tend to fall; the obverse is likewise true. I would argue that the pandemic and Argentina’s recession make this seem scarier than it would in a normal economy. Absent both extraordinary elements and hotels might be seen as perfectly fine businesses.

Irsa carries hotel assets at $23.4M on the balance sheet, slightly down from $24.8M in 2022. Over the past decade, there has not been much activity in the form of buying or selling assets in this segment. It’s only worth noting that Irsa sold its 49% stake in a hotel located in Rosario for $4.2M in 2015.

Sales and Development Segment

Historically, Irsa has re-deployed most of the cash generated in the purchase of land, buildings, and for obtaining certain concessions. The purpose of these is quite varied; some are for expanding the shopping or office portfolio, and others to keep potentially valuable land in reserve for future usage.

The segment has generated $4M, $12M, and $6.8M in sales during 2022, 2023, and 2024, respectively. However, this segment affected Irsa’s p&l the most. Assets included are carried at $581M in the balance sheet, which is substantially below 2023’s $790M, and 2022’s $863M. Absent the fair value adjustments, mostly of the sales and development segment, Irsa would have generated decent levels of profit, at naturally good margins. This, however, does not affect the company’s capacity to generate cash flow.

Irsa’s recent years are characterized by the company’s concentrating operations on shopping malls and offices. I believe this is materially changing and will highly influence the company’s investments moving forward. Although Irsa will continue to expand their currently held assets and acquire new ones when opportunities arise, it seems that management will more pronouncedly focus on the residential market.

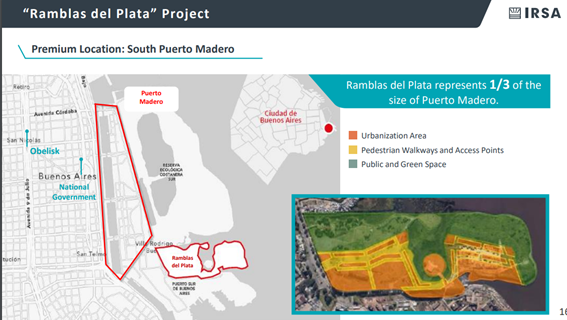

Ramblas del Plata, previously known as Costa Urbana, is a project that management has shown excitement about for several years. Ramblas del Plata is a 70-hectare land with 866,000sqm of buildable area, but of which 71% will be destined to public use. Irsa carries it at $359M on the balance sheet. The land is in a very peculiar location in Buenos Aires. It’s next to Puerto Madero, a premium area within the city that has experienced great success since it was constructed in the 90s.

The company expects this to be a 10–20 years project, to which Irsa committed a total investment of $40M. The rest will be financed by buyers and worked out through agreements. After it’s finished, the company expects it could be home to 6,000 families, with capacity for over 10,000 houses.

Irsa went through a couple of years seeking approvals and certification required to begin constructing Ramblas del Plata. In the conference call held in November 2024, management mentioned the company is almost at the final phase of compliance. At any moment they could get the last paperwork ready and start the project shortly thereafter.

In late November, another announcement was made, alongside the acquisition of Terrazas de Mayo. Management pointed out that Irsa made progress in the commercialization of the project. The company received offers for 126,000 square meters, which represents 18% of the total sellable area. Should all of these materialize, Irsa would receive $40M in cash and the right to keep 16,500 square meters in functional units of fully constructed area. Over the next couple of months, Irsa would presumably start with building the infrastructure if the deals close.

Irsa’s Focus on the Residential Market

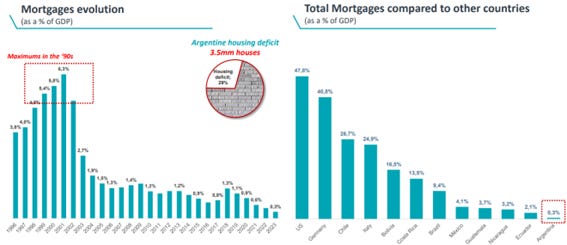

I have addressed the fact that Irsa has lately placed more emphasis on shopping malls, offices, and, to some extent, hotels. In Argentina, for over a decade, there’s been incredibly limited access to credit. The mortgage market somewhat thrived in the 90s and never recovered. Given how large of a purchase apartments and houses are, only a handful of families engaged in these. Residential real estate, if to anyone, only appealed to investors. However, this started to change.

One of the core tenets of Milei’s presidency is deregulation. Since December 2023, when his mandate began, his team has made great effort in deleting regulations across most markets within Argentina, including real estate. Multiple laws have been passed to congress, others by decree, and Milei’s commentaries seem to suggest this trend should continue.

Rental supply in Buenos Aires already reflected the increased simplicity and the fact that the government won’t intercede, or not as much as before, in private transactions. After this occurred, prices started to pick up and seemed to be looking for an equilibrium. Construction costs, due to the devaluation of Argentina’s currency, have been high for the past 2 quarters, but should also start trending towards an equilibrium, where it’s feasible to engage in real estate projects. If salary growth continues to outpace inflation, families will become increasingly wealthier, permitting them to afford rentals, at first, and then aim for more expensive ones.

On the finance side, Argentina’s risk premium in the bond market dropped from over 2000bps to around 700bps. Not only does this allow the government to borrow at lower rates but complementing it with a rapidly decelerating inflation allowed for a decrease in interest rates, which spread throughout the whole economy. Argentina’s central bank interest rate exceeded 100% in late 2023, yet it’s now at 32%.

The other important factor is Milei’s policy of not overspending on their income. The government thus far registers a budget surplus for 2024 and the president’s comments suggest that frugality will continue to be core to their strategy. Prior to this occurring, it’s highly likely that private banks focused on lending to the government, but now they’ll look for new customers, who’ll end up being Argentinian citizens.

Partly due to these reasons and many other presumably positive indicators of the country’s administration led to the rebirth of Argentina’s mortgage market. Mortgages are unbelievably important for the aggregate of a population to be able to purchase homesites. If mortgage rates are accessible, this should tend to strongly increase demand for real estate. Irsa seems thus very well positioned to capture a potentially big, rising, market.

During Irsa’s conference call, held in November of 2024, the team highlighted their feeling of the market. Tides seem to be turning. They mentioned that recent government actions are having a positive effect on the residential market.

Irsa plans to carry out two more residential projects, namely Del Plata Building, which will be in a great area of Buenos Aires and count with 720 apartments; and La Plata Project, which will have 100,000 of buildable square meters, out of which 22,000 will be destined to a new shopping mall.

Banco Hipotecario

In 1999-2000, Irsa acquired a stake in Banco Hipotecario, which subsequently increased to 29.9% ownership, which they’ve held since. The bank was founded in 1886 and has been a leader in mortgage lending within Argentina. During the late 90s, its privatization process began, but the government that succeeded the one that started with it decided to retain a controlling stake in Banco Hipotecario. As of 2024, the Argentinian government remains the controlling shareholder. Nonetheless, 7 of Irsa’s executives and directors sit on Banco Hipotecario’s board.

Banco Hipotecario has a 62-branch network that extends to all provinces across the country. The company had ARS 372bn in equity as of June of 2024, equating to around $275M, and total assets of around $1.8bn.

For it has been a household name for 130 years, the bank is very well-positioned to capture an upside in Argentina’s mortgage market. In addition to this, there is a possibility of Banco Hipotecario and Irsa cooperating on projects, creating very valuable synergies. While Irsa plans to undertake big residential projects, Banco Hipotecario looks to finance home buyers. It is to be determined how the economy continues to fare, but future prospects appear to be good, giving a chance for demand of these loans to explode.

In the fiscal year that ended in June of 2024, Banco Hipotecario approved dividends distribution of around $20M, of which $10.5M were distributed to Irsa. The bank operated profitably over the past 2 years, had returns on equity above 15% and its balance sheet is healthy, with liquidity exceeding total deposits. If the mortgage market effectively recovers and grows, Banco Hipotecario could pay dividends to Irsa for a long time to come.

La Rural – Special Mention

In the city of Buenos Aires, there is an emblematic building called La Rural, which is one of the most well-regarded convention centers in the country. It was founded in 1878 and serves as the place where fairs, exhibitions, congresses, and various events, including those business-wise, are held. La Rural has multiple millions of visitors every year.

Irsa acquired its 50% stake in La Rural by purchasing in two separate years, namely 2011 and 2016. The building generally requires a governmental concession to be utilized, which Irsa had formerly gotten. Irsa renewed its concession in 2022, extending its usage period of La Rural until 2037. In order to get this extension, Irsa agreed to pay $12M in annual installments.

Irsa received slightly over $1M in dividends from La Rural during the fiscal year 2024. The company’s interest in La Rural’s total 2024 income was $5.6M, and they carry their equity interest at $7.8M in Irsa’s balance sheet. The following chart includes the ownership, equity value in La Rural and Banco Hipotecario, and Irsa’s interest in their 2024 income. It must be observed that both businesses grew by over 150% yearly.

Cash Flow and Distribution

Irsa has been cash flow positive for more than a decade, with no year being an exception. During 2022, 2023, and 2024, the company generated $75M, $100M, and $76.6M from operating activities, respectively Moreover, in recent years, Irsa’s sales of investment properties outweighed purchases, creating a large inflow of cash.

Instead of reinvesting most of this capital, Irsa reduced its debt. The company had historically operated with relatively high leverage. But seemingly ever since a change in directors, and the merger with Irsa CP, capital has been used to deleverage the business and return a part to shareholders.

Considering Irsa’s high recent activity in the debt market ($52M issued in February and $42M issued in June of 2024), it might be expected for management to leverage up the balance sheet. However, I wouldn’t expect the business to return to prior levels. As of early 2025, net debt is around two times rental EBITDA.

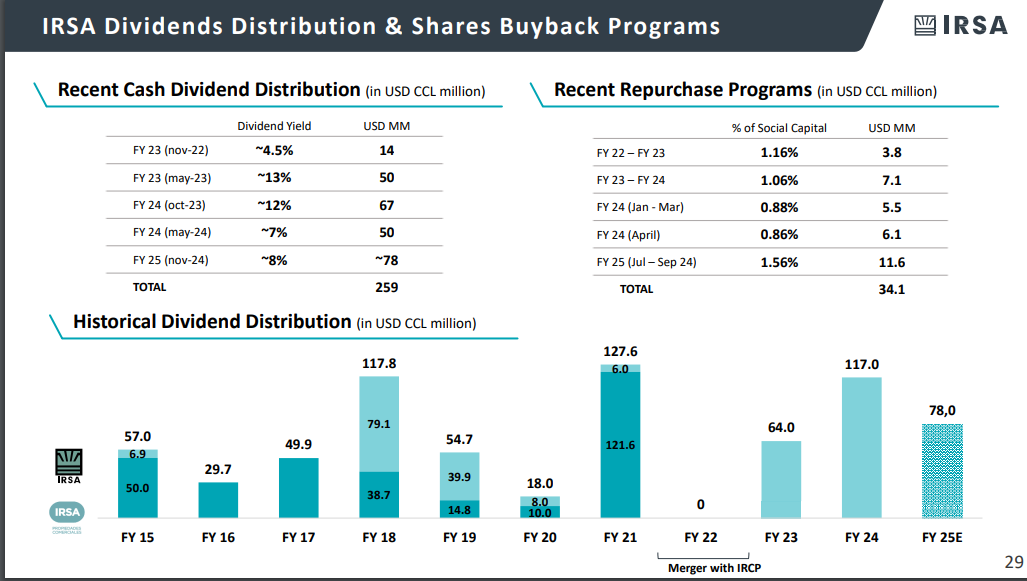

After considering debt payback, Irsa still had cash available. During 2023 and 2024, management strongly favored returning cash to shareholders. Irsa distributed $64M in fiscal year 2023, $117M in 2024, and, in December of 2024, $78M more. At the same time, the company repurchased $34M in shares over the past 2 years. Both elements represented around a 30% yield for investors.

I contacted Irsa’s investor relations department in December 2024 and was notified that, onward, Irsa expects to again focus on reinvesting cash generated. Personally, I would believe they’ll continue paying dividends, and repurchasing stock as long as it seems below fair value to management, but much less aggressively.

Final Remarks

Irsa’s business is centered around redeploying the cash generated by its portfolio of offices, shopping malls, and hotels. I’m inclined to believe that Argentina’s economic environment in the past decade has been detrimental to Irsa’s operations and that the company can generate profits well above the levels heretofore exhibited.

The nature of the assets that make up part of Irsa’s portfolio, namely their local and national relevance, brand value, and quality, make me further suspect their intrinsic value is well in excess of the market’s view thereof. I suspect offices, shopping malls, and hotels have a long runway ahead. I believe chances are high that they’ll continue to generate good levels of cash for the coming years and probably decades.

I conclude their cash generation capacity after analyzing the assets’ economics, high-margin profile, and low capital requirements. On the other hand, the estimated competitive advantage period derives from the nature of these assets, how it has played out thus far, and how it has played out in other countries.

Moreover, if Argentina’s economy begins to grow after a decade of stagnation, consumption should pick up, inevitably benefitting stores within shopping malls. Land, office prices, and rentals would become more expensive. This would benefit Irsa in the form of higher rental revenue and higher base rent charged to tenants. Lastly, to the extent that any sales whatsoever are realized, the price at which these transactions will be made should exceed what the market might’ve agreed to over the past couple of years.

Even under stressful scenarios, Irsa’s portfolio has shown resilience, operating mostly profitably. Considering Irsa’s market capitalization of around $1.35 billion, or an enterprise value of $1.5bn, an investor purchasing a stake in the underlying business would be paying around 1.3 times its book value. I believe that, for the reasons laid in the foregoing report, such a price contains a large enough margin of safety to turn the potential upside into an attractive one.

I must nonetheless observe that, as pointed out in the opening remarks, many things are going on with the business. Complemented with Argentinian companies’ perceived shadiness, plus the country’s history, these factors remain posing the largest risk in this operation. Except for a political and economic setback, these can be extinguished with further due diligence, which is what I encourage the reader to do.

Thank you very much for reading and I encourage you to reach out to me at giulianomana@0to1stockmarket.com if you have any doubts about Irsa.

Disclaimer: This is not financial advice.