I have been reading and writing about Clayton Christensen’s work for 3 months now and there’s definitely no bottom to it. By itself, his theory of disruptive innovation has an unbelievably profound depth. But, moreover, there are infinite concepts that surround the theory and Clayton’s thinking that also bring layers and layers of knowledge. Among these, we find ‘business models’, ‘interdependence vs modularity’, ‘how industries evolve’, and many more we’ll be covering accordingly.

The reason why I’m placing infinite emphasis on learning these things goes around the following. The definition of a theory. A theory is a statement of causality. And a good one can not only detect patterns from observations, but actually predict a phenomenon’s behavior. The good thing about the disruptive theory is that it is industry-agnostic. There is only one process, which seems to be repeated industry after industry. If correct, it should allow us to leverage it in our companies’ industries and foresee whether there are dangers on this front or, even better, if there are not.

Disruption in the steel industry

In the 1990s, Andy Grove’s acquaintances and partners were talking about this new thing called disruptive innovation. Grove was curious and called Clayton directly to see what it was about. After a short conversation, Andy asked him if he could go to Intel’s headquarters on the west coast to explain his theory to Intel’s team and analyze how could it impact the business. Since there are too many specific pieces of information needed to perform a reasonable assessment over each industry, Clayton always tells the story of how disruption worked in the steel industry.

Integrated steel manufacturers had been leading the industry for a long time and were quite comfortable, but things changed when mini mills became technologically viable in the mid 60s. However, the steel quality they could produce was extremely low, which becomes a problem when trying to compete in the high-end of the market.

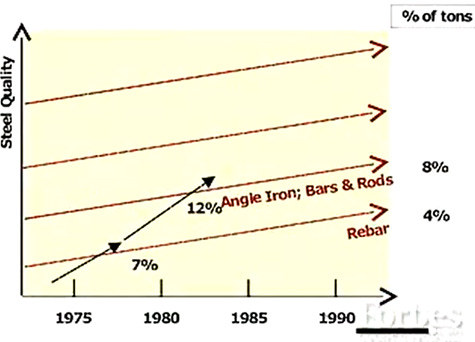

Therefore, the only market that would accept what a mini mill could produce was the concrete reinforcing bar market, at the bottom, because there’s almost no specifications for re-bar. Once it’s buried in cement, the quality is unverifiable and non-required as well, if I’m not mistaken.

At the same time, because the quality of the product didn’t matter that much at this bottom end of the market, margins were in the mid to high single digits. Furthermore, it only accounted for 4% of the industry’s tons produced. Curiously, because mini mills had a 20% cost advantage over integrated manufacturers, their margins in this market were pretty nice.

When integrated manufacturers saw mini mills getting into the re-bar market, they just walked away from it. Not only was this a minuscule part of the industry, but it also reported almost no benefit because of the low margins. Integrated producers, because of the high quality of their steel, could compete at the high end of the market (angle iron; bars & rods), where profit margins were higher. One by one, they started leaving the re-bar market, which went on until 1979, when the last integrated manufacturer left it.

In 1980, when there were only mini mills competing with one another, the price of re-bar dropped by 20%. Once the high cost producing companies left, the remaining producers all had this 20% cost advantage. Added to the fact that steel is a commodity, prices very quickly tended towards costs, as there was no meaningful differentiation between products. At this point, mini mill companies started wondering what would they do since they now weren’t making any profit.

In most industries, the higher you go upmarket, the higher the profit margins. Therefore, these new companies had to find their way into higher tier markets. What hadn’t allowed mini mills to move more rapidly upmarket is that, in parallel, the higher you go, the higher quality is required to compete. In the case of mini mills, they weren’t initially optimized to produce something of higher quality than re-bar. But, little by little, the rates of improvement pushed mini mills quality capacity higher and higher.

That’s the time when mini mills entered the angle iron, bars & rods market. When integrated manufacturers saw this, they were very happy in leaving the bottom end of the industry. Gross margins were a mere 12% and it only represented 8% of total tons produced. Moreover, integrated steel producers had the luxury of competing at the high end of the market, structural steel.

It made no sense to invest in protecting the least profitable part of the business when they could reconfigure their fabs to now produce more of the high margin products. One by one, they were leaving this market and, in 1984, the last one had left it, leaving mini mills competing with one another. A year later, prices drop 20%. Now mini mills find themselves with no profit margins, so what will they do? Well, they have to go up market and compete in structural steel.

The same story happened with structural and, as of 2010, when I think Clayton was shedding light on this matter, mini mills now had half of the sheet steel market.

That is how disruption works, industry after industry. The new lower cost player displaces the giant from the bottom end of the market. One is happy entering it and the other is happy leaving it. They don’t see the threat until, market after market, they get competed away and, finally, the disruptor claims the highest end of the market.

Personal commentary

What a fascinating process. I’m unbelievably dazzled by Clayton’s realizations and I hope you see some of that. I honestly think we can find a lot of use in this theory. It is becoming increasingly clear that we can leverage it to find true compounders or disruptors. It can very much help analyzing competitive landscapes. Anyway, hope you enjoyed the article.

Contact: giulianomana@0to1stockmarket.com

I have no idea why someone should invest in such industries. Sure also today so called "safe harbours" can or will be disrupted some day, but steel never had any moat, high competition, low margins, cyclical...

Hi Giuliano, great article brings back many memories. Two of my first Businesses were in the Steel Industry, one was United Steel: that was in Structural Steel Fabrication and Erection up to 300 Tonnes.

SteelCorp: Was in the Steel Reinforcing Industry and was the First company in Queensland, Australia to incorporate Tapered Threading on Reo Bars for the Construction industry.

In the old days when high rise went up, we used to weld the reo bars end to end, so builders could lay concrete and to go to the next floor as the building rose, or just use lap splicing. It was very slow, labor intensive, we had to drag a welder every where etc.

There was a better way.

I invested in and worked on a new technology in the 80's called Tapered Threading, that allowed me to use a machine, imagine a mobile Plumbers Pipe Threading Machine, about that size.

I would put a course tapered thread on each end of the reo bar, diameter sizes from 12mm up to 50mm Diameter. Small diameter size threading at beginning of reo and widening out the diameter as I got further down the reo bar. The length of the tapered thread was about 50mm to 100mm depending on reo size.

A standard parallel thread is not strong enough to hold the reo bars because they can be in tension or compression, so had to redistribute the weight into not only the threads, but also the diameter of the reo bar and the female Coupler/Collar because of it's strength.

Then the spliced reo bars can behave as continuous lengths of reinforcing steel bars by providing “full strength” in tension, compression and stress reversal applications. It also develops higher tensile strength than lap splicing and provides full load transfer with the slimmest and shortest coupler possible.

The Female Couplers which also had 2 internal tapered threads, one at each end of the coupler and meeting in the middle for inserting and turning the reo bar, and were made in machine shops. This joining system also allowed builders to join different diameter sizes of reo bar together, it was much stronger than side by side (lap splicing) much faster and had a longer life.

So thank you very much for the walk down memory lane.

all the best

Kev Borg

Kiwi